Publication

Metrics

Paper Preview

Abstract

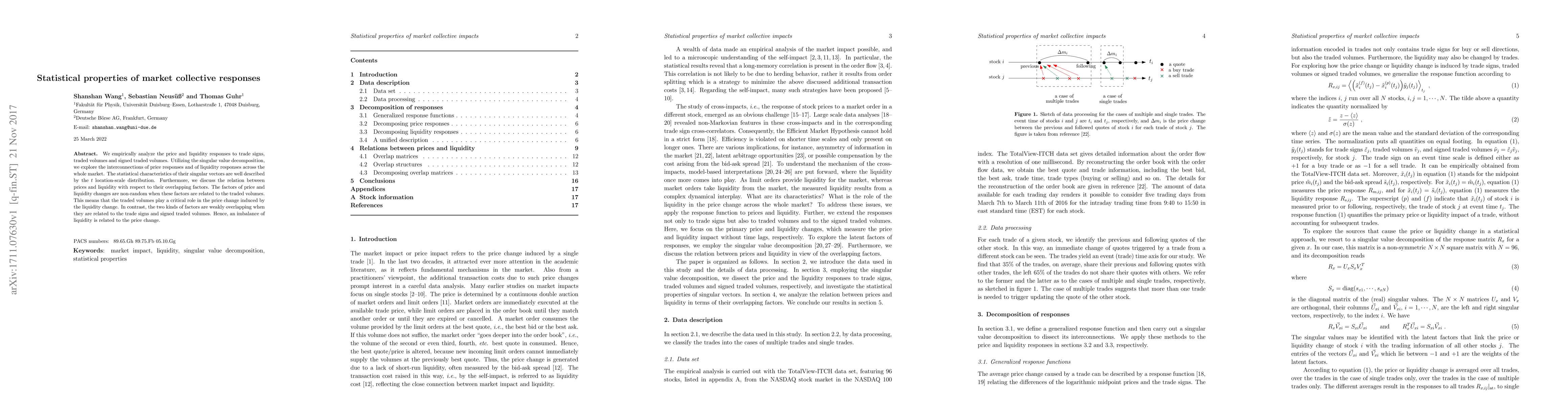

We empirically analyze the price and liquidity responses to trade signs, traded volumes and signed traded volumes. Utilizing the singular value decomposition, we explore the interconnections of price responses and of liquidity responses across the whole market. The statistical characteristics of their singular vectors are well described by the $t$ location-scale distribution. Furthermore, we discuss the relation between prices and liquidity with respect to their overlapping factors. The factors of price and liquidity changes are non-random when these factors are related to the traded volumes. This means that the traded volumes play a critical role in the price change induced by the liquidity change. In contrast, the two kinds of factors are weakly overlapping when they are related to the trade signs and signed traded volumes. Hence, an imbalance of liquidity is related to the price change.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0