Serial correlation and heterogeneous volatility in financial markets: beyond the LeBaron effect

Publication

Metrics

AI Quick Summary

This paper investigates the relationship between serial correlation in financial returns and volatility at the intraday level for the S&P500 index, confirming the LeBaron effect. It further explores the impact of unexpected volatility on serial correlation, finding that unexpected volatility positively correlates with intraday serial correlation.

Paper Preview

Abstract

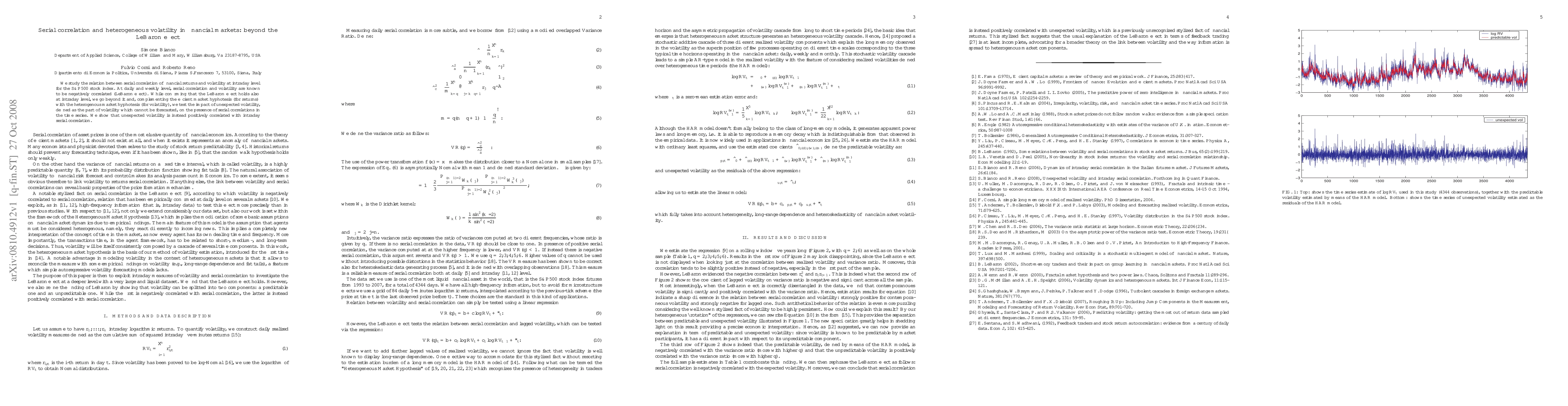

We study the relation between serial correlation of financial returns and volatility at intraday level for the S&P500 stock index. At daily and weekly level, serial correlation and volatility are known to be negatively correlated (LeBaron effect). While confirming that the LeBaron effect holds also at intraday level, we go beyond it and, complementing the efficient market hyphotesis (for returns) with the heterogenous market hyphotesis (for volatility), we test the impact of unexpected volatility, defined as the part of volatility which cannot be forecasted, on the presence of serial correlations in the time series. We show that unexpected volatility is instead positively correlated with intraday serial correlation.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0