Segment-Based Credit Scoring Using Latent Clusters in the Variational Autoencoder

Publication

Metrics

AI Quick Summary

This paper proposes a novel credit scoring method using a Variational Autoencoder (VAE) to identify customer segments with distinct risk profiles, improving accuracy. The VAE's latent space captures the propensity for financial distress through Weight of Evidence transformation, enabling effective cluster visualization and scalability, while developing individual classifiers for clusters enhances scoring.

Paper Preview

Abstract

Identifying customer segments in retail banking portfolios with different risk profiles can improve the accuracy of credit scoring. The Variational Autoencoder (VAE) has shown promising results in different research domains, and it has been documented the powerful information embedded in the latent space of the VAE. We use the VAE and show that transforming the input data into a meaningful representation, it is possible to steer configurations in the latent space of the VAE. Specifically, the Weight of Evidence (WoE) transformation encapsulates the propensity to fall into financial distress and the latent space in the VAE preserves this characteristic in a well-defined clustering structure. These clusters have considerably different risk profiles and therefore are suitable not only for credit scoring but also for marketing and customer purposes. This new clustering methodology offers solutions to some of the challenges in the existing clustering algorithms, e.g., suggests the number of clusters, assigns cluster labels to new customers, enables cluster visualization, scales to large datasets, captures non-linear relationships among others. Finally, for portfolios with a large number of customers in each cluster, developing one classifier model per cluster can improve the credit scoring assessment.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

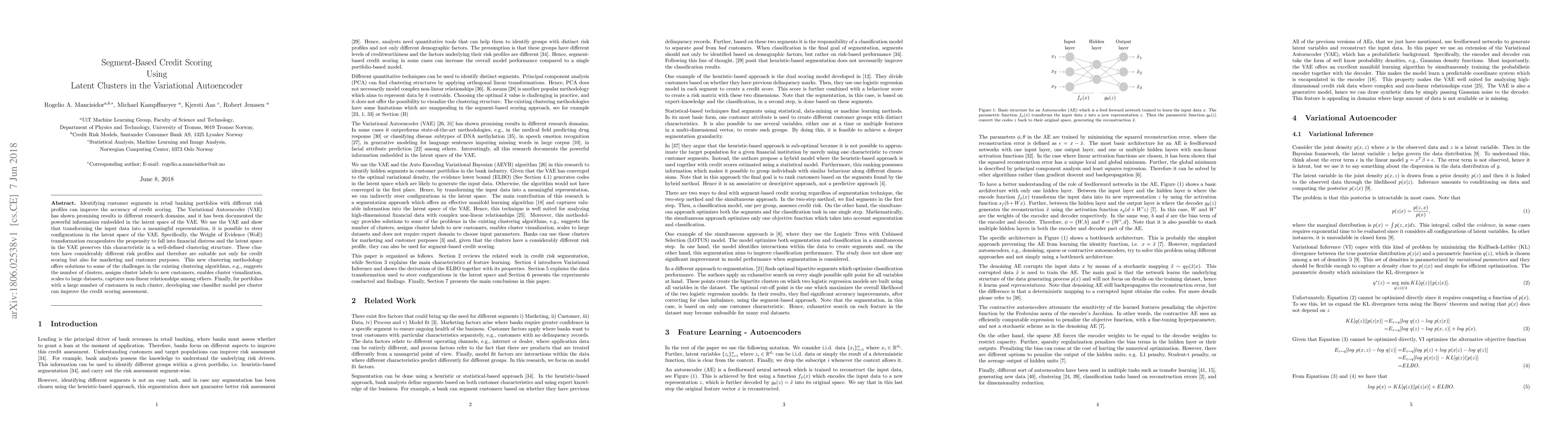

Discussion 0