01

MethodologyHow they did it

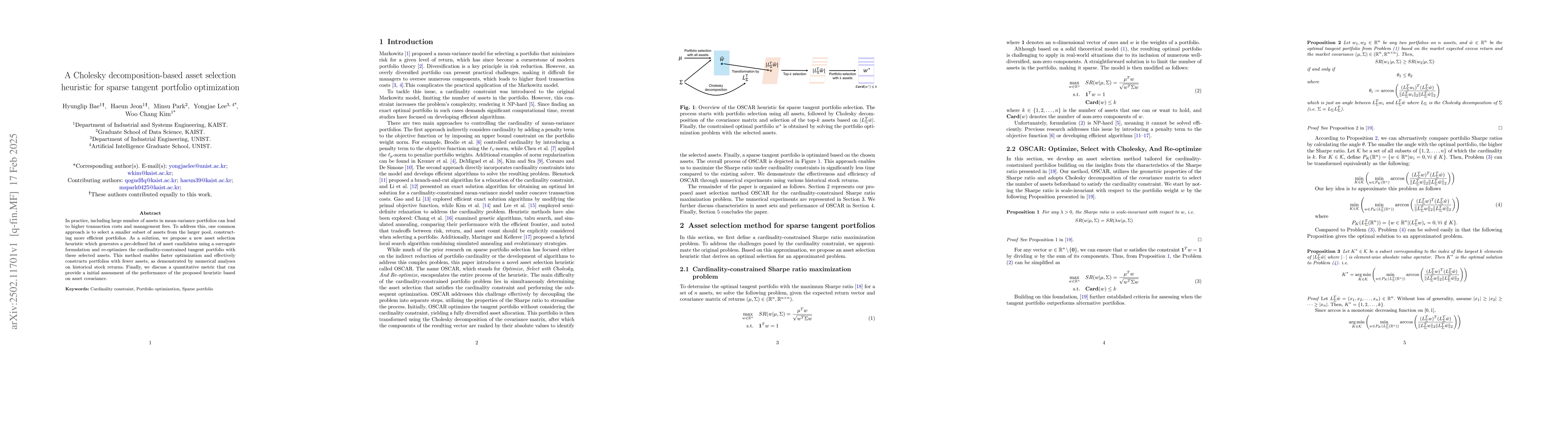

The research proposes a new asset selection heuristic called OSCAR for sparse tangent portfolio optimization. It involves three steps: optimizing the unconstrained version, selecting assets based on the k largest components of |LΣˆw|, and re-optimizing the portfolio optimization problem without cardinality constraint using the selected assets.

Discussion 0