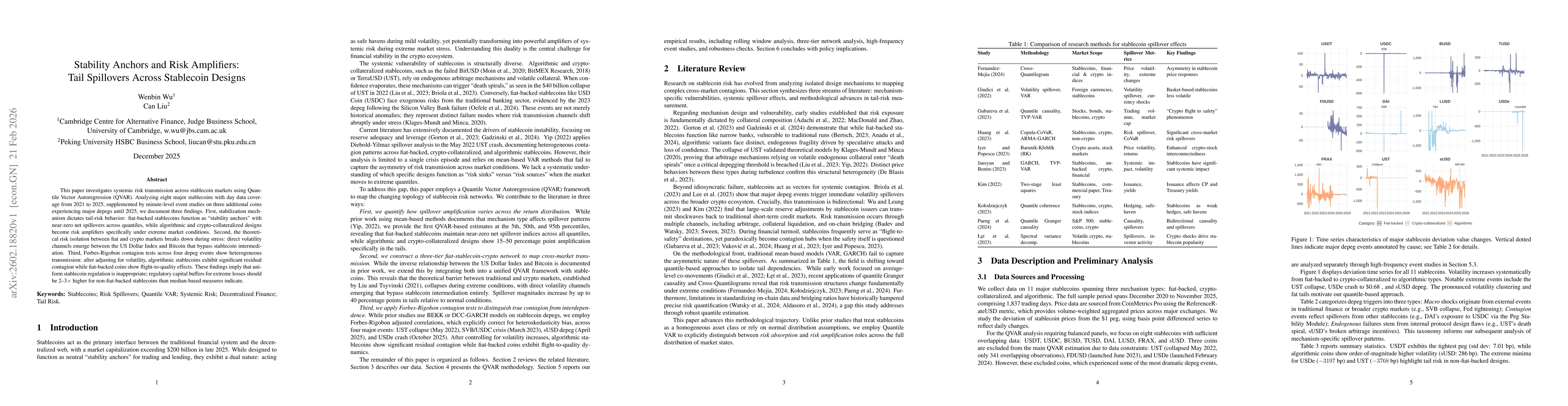

This paper investigates systemic risk transmission across stablecoin markets using Quantile Vector Autoregression (QVAR). Analyzing eight major stablecoins with day data coverage from 2021 to 2025, supplemented by minute-level event studies on three additional coins experiencing major depegs until 2025, we document three findings. First, stabilization mechanism dictates tail-risk behavior: fiat-backed stablecoins function as "stability anchors" with near-zero net spillovers across quantiles, while algorithmic and crypto-collateralized designs become risk amplifiers specifically under extreme market conditions. Second, the theoretical risk isolation between fiat and crypto markets breaks down during stress: direct volatility channels emerge between the US Dollar Index and Bitcoin that bypass stablecoin intermediation. Third, Forbes-Rigobon contagion tests across four depeg events show heterogeneous transmission: after adjusting for volatility, algorithmic stablecoins exhibit significant residual contagion while fiat-backed coins show flight-to-quality effects. These findings imply that uniform stablecoin regulation is inappropriate; regulatory capital buffers for extreme losses should be 2--3x higher for non-fiat-backed stablecoins than median-based measures indicate.

Discussion 0