Publication

Metrics

Paper Preview

Abstract

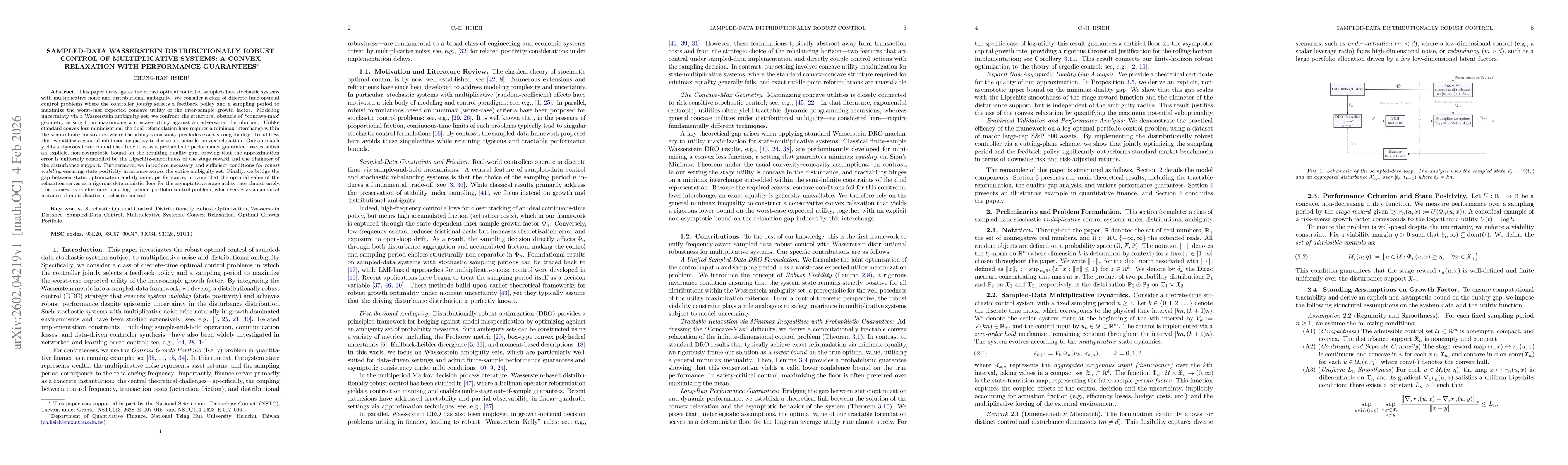

This paper investigates the robust optimal control of sampled-data stochastic systems with multiplicative noise and distributional ambiguity. We consider a class of discrete-time optimal control problems where the controller \emph{jointly} selects a feedback policy and a sampling period to maximize the worst-case expected concave utility of the inter-sample growth factor. Modeling uncertainty via a Wasserstein ambiguity set, we confront the structural obstacle of~``concave-max'' geometry arising from maximizing a concave utility against an adversarial distribution. Unlike standard convex loss minimization, the dual reformulation here requires a minimax interchange within the semi-infinite constraints, where the utility's concavity precludes exact strong duality. To address this, we utilize a general minimax inequality to derive a tractable convex relaxation. Our approach yields a rigorous lower bound that functions as a probabilistic performance guarantee. We establish an explicit, non-asymptotic bound on the resulting duality gap, proving that the approximation error is uniformly controlled by the Lipschitz-smoothness of the stage reward and the diameter of the disturbance support. Furthermore, we introduce necessary and sufficient conditions for \emph{robust viability}, ensuring state positivity invariance across the entire ambiguity set. Finally, we bridge the gap between static optimization and dynamic performance, proving that the optimal value of the relaxation serves as a rigorous deterministic floor for the asymptotic average utility rate almost surely. The framework is illustrated on a log-optimal portfolio control problem, which serves as a canonical instance of multiplicative stochastic control.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0