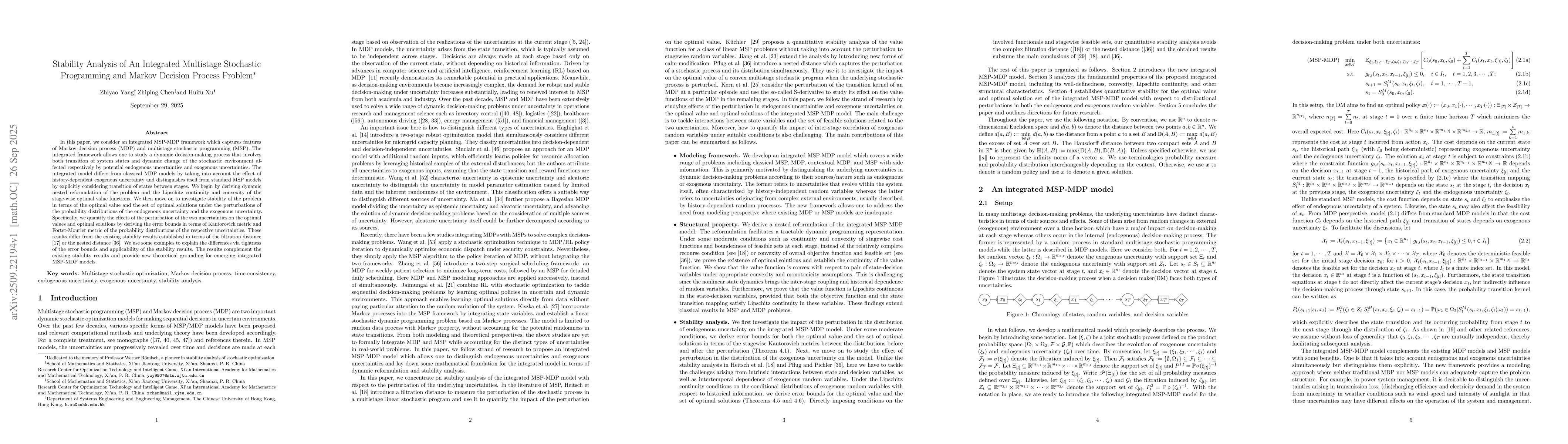

In this paper, we consider an integrated MSP-MDP framework which captures

features of Markov decision process (MDP) and multistage stochastic programming

(MSP). The integrated framework allows one to study a dynamic decision-making

process that involves both transition of system states and dynamic change of

the stochastic environment affected respectively by potential endogenous

uncertainties and exogenous uncertainties. The integrated model differs from

classical MDP models by taking into account the effect of history-dependent

exogenous uncertainty and distinguishes itself from standard MSP models by

explicitly considering transition of states between stages. We begin by

deriving dynamic nested reformulation of the problem and the Lipschitz

continuity and convexity of the stage-wise optimal value functions. We then

move on to investigate stability of the problem in terms of the optimal value

and the set of optimal solutions under the perturbations of the probability

distributions of the endogenous uncertainty and the exogenous uncertainty.

Specifically, we quantify the effects of the perturbation of the two

uncertainties on the optimal values and optimal solutions by deriving the error

bounds in terms of Kantorovich metric and Fortet-Mourier metric of the

probability distributions of the respective uncertainties. These results differ

from the existing stability results established in terms of the filtration

distance \cite{heitsch2009scenario} or the nested distance

\cite{pflug2012distance}. We use some examples to explain the differences via

tightness of the error bounds and applicability of the stability results. The

results complement the existing stability results and provide new theoretical

grounding for emerging integrated MSP-MDP models.

Discussion 0