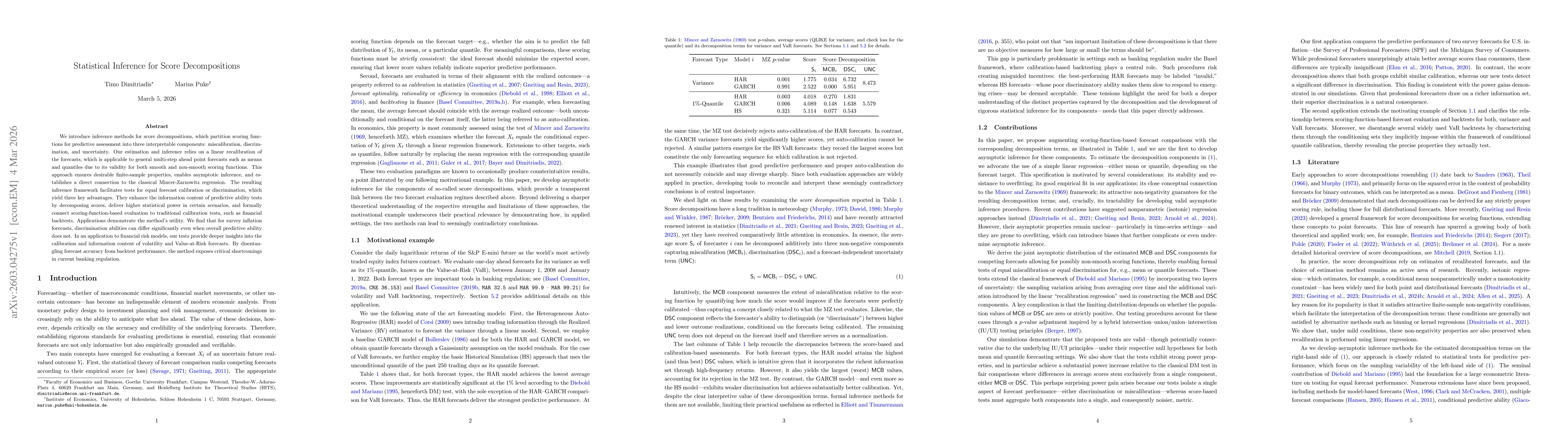

We introduce inference methods for score decompositions, which partition scoring functions for predictive assessment into three interpretable components: miscalibration, discrimination, and uncertainty. Our estimation and inference relies on a linear recalibration of the forecasts, which is applicable to general multi-step ahead point forecasts such as means and quantiles due to its validity for both smooth and non-smooth scoring functions. This approach ensures desirable finite-sample properties, enables asymptotic inference, and establishes a direct connection to the classical Mincer-Zarnowitz regression. The resulting inference framework facilitates tests for equal forecast calibration or discrimination, which yield three key advantages. They enhance the information content of predictive ability tests by decomposing scores, deliver higher statistical power in certain scenarios, and formally connect scoring-function-based evaluation to traditional calibration tests, such as financial backtests. Applications demonstrate the method's utility. We find that for survey inflation forecasts, discrimination abilities can differ significantly even when overall predictive ability does not. In an application to financial risk models, our tests provide deeper insights into the calibration and information content of volatility and Value-at-Risk forecasts. By disentangling forecast accuracy from backtest performance, the method exposes critical shortcomings in current banking regulation.

Discussion 0