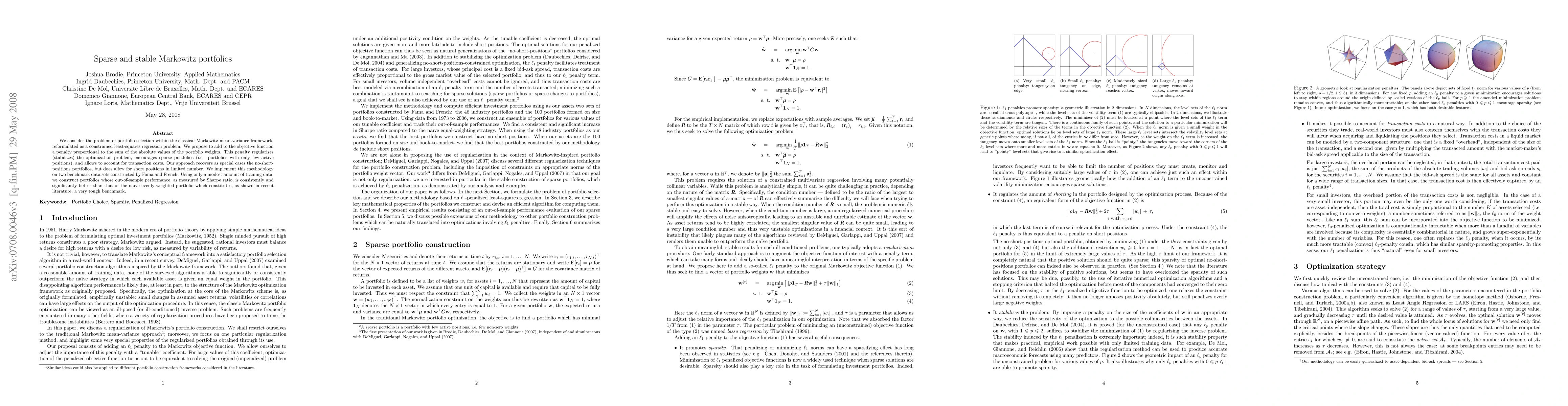

We consider the problem of portfolio selection within the classical Markowitz

mean-variance framework, reformulated as a constrained least-squares regression

problem. We propose to add to the objective function a penalty proportional to

the sum of the absolute values of the portfolio weights. This penalty

regularizes (stabilizes) the optimization problem, encourages sparse portfolios

(i.e. portfolios with only few active positions), and allows to account for

transaction costs. Our approach recovers as special cases the

no-short-positions portfolios, but does allow for short positions in limited

number. We implement this methodology on two benchmark data sets constructed by

Fama and French. Using only a modest amount of training data, we construct

portfolios whose out-of-sample performance, as measured by Sharpe ratio, is

consistently and significantly better than that of the naive evenly-weighted

portfolio which constitutes, as shown in recent literature, a very tough

benchmark.

Discussion 0