Stock market indices serve as fundamental market measurement that quantify

systematic market dynamics. However, accurate index price prediction remains

challenging, primarily because existing approaches treat indices as isolated

time series and frame the prediction as a simple regression task. These methods

fail to capture indices' inherent nature as aggregations of constituent stocks

with complex, time-varying interdependencies. To address these limitations, we

propose Cubic, a novel end-to-end framework that explicitly models the adaptive

fusion of constituent stocks for index price prediction. Our main contributions

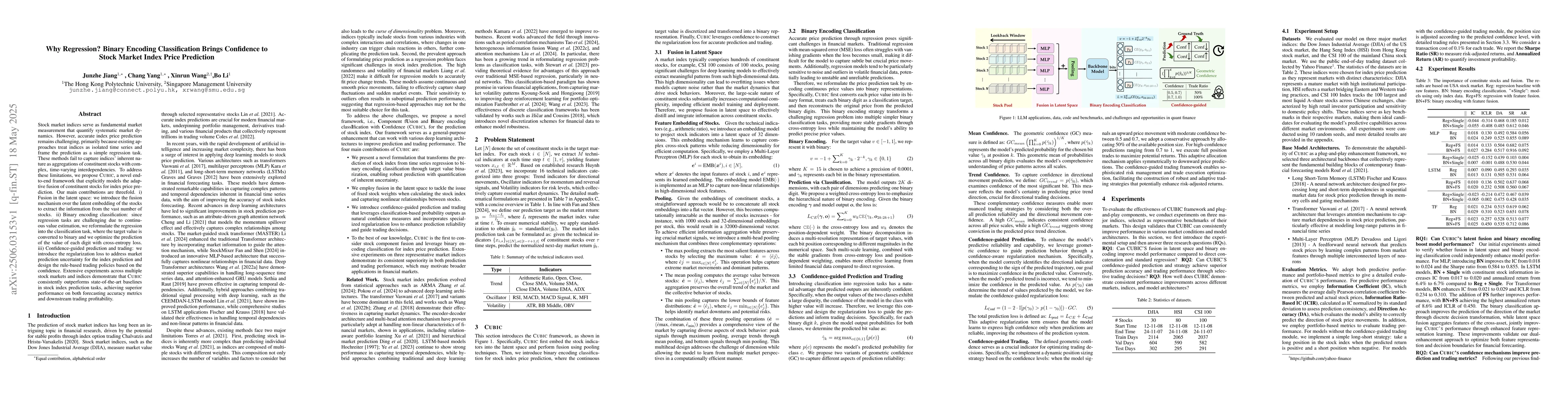

are threefold. i) Fusion in the latent space: we introduce the fusion mechanism

over the latent embedding of the stocks to extract the information from the

vast number of stocks. ii) Binary encoding classification: since regression

tasks are challenging due to continuous value estimation, we reformulate the

regression into the classification task, where the target value is converted to

binary and we optimize the prediction of the value of each digit with

cross-entropy loss. iii) Confidence-guided prediction and trading: we introduce

the regularization loss to address market prediction uncertainty for the index

prediction and design the rule-based trading policies based on the confidence.

Extensive experiments across multiple stock markets and indices demonstrate

that Cubic consistently outperforms state-of-the-art baselines in stock index

prediction tasks, achieving superior performance on both forecasting accuracy

metrics and downstream trading profitability.

Discussion 0