Given a universe of N assets, investors often form equally weighted

portfolios (EWPs) by selecting subsets of assets. EWPs are simple, robust, and

competitive out-of-sample, yet the uncertainty about which subset truly

performs best is largely ignored. Traditional approaches typically rely on a

single selected portfolio, but this fails to consider alternative investment

strategies that may perform just as well when accounting for statistical

uncertainty. To address this selection uncertainty, we introduce the Selection

Confidence Set (SCS) for EWPs: the set of all portfolios that, under a given

loss function and at a specified confidence level, contains the unknown set of

optimal portfolios under repeated sampling. The SCS quantifies selection

uncertainty by identifying a range of plausible portfolios, challenging the

idea of a uniquely optimal choice. Like a confidence set, its size reflects

uncertainty -- growing with noisy or limited data, and shrinking as the sample

size increases. Theoretically, we establish that the SCS covers the unknown

optimal selection with high probability and characterize how its size grows

with underlying uncertainty, corroborating these results through Monte Carlo

experiments. Applications to the French 17-Industry Portfolios and Layer-1

cryptocurrencies underscore the importance of accounting for selection

uncertainty when comparing equally weighted strategies.

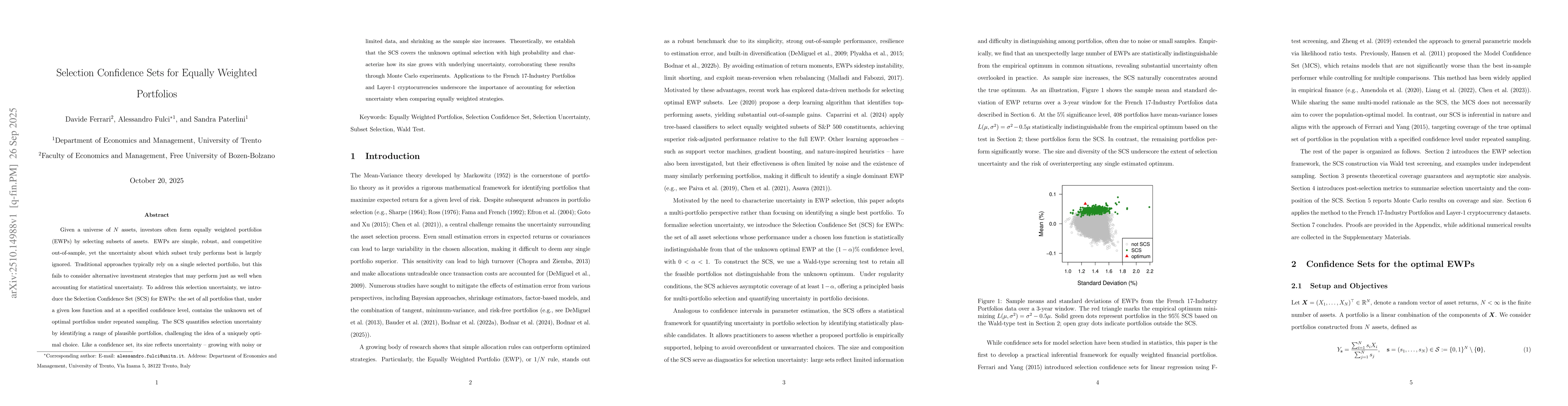

Discussion 0