Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel regression framework which simultaneously models the quantile and the Expected Shortfall (ES) of a response variable given a set of covariates. This regression is based on a str...

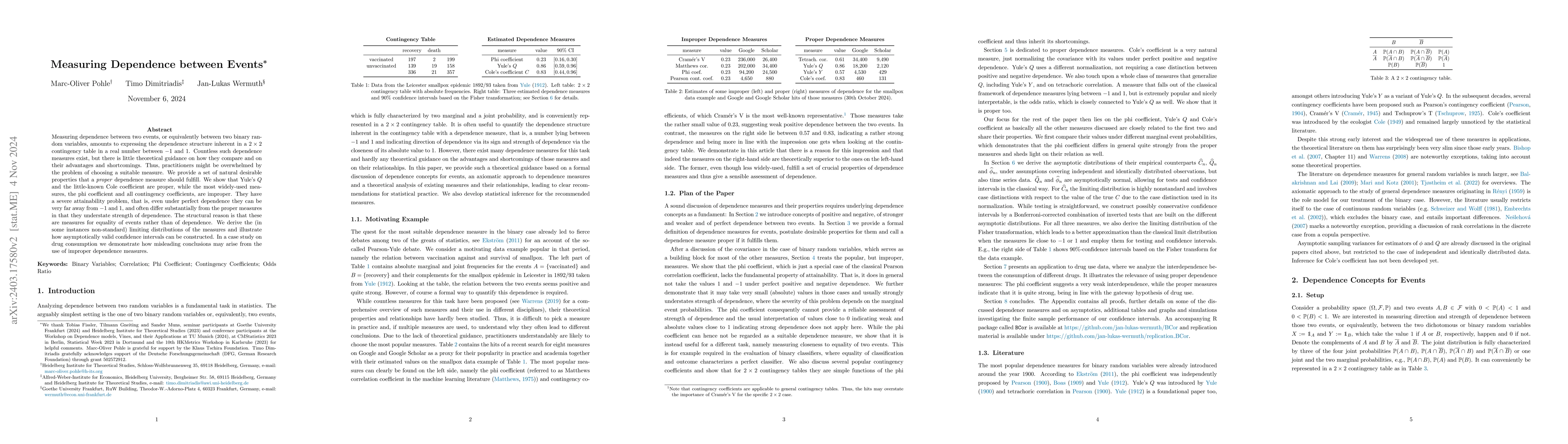

Measuring dependence between two events, or equivalently between two binary random variables, amounts to expressing the dependence structure inherent in a $2\times 2$ contingency table in a real num...

We introduce a new regression method that relates the mean of an outcome variable to covariates, given the "adverse condition" that a distress variable falls in its tail. This allows to tailor class...

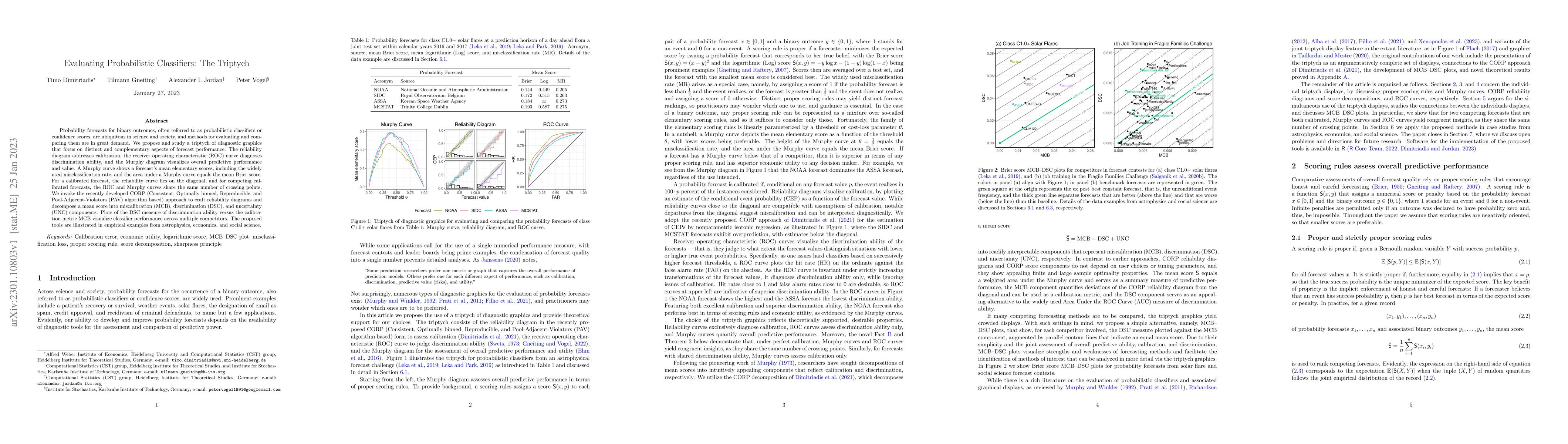

Probability forecasts for binary outcomes, often referred to as probabilistic classifiers or confidence scores, are ubiquitous in science and society, and methods for evaluating and comparing them a...

This paper analyzes the benefits of sampling intraday returns in intrinsic time for the standard and pre-averaging realized variance (RV) estimators. We theoretically show in finite samples and asym...

We characterize the full classes of M-estimators for semiparametric models of general functionals by formally connecting the theory of consistent loss functions from forecast evaluation with the the...

Given a statistical functional of interest such as the mean or median, a (strict) identification function is zero in expectation at (and only at) the true functional value. Identification functions ...

The popular systemic risk measure CoVaR (conditional Value-at-Risk) is widely used in economics and finance. Formally, it is defined as a large quantile of one variable (e.g., losses in the financia...

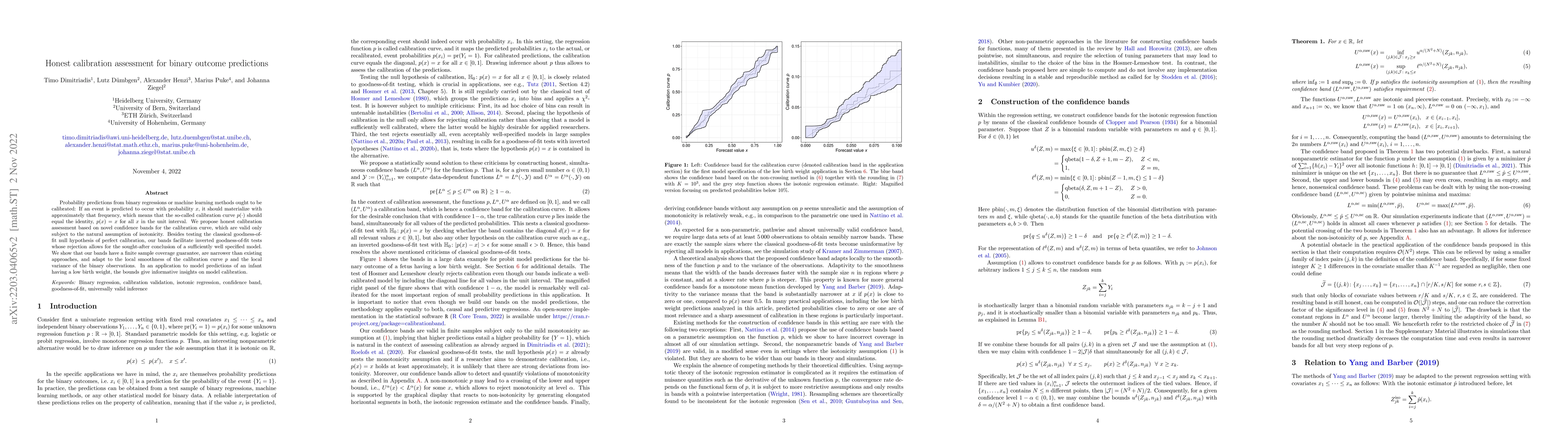

Probability predictions from binary regressions or machine learning methods ought to be calibrated: If an event is predicted to occur with probability $x$, it should materialize with approximately t...

This article proposes an alternative to the Hosmer-Lemeshow (HL) test for evaluating the calibration of probability forecasts for binary events. The approach is based on e-values, a new tool for hyp...

Loss functions are widely used to compare several competing forecasts. However, forecast comparisons are often based on mismeasured proxy variables for the true target. We introduce the concept of e...

Parameter estimation via M- and Z-estimation is equally powerful in semiparametric models for one-dimensional functionals due to a one-to-one relation between corresponding loss and identification f...

We propose forecast encompassing tests for the Expected Shortfall (ES) jointly with the Value at Risk (VaR) based on flexible link (or combination) functions. Our setup allows testing encompassing f...

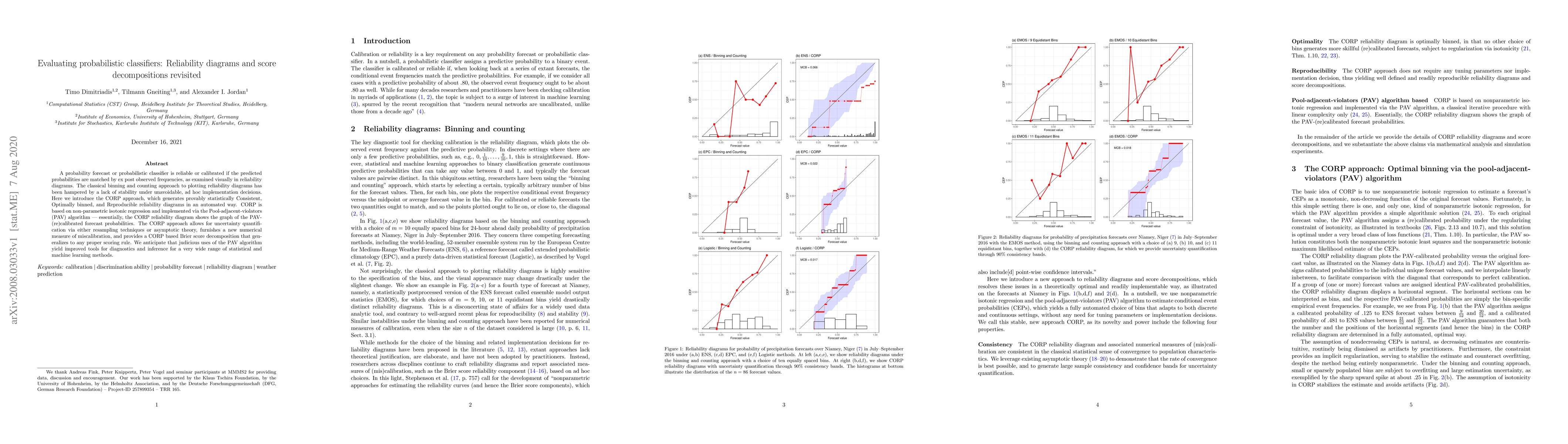

A probability forecast or probabilistic classifier is reliable or calibrated if the predicted probabilities are matched by ex post observed frequencies, as examined visually in reliability diagrams....

Rational respondents to economic surveys may report as a point forecast any measure of the central tendency of their (possibly latent) predictive distribution, for example the mean, median, mode, or...

We introduce new forecast encompassing tests for the risk measure Expected Shortfall (ES). The ES currently receives much attention through its introduction into the Basel III Accords, which stipula...

This paper introduces novel backtests for the risk measure Expected Shortfall (ES) following the testing idea of Mincer and Zarnowitz (1969). Estimating a regression framework for the ES stand-alone...

Score-driven models have been applied in some 400 published articles over the last decade. Much of this literature cites the optimality result in Blasques et al. (2015), which, roughly, states that su...

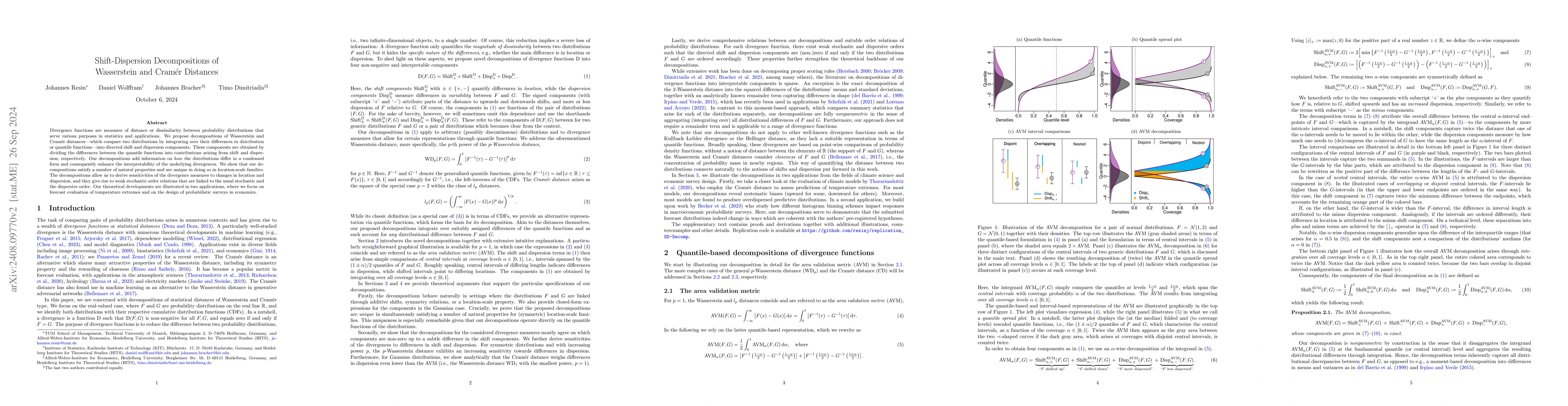

Divergence functions are measures of distance or dissimilarity between probability distributions that serve various purposes in statistics and applications. We propose decompositions of Wasserstein an...

Following several episodes of financial market turmoil in recent decades, changes in systemic risk have drawn growing attention. Therefore, we propose surveillance schemes for systemic risk, which all...

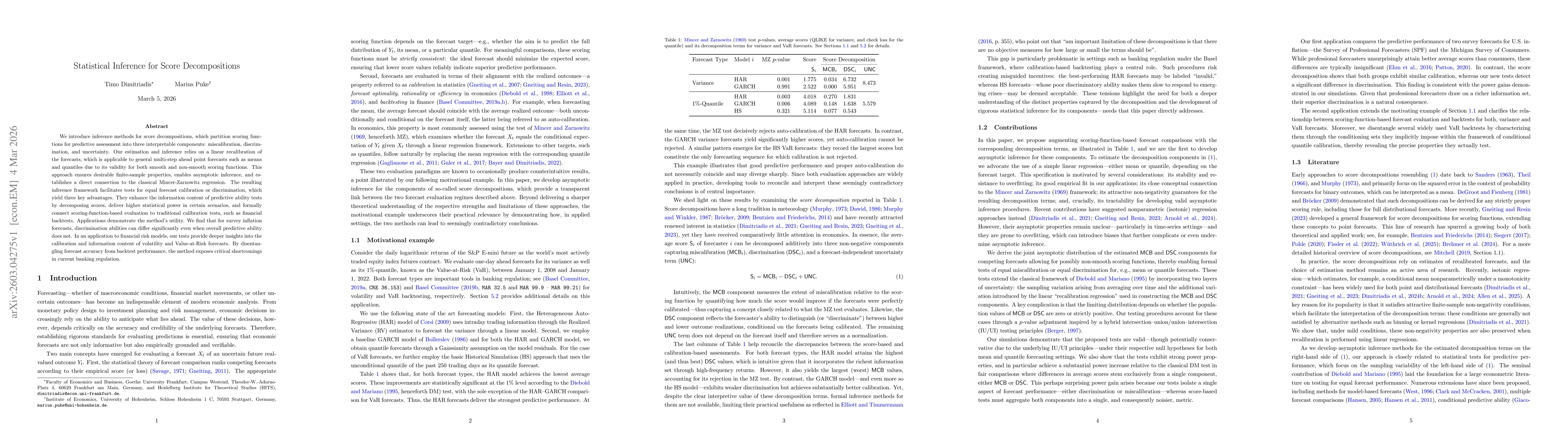

We introduce inference methods for score decompositions, which partition scoring functions for predictive assessment into three interpretable components: miscalibration, discrimination, and uncertaint...