Authors

Summary

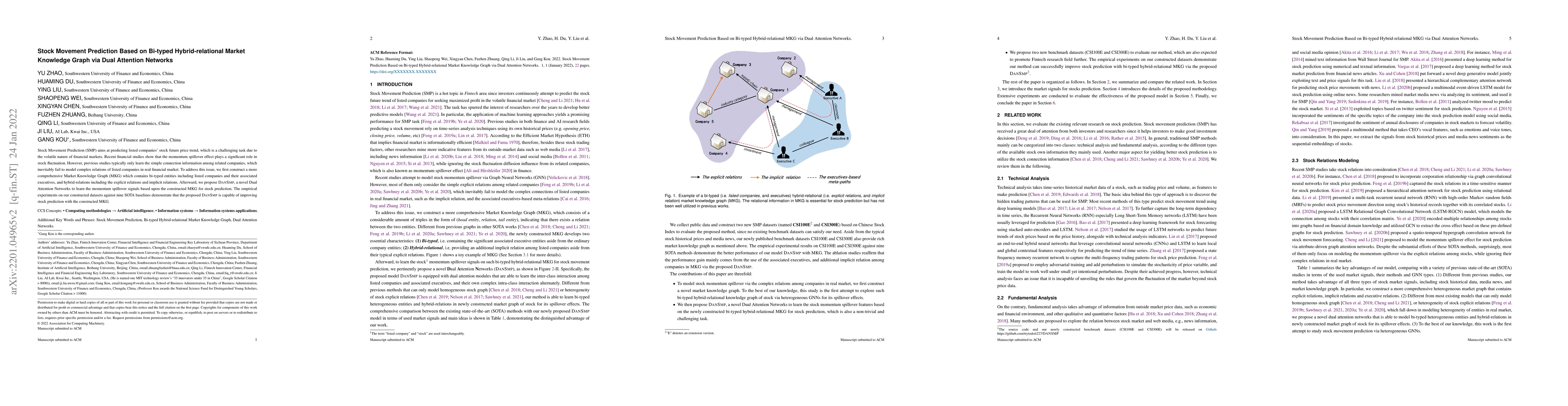

Stock Movement Prediction (SMP) aims at predicting listed companies' stock future price trend, which is a challenging task due to the volatile nature of financial markets. Recent financial studies show that the momentum spillover effect plays a significant role in stock fluctuation. However, previous studies typically only learn the simple connection information among related companies, which inevitably fail to model complex relations of listed companies in the real financial market. To address this issue, we first construct a more comprehensive Market Knowledge Graph (MKG) which contains bi-typed entities including listed companies and their associated executives, and hybrid-relations including the explicit relations and implicit relations. Afterward, we propose DanSmp, a novel Dual Attention Networks to learn the momentum spillover signals based upon the constructed MKG for stock prediction. The empirical experiments on our constructed datasets against nine SOTA baselines demonstrate that the proposed DanSmp is capable of improving stock prediction with the constructed MKG.

AI Key Findings

Generated Sep 03, 2025

Methodology

The research constructs a Bi-typed Hybrid-relational Market Knowledge Graph (MKG) incorporating listed companies and their executives with explicit and implicit relations. It then proposes Dual Attention Networks (DANSMP) to learn momentum spillover signals from this MKG for stock movement prediction.

Key Results

- DANSMP outperforms nine state-of-the-art (SOTA) baselines on constructed datasets in terms of Accuracy, AUC, Directional Accuracy, and Precision.

- Empirical experiments demonstrate that DANSMP improves stock prediction by effectively modeling complex relations in the real financial market.

Significance

This research is significant as it addresses the challenge of modeling complex relations in financial markets for stock movement prediction, which previous studies have inadequately handled.

Technical Contribution

The paper introduces a novel Bi-typed Hybrid-relational MKG and a Dual Attention Networks (DANSMP) framework for stock movement prediction, effectively capturing complex relations and momentum spillover effects.

Novelty

The proposed method distinguishes itself by integrating bi-typed entities (companies and executives) and hybrid relations (explicit and implicit) into a single MKG, and by employing Dual Attention Networks to learn spillover signals for stock prediction.

Limitations

- The study relies on data from China's financial market, limiting its generalizability to other markets.

- The model's performance may vary with changes in market dynamics or the introduction of new types of relations.

Future Work

- Exploring the impact of additional executive-related information from news and social media on stock prediction.

- Investigating the model's performance on other stock market datasets from different geographical regions.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersLearning Bi-typed Multi-relational Heterogeneous Graph via Dual Hierarchical Attention Networks

Qing Li, Ji Liu, Yu Zhao et al.

Graph-Based Learning for Stock Movement Prediction with Textual and Relational Data

Christian-Yann Robert, Qinkai Chen

FinMamba: Market-Aware Graph Enhanced Multi-Level Mamba for Stock Movement Prediction

Yifan Hu, Shu-Tao Xia, Tao Dai et al.

| Title | Authors | Year | Actions |

|---|

Comments (0)