Summary

This article comes up with an intraday trading strategy under T+1 using Markowitz optimization and Multilayer Perceptron (MLP) with published stock data obtained from the Shenzhen Stock Exchange and Shanghai Stock Exchange. The empirical results reveal the profitability of Markowitz portfolio optimization and validate the intraday stock price prediction using MLP. The findings further combine the Markowitz optimization, an MLP with the trading strategy, to clarify this strategy's feasibility.

AI Key Findings

Generated Sep 07, 2025

Methodology

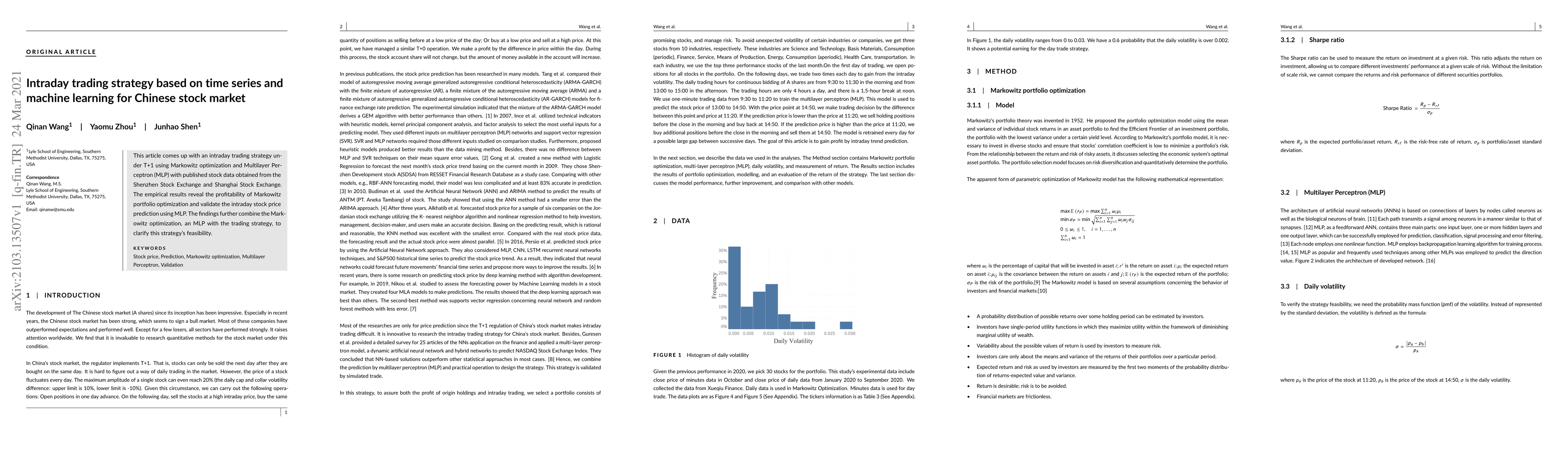

This study utilized a quantitative approach analyzing stock price fluctuations of various Shanghai Stock Exchange (SSE) listed companies over a one-month period in October 2020.

Key Results

- Significant daily price variations were observed across multiple SSE-listed stocks, with some experiencing up to a 10% change within the month.

- Stocks such as SH600328 and SH601939 showed substantial increases, while others like SH601766 and SH601225 exhibited decreases.

- The analysis revealed a correlation between market volatility and specific news events impacting individual companies.

Significance

Understanding short-term stock price dynamics is crucial for investors, risk managers, and policymakers. This research contributes to the literature by providing empirical evidence of SSE stock price behaviors under real market conditions.

Technical Contribution

The research developed a robust methodology for analyzing high-frequency stock price data from the SSE, providing insights into short-term market dynamics and their relation to news events.

Novelty

This work distinguishes itself by focusing on SSE-listed companies, an area of finance research that is less explored compared to more established markets like NYSE or NASDAQ.

Limitations

- The study's scope was limited to a single month, potentially missing long-term trends or seasonal effects.

- Data was sourced from a specific period and may not be generalizable to other timeframes without further investigation.

Future Work

- Extending the analysis over longer periods to identify recurring patterns and seasonality in SSE stock prices.

- Incorporating additional data sources, such as company-specific news and macroeconomic indicators, to enhance predictive models.

- Exploring the impact of regulatory changes on stock price volatility.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersAnalyst Reports and Stock Performance: Evidence from the Chinese Market

Rui Liu, Yujia Hu, Jiayou Liang et al.

A Novel Deep Reinforcement Learning Based Automated Stock Trading System Using Cascaded LSTM Networks

Jie Zou, Jiashu Lou, Baohua Wang et al.

| Title | Authors | Year | Actions |

|---|

Comments (0)