Authors

Summary

A novel spatiotemporal framework using diverse econometric approaches is proposed in this research to analyze relationships among eight economy-wide variables in varying market conditions. Employing Vector Autoregression (VAR) and Granger causality, we explore trade policy effects on emerging manufacturing hubs in China, India, Malaysia, Singapore, and Vietnam. A Bayesian Global Vector Autoregression (BGVAR) model also assesses interaction of cross unit and perform Unconditional and Conditional Forecasts. Utilizing time-series data from the Asian Development Bank, our study reveals multi-way cointegration and dynamic connectedness relationships among key economy-wide variables. This innovative framework enhances investment decisions and policymaking through a data-driven approach.

AI Key Findings

Generated Jun 10, 2025

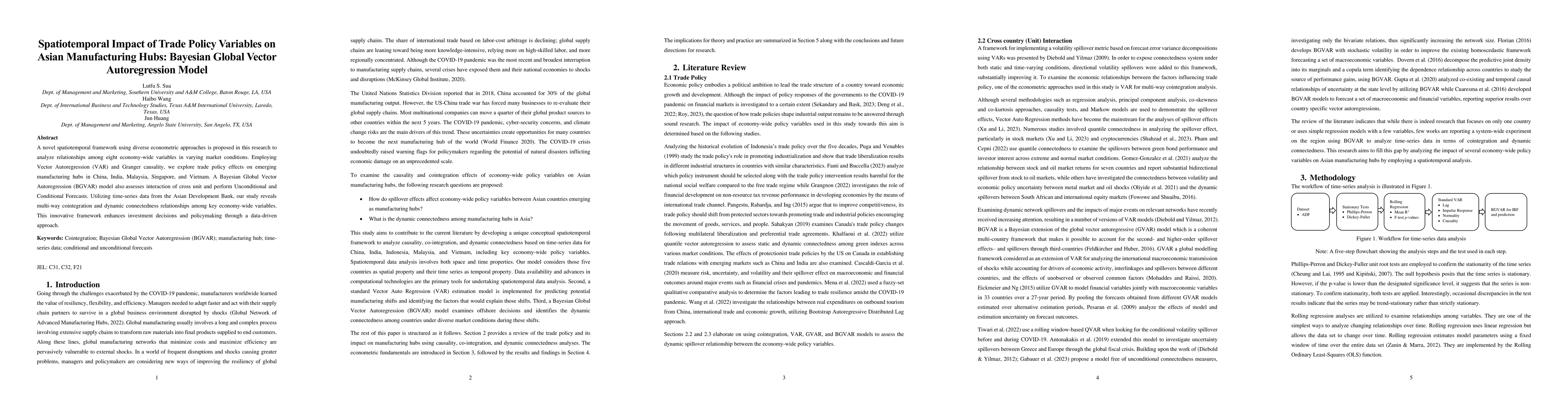

Methodology

This research employs a novel spatiotemporal framework using Vector Autoregression (VAR), Granger causality, and Bayesian Global Vector Autoregression (BGVAR) model to analyze relationships among eight economy-wide variables in varying market conditions. It examines trade policy effects on emerging manufacturing hubs in China, India, Malaysia, Singapore, and Vietnam.

Key Results

- The study reveals multi-way cointegration and dynamic connectedness relationships among key economy-wide variables.

- Compelling evidence rejects the null hypothesis of no cointegration between the variables, with a few exceptions.

- China's centrality in the trade network is highlighted, indicating substantial impacts from its trade policies or shocks on other countries.

- The BGVAR model demonstrates robustness, with weak cross-unit correlations suggesting the model effectively captures country-specific shocks.

- Unconditional forecasts show China's MPI with a clear upward trajectory and low uncertainty, while conditional forecasts illustrate spillover effects from China's policy variables on other countries.

Significance

This research enhances investment decisions and policymaking through a data-driven approach, providing insights into the spatiotemporal impact of trade policy variables on Asian manufacturing hubs, which is crucial for regional economic development and international trade strategies.

Technical Contribution

The paper introduces a Bayesian Global Vector Autoregression (BGVAR) model using the Normal-Gamma prior (NG) to estimate parameters in VAR models, particularly useful for large systems where regularization is needed to prevent overfitting.

Novelty

This research proposes an innovative spatiotemporal framework that combines diverse econometric approaches to analyze the relationships among economy-wide variables in varying market conditions, providing a comprehensive understanding of trade policy effects on Asian manufacturing hubs.

Limitations

- Data availability across countries, such as the Purchasing Managers' Index (PMI), could be expanded to include more nations.

- The study does not investigate the mechanisms driving stronger spillovers like trade intensity and supply chain linkages in detail.

Future Work

- Investigating the mechanisms driving stronger spillovers such as trade intensity and supply chain linkages can help refine policy strategies.

- Examining how specific policy shocks propagate through these manufacturing hubs could provide actionable insights for regional cooperation.

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersLow Tree-Rank Bayesian Vector Autoregression Model

Leo L. Duan, Zhengwu Zhang, George Michailidis et al.

Bayesian Mixed-Frequency Quantile Vector Autoregression: Eliciting tail risks of Monthly US GDP

Aubrey Poon, Dan Zhu, Matteo Iacopini et al.

A Bayesian mixture model for Poisson network autoregression

Gesine Reinert, Anastasia Mantziou, Elly Hung

No citations found for this paper.

Comments (0)