Publication

Metrics

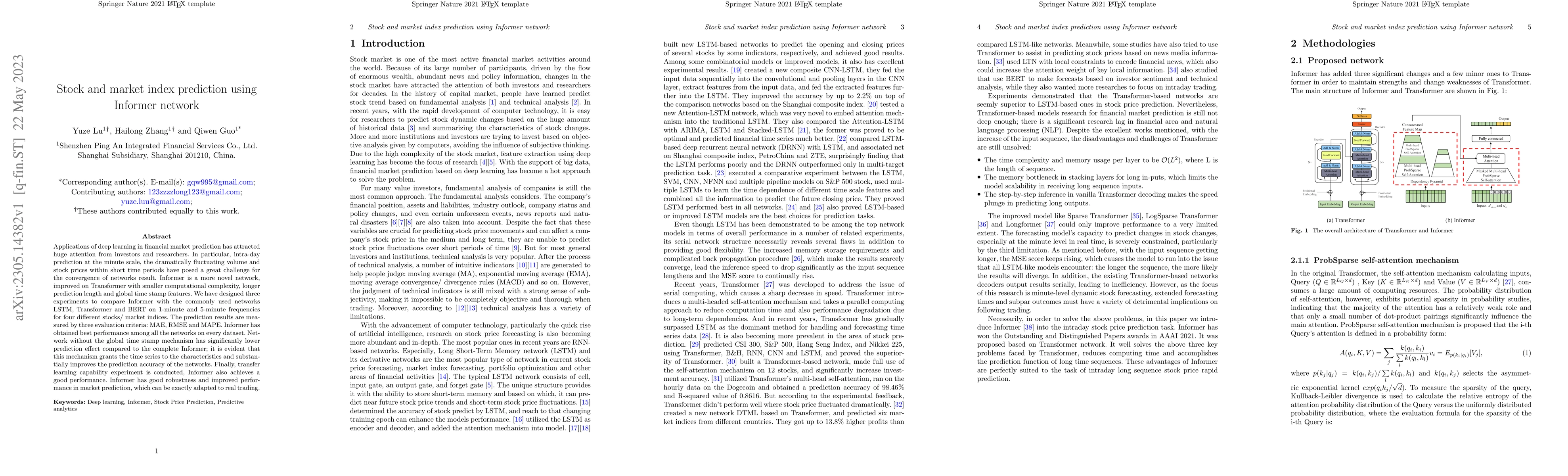

AI Quick Summary

Informer network outperforms LSTM, Transformer, and BERT in predicting intra-day stock and market index prices, demonstrating superior performance across various evaluation metrics and showcasing enhanced robustness and transfer learning capabilities. The inclusion of global time stamp features significantly boosts prediction accuracy.

Paper Preview

Abstract

Applications of deep learning in financial market prediction has attracted huge attention from investors and researchers. In particular, intra-day prediction at the minute scale, the dramatically fluctuating volume and stock prices within short time periods have posed a great challenge for the convergence of networks result. Informer is a more novel network, improved on Transformer with smaller computational complexity, longer prediction length and global time stamp features. We have designed three experiments to compare Informer with the commonly used networks LSTM, Transformer and BERT on 1-minute and 5-minute frequencies for four different stocks/ market indices. The prediction results are measured by three evaluation criteria: MAE, RMSE and MAPE. Informer has obtained best performance among all the networks on every dataset. Network without the global time stamp mechanism has significantly lower prediction effect compared to the complete Informer; it is evident that this mechanism grants the time series to the characteristics and substantially improves the prediction accuracy of the networks. Finally, transfer learning capability experiment is conducted, Informer also achieves a good performance. Informer has good robustness and improved performance in market prediction, which can be exactly adapted to real trading.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0