Academic Profile

Statistics

Similar Authors

Papers on arXiv

Inspired by the recent work [28] on the statistical robustness of empirical risks in reproducing kernel Hilbert space (RKHS) where the training data are potentially perturbed or even corrupted, we t...

Bayesian game is a strategic decision-making model where each player's type parameter characterizing its own objective is private information: each player knows its own type but not its rivals' type...

In this paper, we revisit the LAPUE model with a different focus: we begin by adopting a new penalty function which gives a smooth transition of the boundary between lateness and no lateness and dem...

In this paper, we consider a multi-attribute decision making problem where the decision maker's (DM's) objective is to maximize the expected utility of outcomes but the true utility function which c...

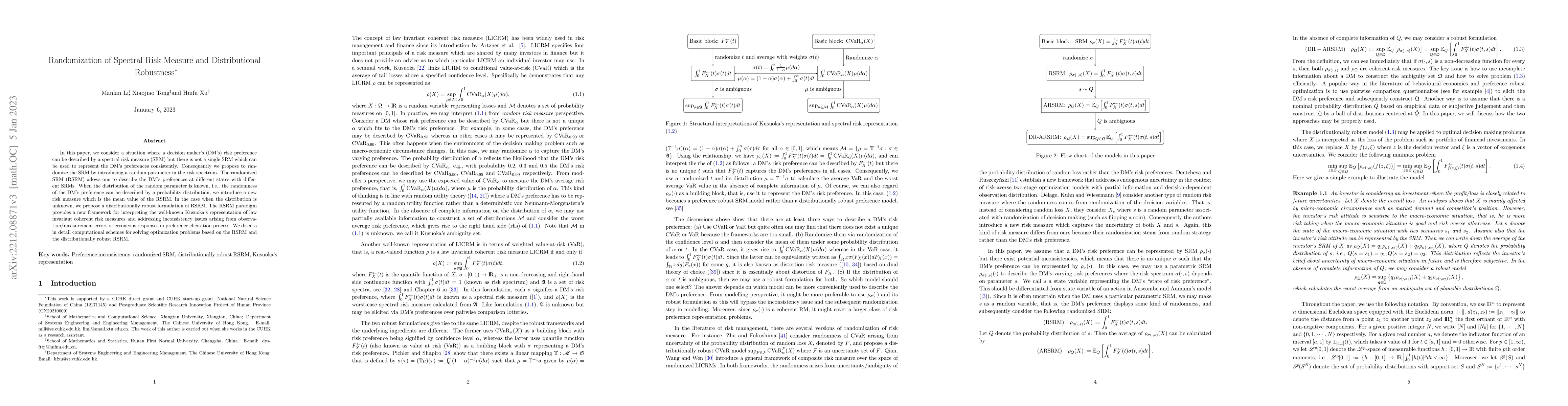

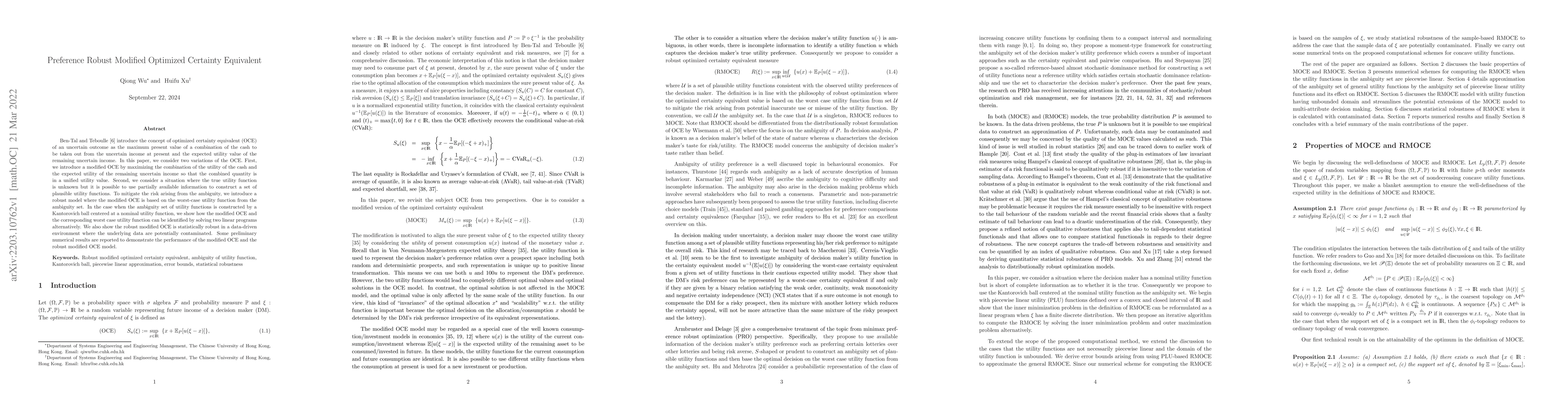

In this paper, we consider a situation where a decision maker's (DM's) risk preference can be described by a spectral risk measure (SRM) but there is not a single SRM which can be used to represent ...

Utility preference robust optimization (PRO) has recently been proposed to deal with optimal decision making problems where the decision maker's (DM) preference over gains and losses is ambiguous. I...

Ben-Tal and Teboulle \cite{BTT86} introduce the concept of optimized certainty equivalent (OCE) of an uncertain outcome as the maximum present value of a combination of the cash to be taken out from...

The utility-based shortfall risk (SR) measure introduced by Folmer and Schied [15] has been recently extended by Mao and Cai [29] to cumulative prospect theory (CPT) based SR in order to better capt...

In this paper, we consider a multistage expected utility maximization problem where the decision maker's utility function at each stage depends on historical data and the information on the true uti...

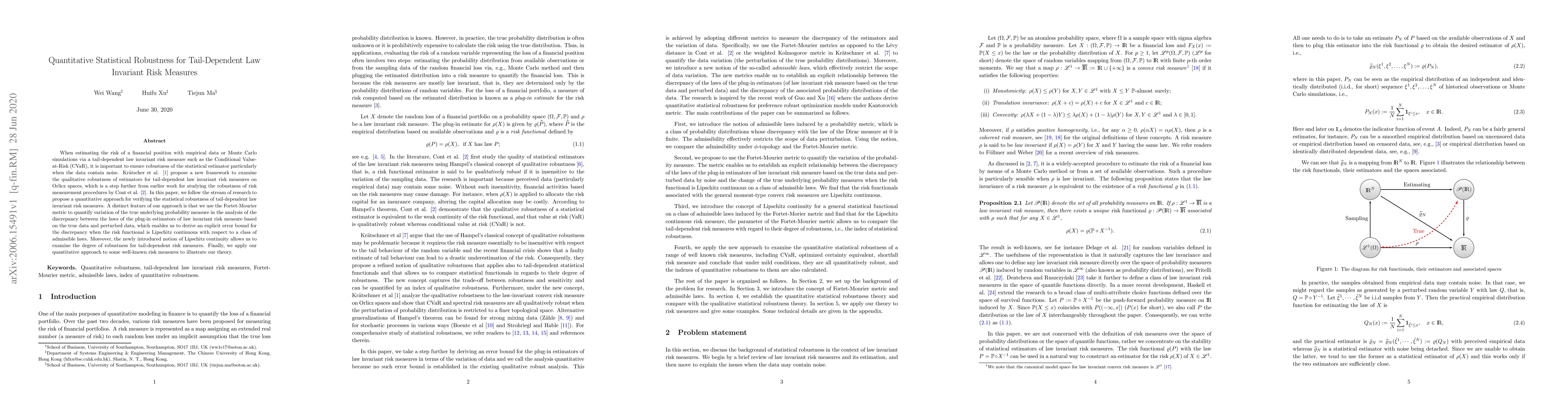

When estimating the risk of a financial position with empirical data or Monte Carlo simulations via a tail-dependent law invariant risk measure such as the Conditional Value-at-Risk (CVaR), it is im...

This paper studies convergence of empirical risks in reproducing kernel Hilbert spaces (RKHS). A conventional assumption in the existing research is that empirical training data do not contain any n...

Finding an approximation of the inverse of the covariance matrix, also known as precision matrix, of a random vector with empirical data is widely discussed in finance and engineering. In data-driven ...

Inspired by the recent work by Shapiro et al. [45], we propose a Bayesian distributionally robust Nash equilibrium (BDRNE) model where each player lacks complete information on the true probability di...

In this paper, we revisit the multistage spectral risk minimization models proposed by Philpott et al.~\cite{PdF13} and Guigues and R\"omisch \cite{GuR12} but with some new focuses. We consider a situ...

Inspired by \cite{shapiro2023episodic}, we consider a stochastic optimal control (SOC) and Markov decision process (MDP) where the risks arising from epistemic and aleatoric uncertainties are assessed...

We consider risk-averse contextual optimization problems where the decision maker (DM) faces two types of uncertainties: problem data uncertainty (PDU) and contextual uncertainty (CU) associated with ...

In this paper, we propose a modified polyhedral method to elicit a decision maker's (DM's) nonlinear univariate utility function, which does not rely on explicit information about the shape structure,...

We investigate a data-driven quasiconcave maximization problem where information about the objective function is limited to a finite sample of data points. We begin by defining an ambiguity set for ad...

In this paper, we consider an integrated MSP-MDP framework which captures features of Markov decision process (MDP) and multistage stochastic programming (MSP). The integrated framework allows one to ...

Since the seminal work by Meirowitz, there has been growing attention on the existence and uniqueness of continuous Bayesian Nash equilibria. In the existing literature, existence is typically establi...

We propose a distributionally robust formulation for simultaneously estimating the covariance matrix and the precision matrix of a random vector.The proposed model minimizes the worst-case weighted su...

Massive MIMO (Multiple-Input Multiple-Output) is a key enabler for 5G and future wireless systems, boosting channel capacity, energy efficiency, and spectral efficiency. However, high power consumptio...

Integrated learning and optimization (ILO) is a framework in contextual optimization which aims to train a predictive model for the probability distribution of the underlying problem data uncertainty,...

In stochastic optimal control (SOC), uncertainty may arise from incomplete knowledge of the true probability distribution of the underlying environment, which is known as Knightian or epistemic uncert...

In this paper, we propose a coordinate-wise polyhedral method (CPM) for cutting polyhedra with theoretical guarantees of convergence. Unlike the existing polyhedral method, which designs pairwise comp...

In this paper, we propose a new approach, called maximum utility split (MUS) scheme, which is built on random utility split (RUS) scheme but with a notable difference: one lottery is designed with two...