Publication

Metrics

AI Quick Summary

This paper proposes a temporal attention augmented bilinear network for financial time-series forecasting, which combines bilinear projection with an attention mechanism to highlight crucial temporal information. The resulting network outperforms existing models in High-Frequency Trading forecasting, achieving better accuracy with fewer computations.

Paper Preview

Abstract

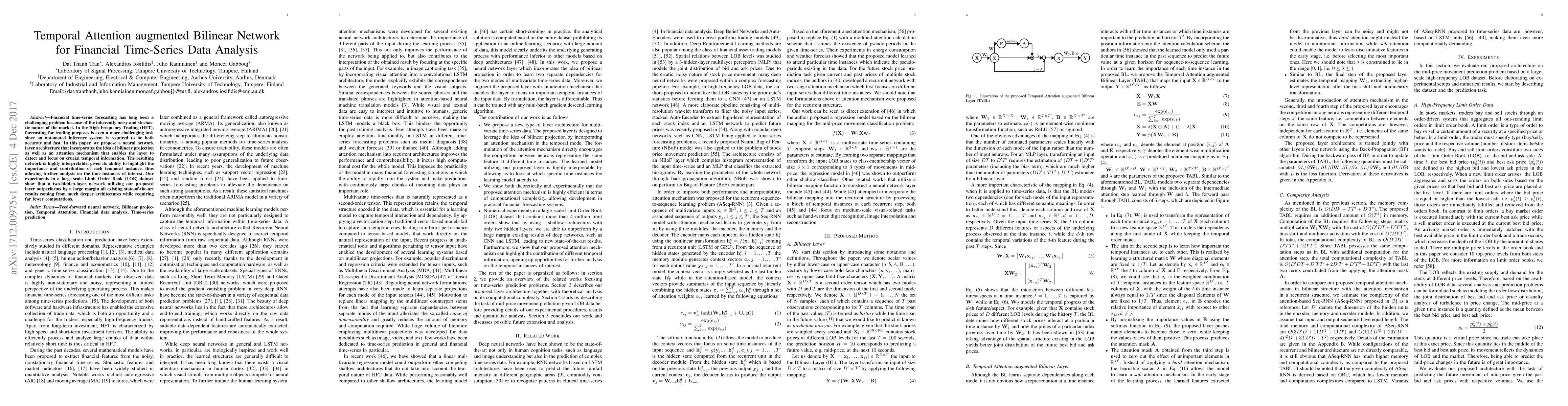

Financial time-series forecasting has long been a challenging problem because of the inherently noisy and stochastic nature of the market. In the High-Frequency Trading (HFT), forecasting for trading purposes is even a more challenging task since an automated inference system is required to be both accurate and fast. In this paper, we propose a neural network layer architecture that incorporates the idea of bilinear projection as well as an attention mechanism that enables the layer to detect and focus on crucial temporal information. The resulting network is highly interpretable, given its ability to highlight the importance and contribution of each temporal instance, thus allowing further analysis on the time instances of interest. Our experiments in a large-scale Limit Order Book (LOB) dataset show that a two-hidden-layer network utilizing our proposed layer outperforms by a large margin all existing state-of-the-art results coming from much deeper architectures while requiring far fewer computations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0