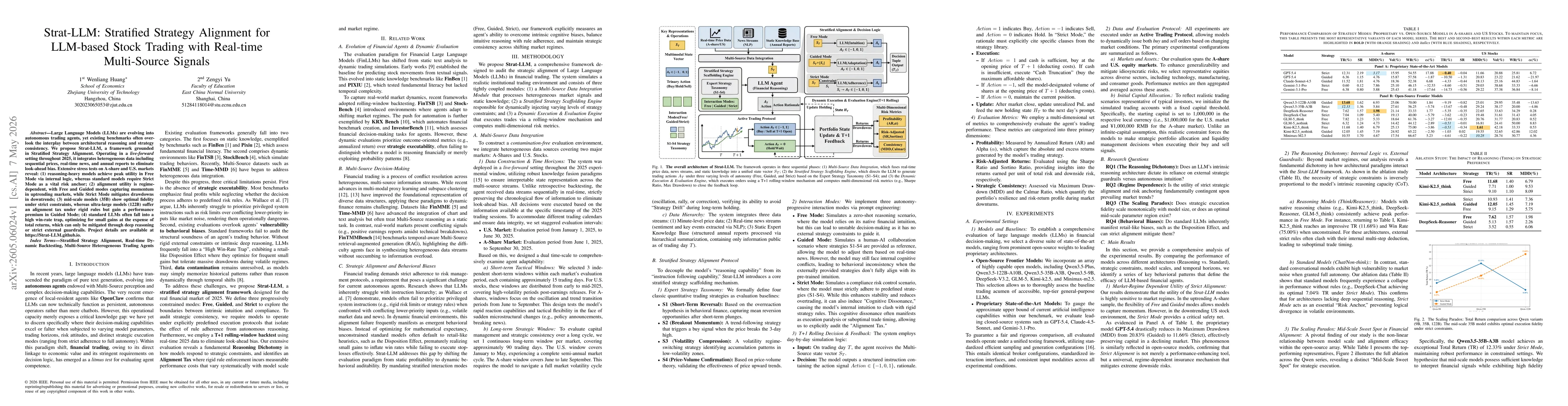

Large Language Models (LLMs) are evolving into autonomous trading agents, yet existing benchmarks often overlook the interplay between architectural reasoning and strategy consistency. We propose Strat-LLM, a framework grounded in Stratified Strategy Alignment. Operating in a live-forward setting throughout 2025, it integrates heterogeneous data including sequential prices, real-time news, and annual reports to eliminate look-ahead bias. Extensive stress tests on A-share and U.S. markets reveal: (1) reasoning-heavy models achieve peak utility in Free Mode via internal logic, whereas standard models require Strict Mode as a vital risk anchor; (2) alignment utility is regime-dependent, with Free and Guided modes capturing momentum in uptrending markets, while Strict Mode mitigates drawdowns in downtrends; (3) mid-scale models (35B) show optimal fidelity under strict constraints, whereas ultra-large models (122B) suffer an alignment tax under rigid rules but gain a performance premium in Guided Mode; (4) standard LLMs often fall into a high win-rate trap, optimizing for small gains at the expense of total returns, which can only be mitigated through deep reasoning or strict external guardrails. Project details are available at https://Strat-LLM.github.io.

Discussion 0