Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies a risk-sensitive decision-making problem under uncertainty. It considers a decision-making process that unfolds over a fixed number of stages, in which a decision-maker chooses am...

This paper introduces a novel robust trading paradigm, called \textit{multi-double linear policies}, situated within a \textit{generalized} lattice market. Distinctively, our framework departs from ...

This paper introduces a unified framework for adaptive portfolio management, integrating dynamic Black-Litterman (BL) optimization with the general factor model, Elastic Net regression, and mean-var...

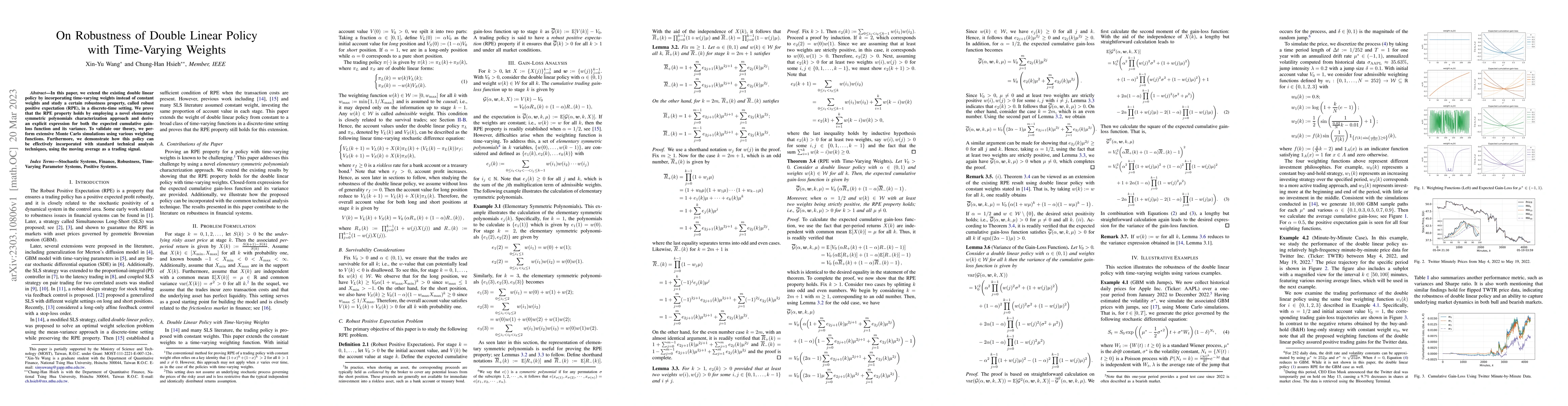

In this paper, we extend the existing double linear policy by incorporating time-varying weights instead of constant weights and study a certain robustness property, called robust positive expectati...

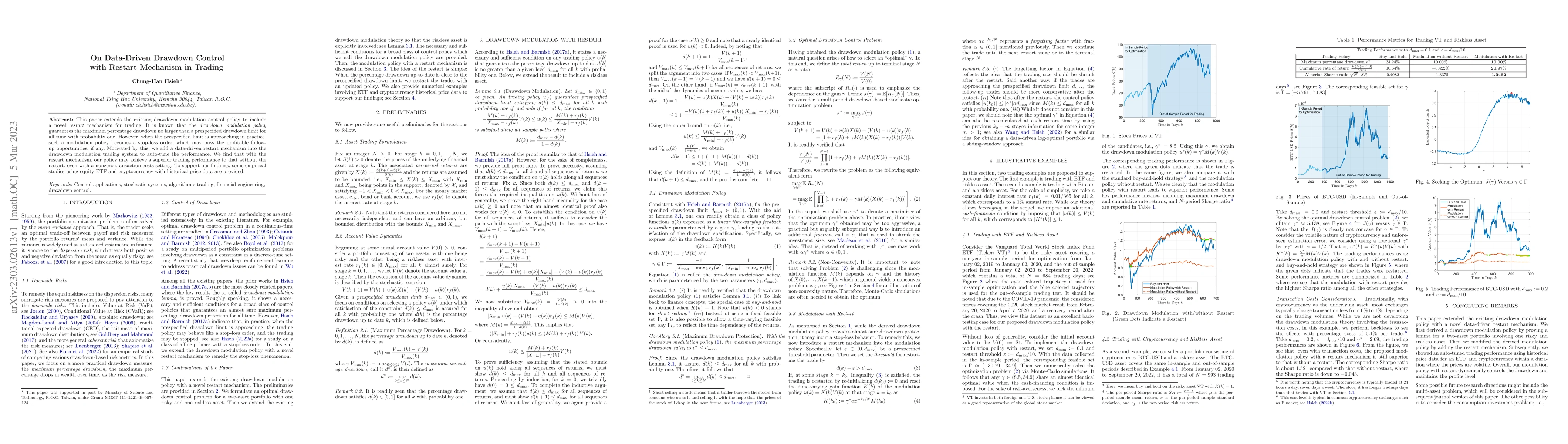

This paper extends the existing drawdown modulation control policy to include a novel restart mechanism for trading. It is known that the drawdown modulation policy guarantees the maximum percentage...

The aim of this paper is to investigate the impact of rebalancing frequency and transaction costs on the log-optimal portfolio, which is a portfolio that maximizes the expected logarithmic growth ra...

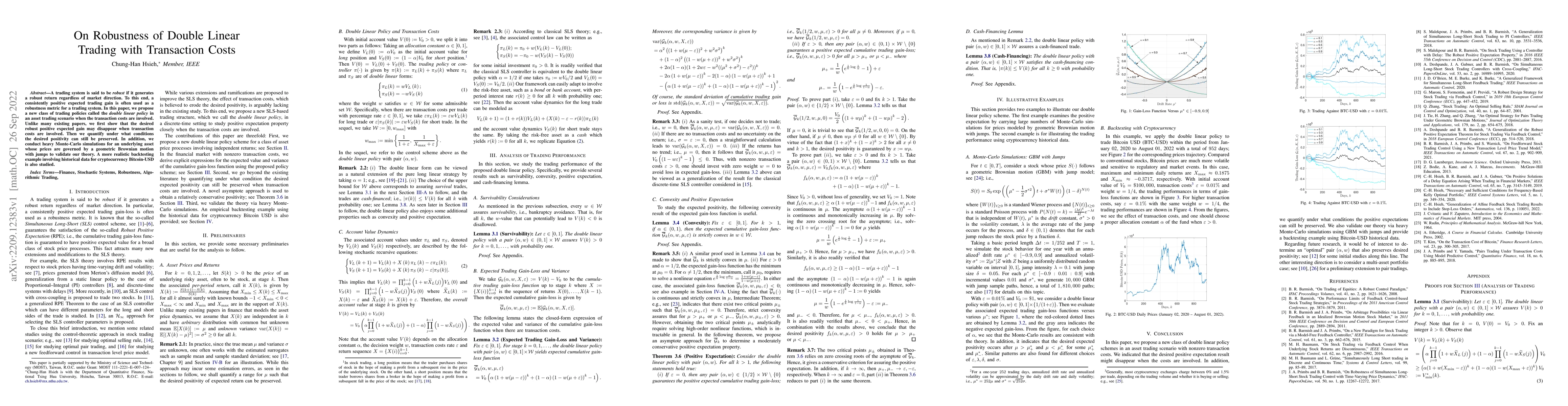

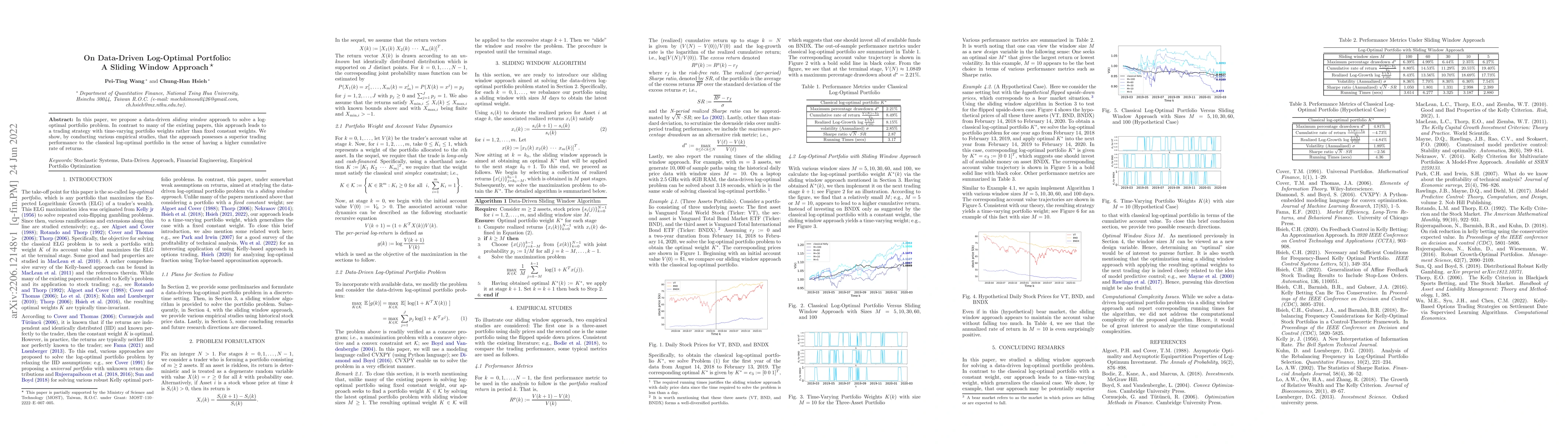

A trading system is said to be {robust} if it generates a robust return regardless of market direction. To this end, a consistently positive expected trading gain is often used as a robustness metri...

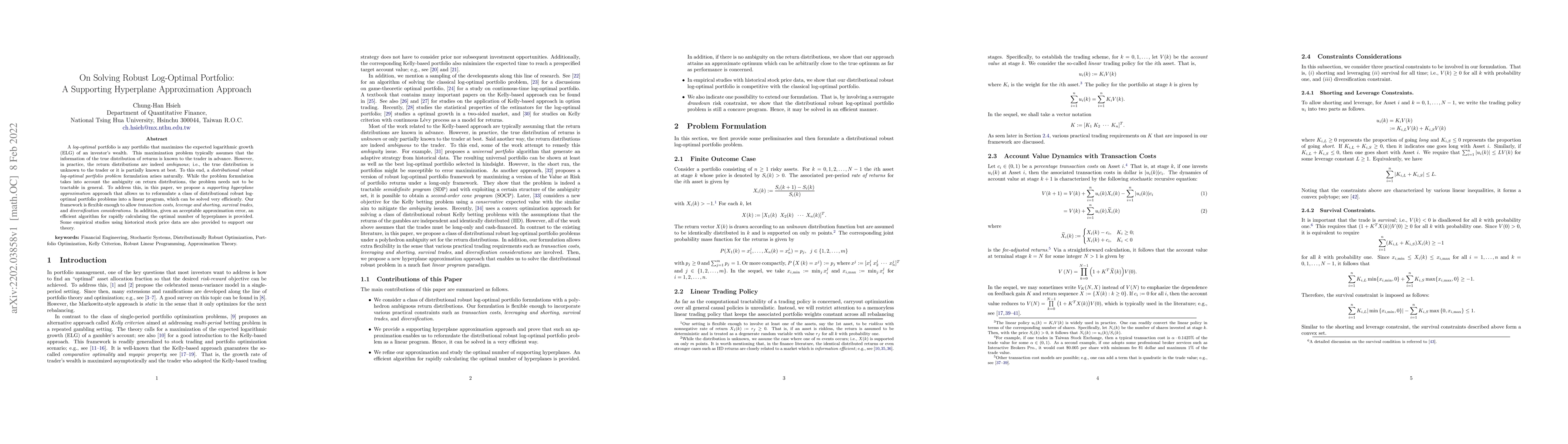

In this paper, we propose a data-driven sliding window approach to solve a log-optimal portfolio problem. In contrast to many of the existing papers, this approach leads to a trading strategy with t...

A {log-optimal} portfolio is any portfolio that maximizes the expected logarithmic growth (ELG) of an investor's wealth. This maximization problem typically assumes that the information of the true ...

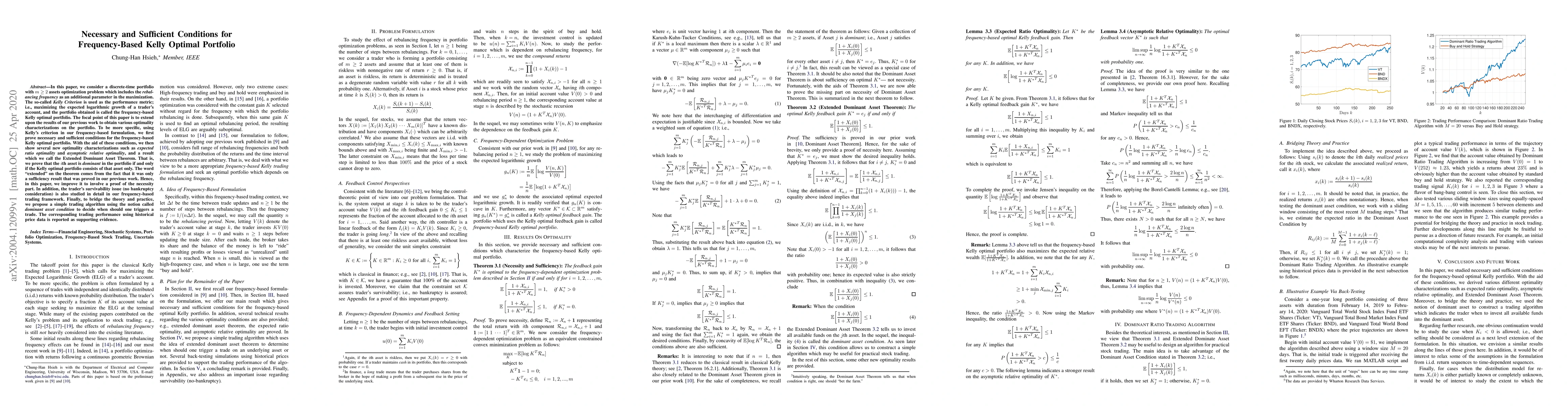

In this paper, we consider a frequency-based portfolio optimization problem with $m \geq 2$ assets when the expected logarithmic growth (ELG) rate of wealth is used as the performance metric. With t...

At the time of writing, the ongoing COVID-19 pandemic, caused by severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), had already resulted in more than thirty-two million cases infected and...

In this paper, we consider a simple discrete-time optimal betting problem using the celebrated Kelly criterion, which calls for maximization of the expected logarithmic growth of wealth. While the c...

The takeoff point of this paper is to generalize the existing stock trading results for a class of affine feedback controller to include consideration of a stop-loss order. Using the geometric Brown...

In this paper, we consider a discrete-time portfolio with $m \geq 2$ assets optimization problem which includes the rebalancing~frequency as an additional parameter in the maximization. The so-calle...

Stock trading based on Kelly's celebrated Expected Logarithmic Growth (ELG) criterion, a well-known prescription for optimal resource allocation, has received considerable attention in the literatur...

Solving large-scale robust portfolio optimization problems is challenging due to the high computational demands associated with an increasing number of assets, the amount of data considered, and marke...

This paper addresses a novel \emph{cost-sensitive} distributionally robust log-optimal portfolio problem, where the investor faces \emph{ambiguous} return distributions, and a general convex transacti...

A common belief is that leveraged ETFs (LETFs) suffer long-term performance decay due to \emph{volatility drag}. We show that this view is incomplete: LETF performance depends fundamentally on return ...

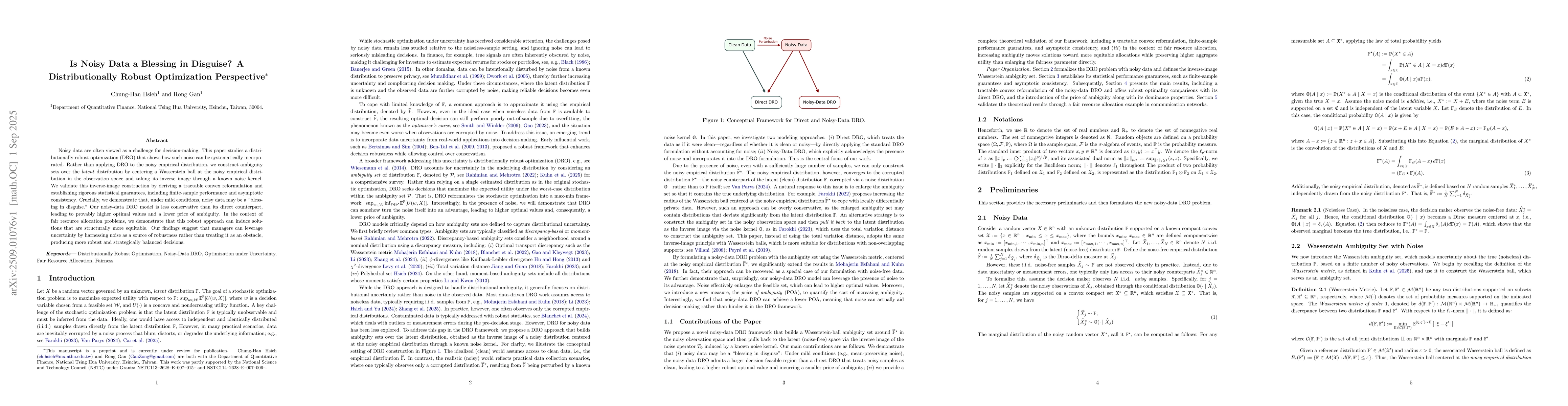

Noisy data are often viewed as a challenge for decision-making. This paper studies a distributionally robust optimization (DRO) that shows how such noise can be systematically incorporated. Rather tha...

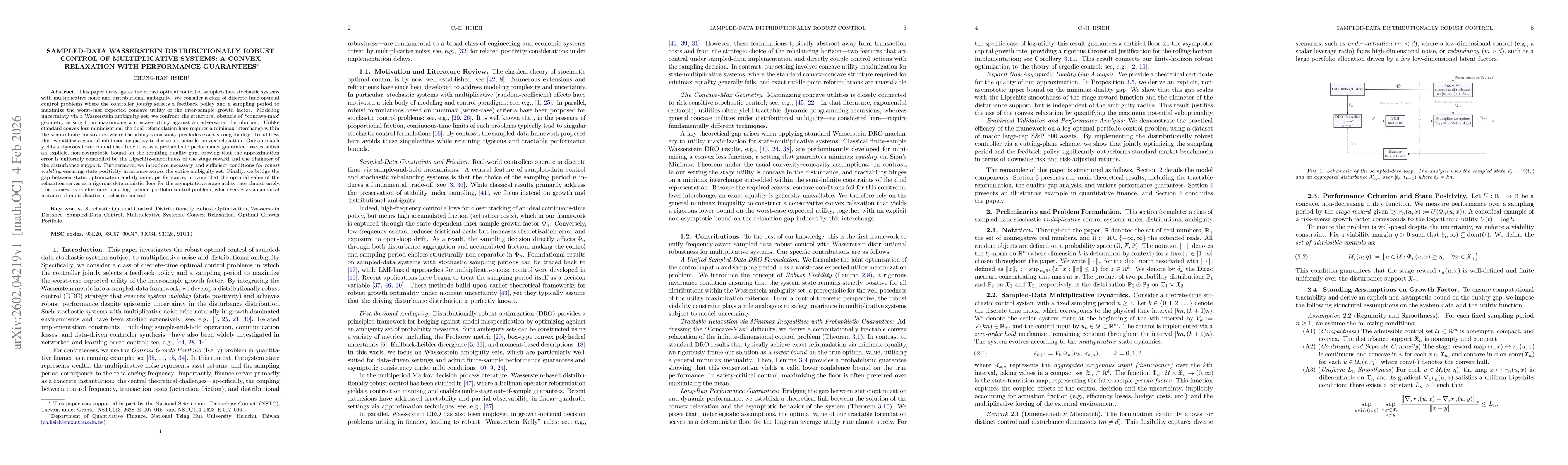

This paper investigates the robust optimal control of sampled-data stochastic systems with multiplicative noise and distributional ambiguity. We consider a class of discrete-time optimal control probl...

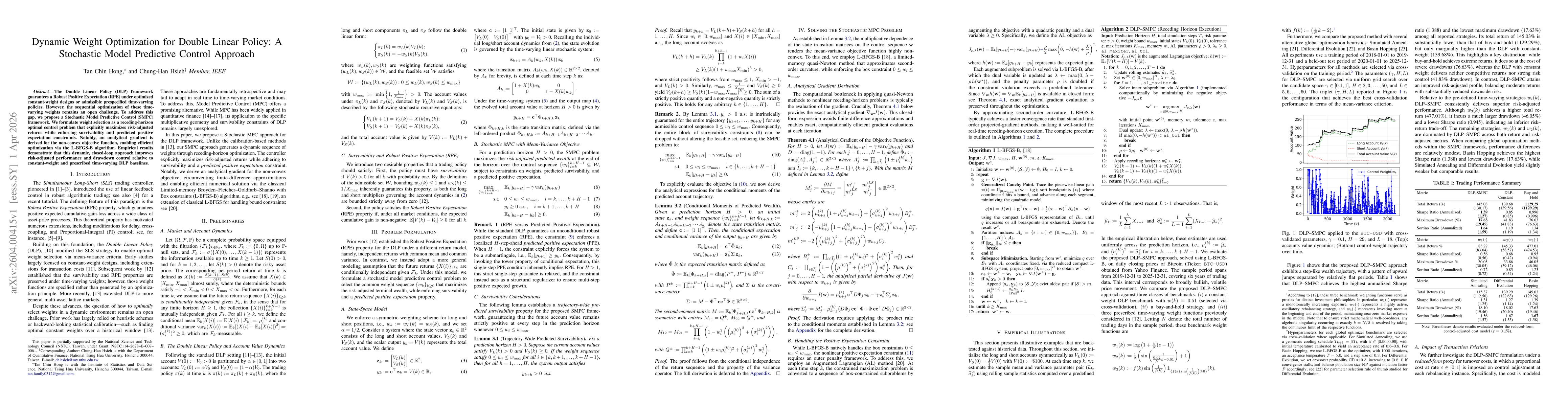

The Double Linear Policy (DLP) framework guarantees a Robust Positive Expectation (RPE) under optimized constant-weight designs or admissible prespecified time-varying policies. However, the sequentia...