We consider forecasting a single time series when there is a large number of

predictors and a possible nonlinear effect. The dimensionality was first

reduced via a high-dimensional (approximate) factor model implemented by the

principal component analysis. Using the extracted factors, we develop a novel

forecasting method called the sufficient forecasting, which provides a set of

sufficient predictive indices, inferred from high-dimensional predictors, to

deliver additional predictive power. The projected principal component analysis

will be employed to enhance the accuracy of inferred factors when a

semi-parametric (approximate) factor model is assumed. Our method is also

applicable to cross-sectional sufficient regression using extracted factors.

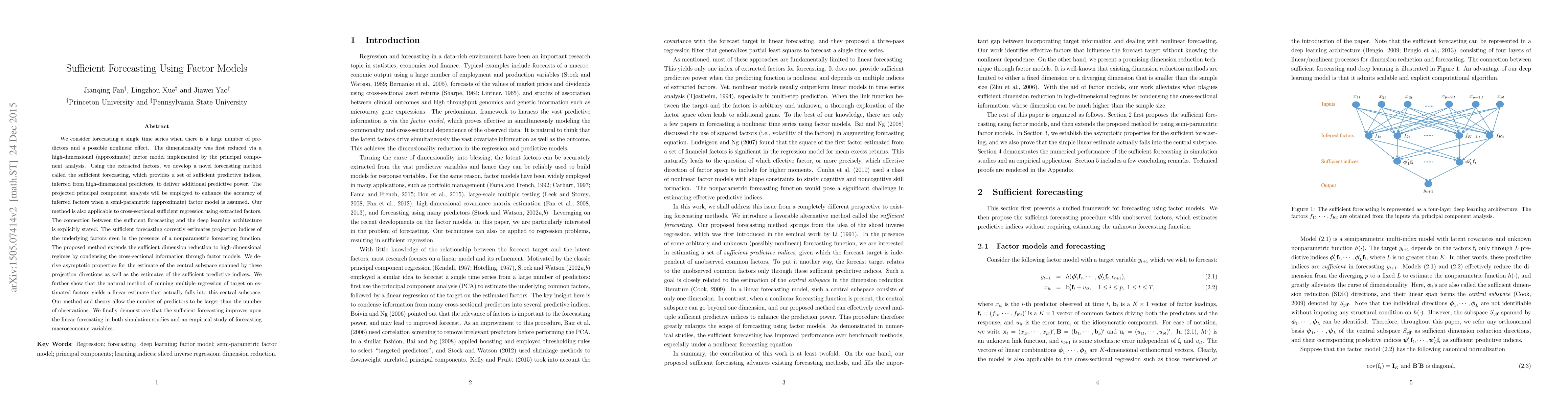

The connection between the sufficient forecasting and the deep learning

architecture is explicitly stated. The sufficient forecasting correctly

estimates projection indices of the underlying factors even in the presence of

a nonparametric forecasting function. The proposed method extends the

sufficient dimension reduction to high-dimensional regimes by condensing the

cross-sectional information through factor models. We derive asymptotic

properties for the estimate of the central subspace spanned by these projection

directions as well as the estimates of the sufficient predictive indices. We

further show that the natural method of running multiple regression of target

on estimated factors yields a linear estimate that actually falls into this

central subspace. Our method and theory allow the number of predictors to be

larger than the number of observations. We finally demonstrate that the

sufficient forecasting improves upon the linear forecasting in both simulation

studies and an empirical study of forecasting macroeconomic variables.

Discussion 0