Academic Profile

Statistics

Similar Authors

Papers on arXiv

Stock price prediction is a crucial element in financial trading as it allows traders to make informed decisions about buying, selling, and holding stocks. Accurate predictions of future stock price...

Sparse graphical modelling has attained widespread attention across various academic fields. We propose two new graphical model approaches, Gslope and Tslope, which provide sparse estimates of the p...

The Markowitz model is still the cornerstone of modern portfolio theory. In particular, when focusing on the minimum-variance portfolio, the covariance matrix or better its inverse, the so-called pr...

We propose a new 2-stage procedure that relies on the elastic net penalty to estimate a network based on partial correlations when data are heavy-tailed. The new estimator allows to consider the las...

Environmental, Social, and Governance (ESG) scores measure companies' performance concerning sustainability and societal impact and are organized on three pillars: Environmental (E), Social (S), and...

While environmental, social, and governance (ESG) trading activity has been a distinctive feature of financial markets, the debate if ESG scores can also convey information regarding a company's ris...

In the context of undirected Gaussian graphical models, we introduce three estimators based on elastic net penalty for the underlying dependence graph. Our goal is to estimate the sparse precision m...

We introduce a financial portfolio optimization framework that allows us to automatically select the relevant assets and estimate their weights by relying on a sorted $\ell_1$-Norm penalization, hen...

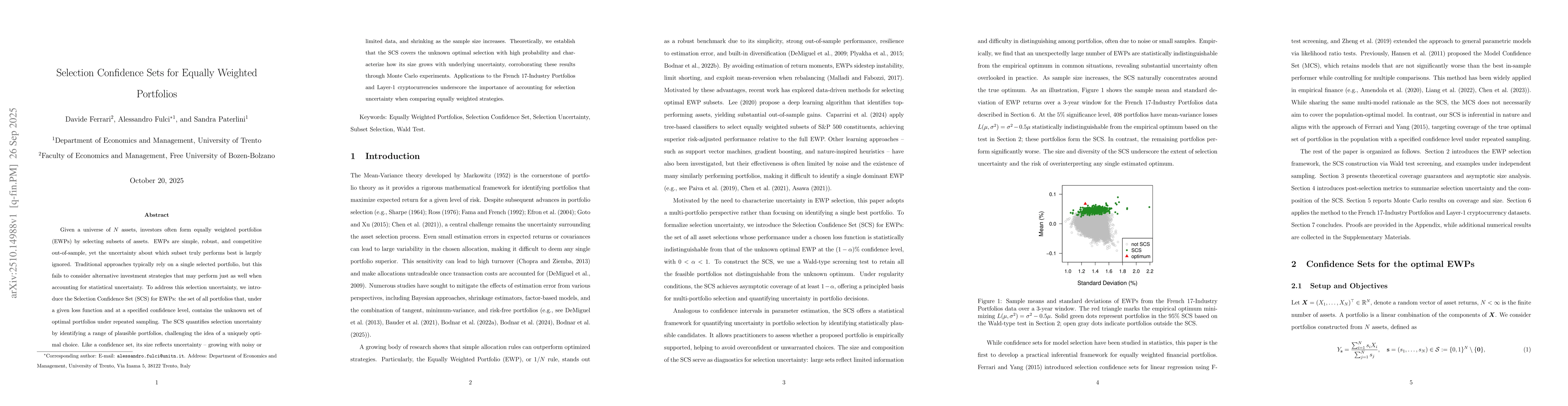

Given a universe of N assets, investors often form equally weighted portfolios (EWPs) by selecting subsets of assets. EWPs are simple, robust, and competitive out-of-sample, yet the uncertainty about ...

This paper studies Graphical SLOPE for precision matrix estimation, with emphasis on its ability to recover both sparsity and clusters of edges with equal or similar strength. In a fixed-dimensional r...