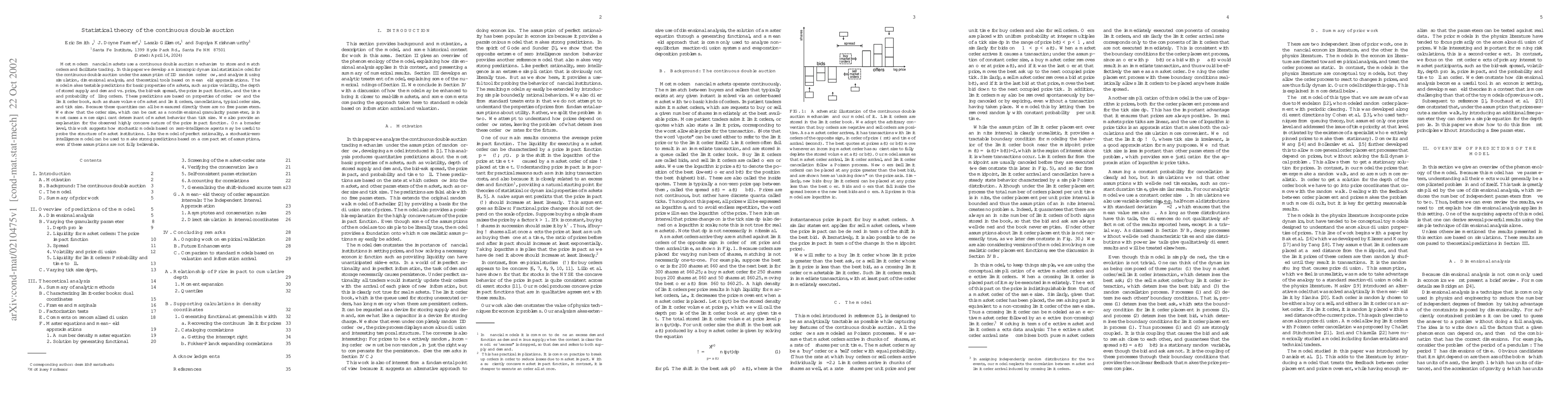

Most modern financial markets use a continuous double auction mechanism to

store and match orders and facilitate trading. In this paper we develop a

microscopic dynamical statistical model for the continuous double auction under

the assumption of IID random order flow, and analyze it using simulation,

dimensional analysis, and theoretical tools based on mean field approximations.

The model makes testable predictions for basic properties of markets, such as

price volatility, the depth of stored supply and demand vs. price, the bid-ask

spread, the price impact function, and the time and probability of filling

orders. These predictions are based on properties of order flow and the limit

order book, such as share volume of market and limit orders, cancellations,

typical order size, and tick size. Because these quantities can all be measured

directly there are no free parameters. We show that the order size, which can

be cast as a nondimensional granularity parameter, is in most cases a more

significant determinant of market behavior than tick size. We also provide an

explanation for the observed highly concave nature of the price impact

function. On a broader level, this work suggests how stochastic models based on

zero-intelligence agents may be useful to probe the structure of market

institutions. Like the model of perfect rationality, a stochastic-zero

intelligence model can be used to make strong predictions based on a compact

set of assumptions, even if these assumptions are not fully believable.

Discussion 0