Background

The paper situates itself in the landscape of stochastic constraint programming, expanding on Walsh (2002) by relaxing restrictive assumptions and broadening objective options. The key motivation is to model decision problems under uncertainty more expressively while still allowing empirical or analytical solution techniques from constraint programming. The authors align stochastic constraint programming with ideas from stochastic programming and stochastic satisfiability, seeking to blend constraint propagation strength with probabilistic reasoning.

Problem / Research Question

The work asks how to represent multi-stage uncertainty with dependencies, multiple chance constraints, and a richer set of objectives within a constraint programming framework. It also asks how to solve such models without bespoke stochastic solvers, and whether a scenario-based interpretation can bridge to conventional CSP/MIP solvers while preserving solution quality. A core research question is whether scenario-based compilation can yield correct, efficient solutions across a broad class of problems and whether scenario reduction can tame combinatorial explosion.

Innovation / Contribution

The paper’s main contributions are: (1) a scenario-based semantics for stochastic constraint programs that supports multi-stage uncertainty and dependent stochastic variables; (2) generalization to multiple chance constraints and a wider range of optimization goals (e.g., minimizing downside, minimizing spread); (3) a compilation route that translates stochastic programs into conventional, non-stochastic CSPs by enumerating scenarios and aligning shared decisions across them; (4) a practical implementation—stochastic OPL—built on top of the existing OPL modeling language; (5) a portfolio of scenario-reduction techniques (Latin hypercube sampling, Monte Carlo, Dupacova et al.’s reduction) to keep problems tractable; (6) robust optimization capabilities via “robust” decision variables; (7) empirical demonstrations across production planning, portfolio management, yield management, and production/inventory control.

Methodology / Approach

The approach starts by declaring both decision variables and stochastic variables, where stochastic variables are defined with probability distributions and often treated as arrays across time stages. Chance constraints are posted with a prob(C) ≥ θ form, meaning the constraint must hold in at least a θ fraction of scenarios. The semantics adopt a scenario-based view: each scenario provides a concrete realization of the stochastic variables, turning the problem into a conventional constraint program per scenario; first-stage decisions are shared across scenarios, while later-stage decisions are scenario-specific but constrained to maintain consistency.

To solve, the stochastic program is compiled by replacing stochastic variables with their scenario-specific values and turning the higher-level objectives into appropriate sums over scenarios (e.g., expected value). This enables leveraging standard constraint solvers and, when beneficial, hybrid solver strategies that combine constraint programming with integer programming ideas. The framework also introduces robust variables to enforce cross-scenario consistency for selected decisions. Finally, the authors integrate a collection of scenario-reduction techniques to mitigate exponential growth in the number of scenarios, including Latin hypercube sampling and Dupacova–Growe-Kuska-Romisch style reductions, with formal metrics like Fortet-Mourier to guide reductions.

Experiments / Evaluation

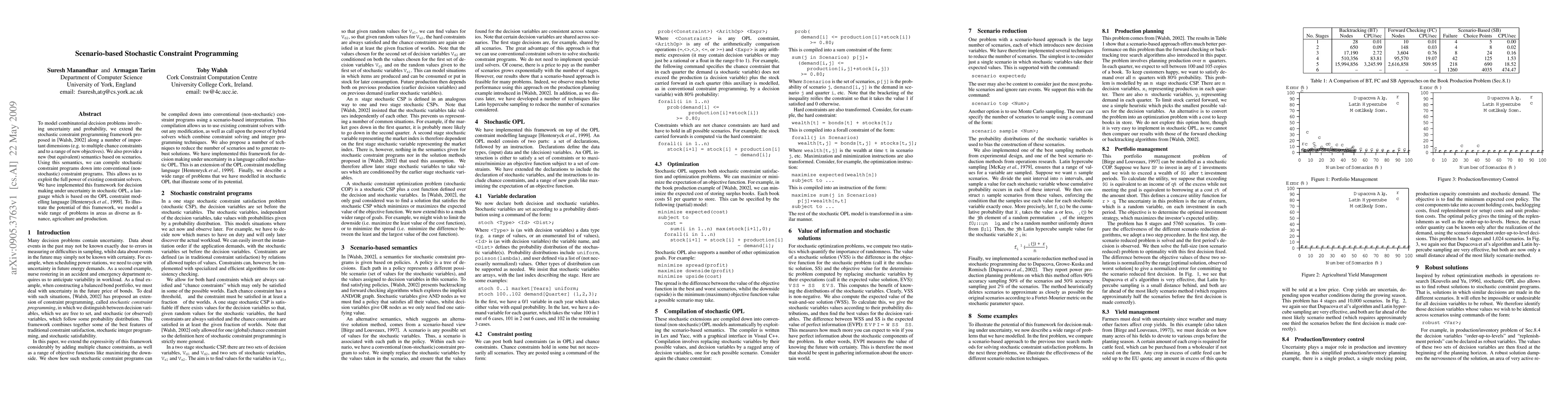

The authors illustrate the framework on a suite of problems drawn from literature and practice. In production planning, a multi-stage problem with an 80% service requirement across quarters demonstrates that scenario-based methods outperform traditional forward checking or backtracking tree search approaches. In portfolio management, a problem with eight stages and thousands of scenarios is used to compare scenario-reduction schemes, showing Dupacova et al.’s reduction and Latin hypercube sampling delivering notably better tradeoffs between solution quality and scenario count. Yield management and production/inventory control problems further corroborate the effectiveness of scenario-based approaches and the value of scenario reduction in achieving near-optimal decisions with substantially fewer scenarios.

Key Results

The core result is that the scenario-based semantics, together with compilation to non-stochastic CSPs, deliver competitive and often superior performance relative to prior stochastic CP methods, particularly on multi-stage problems. The experimental narrative highlights that complexity can be tamed via intelligent scenario reduction while preserving decision quality, and that the approach enables richer objective structures (downside, spread) and robust solutions across scenarios. The framework also demonstrates that existing constraint solvers can be effectively harnessed without bespoke stochastic solvers, validating the practical viability of the approach.

Practical Applications

The framework is positioned for decision-making under uncertainty across finance (portfolio optimization under risk), agriculture (yield planning under weather uncertainty), and production/inventory management (demand and stock risk). Its ability to model non-linear and global constraints, support for robust planning, and compatibility with mature solvers make it attractive for organizations seeking to incorporate probabilistic reasoning into constraint-based planning and scheduling workflows.

Limitations & Considerations

A known limitation is the potential exponential growth of scenarios, which the paper mitigates via reductions but cannot eliminate universally. The accuracy of solutions depends on the chosen scenario set and the quality of the reduction method; mis-specification of stochastic distributions can impact results. While dependencies across stages are allowed, the practical modeling of complex correlations beyond scenario conditioning may require careful formulation. Implementational considerations include memory usage for per-scenario decision variables and the need for practitioners to select appropriate scenario-reduction strategies for their domain and tolerance to approximation error.

Discussion 0