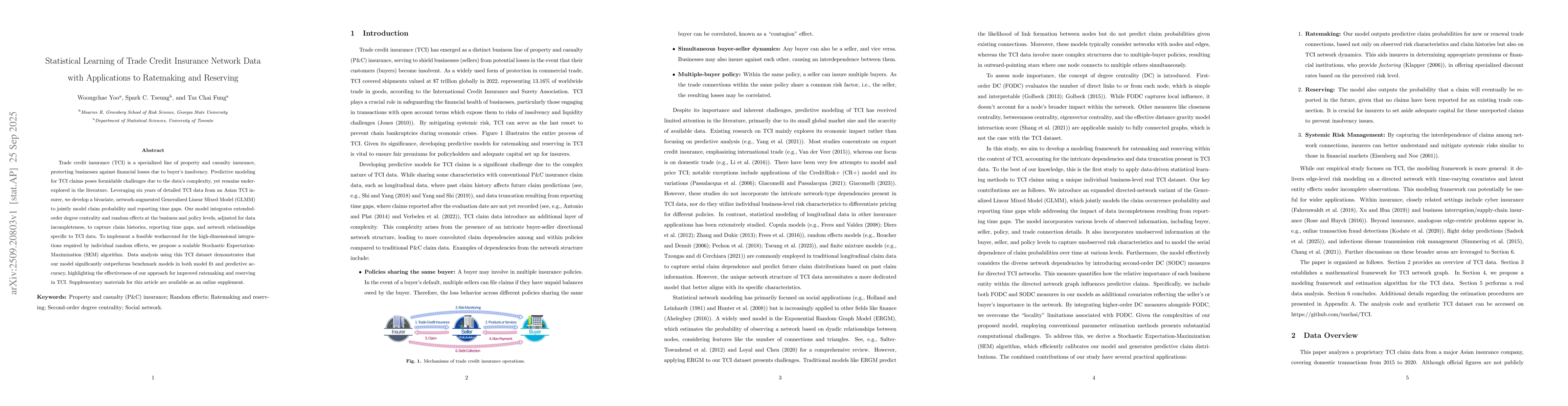

Trade credit insurance (TCI) is a specialized line of property and casualty

insurance, protecting businesses against financial losses due to buyer's

insolvency. Predictive modeling for TCI claims poses formidable challenges due

to the data's complexity, yet remains underexplored in the literature.

Leveraging six years of detailed TCI data from an Asian TCI insurer, we develop

a bivariate, network-augmented Generalized Linear Mixed Model (GLMM) to jointly

model claim probability and reporting time gaps. Our model integrates

extended-order degree centrality and random effects at the business and policy

levels, adjusted for data incompleteness, to capture claim histories, reporting

time gaps, and network relationships specific to TCI data. To implement a

feasible workaround for the high-dimensional integrations required by

individual random effects, we propose a scalable Stochastic

Expectation-Maximization (SEM) algorithm. Data analysis using this TCI dataset

demonstrates that our model significantly outperforms benchmark models in both

model fit and predictive accuracy, highlighting the effectiveness of our

approach for improved ratemaking and reserving in TCI. Supplementary materials

for this article are available as an online supplement.

Discussion 0