01

MethodologyHow they did it

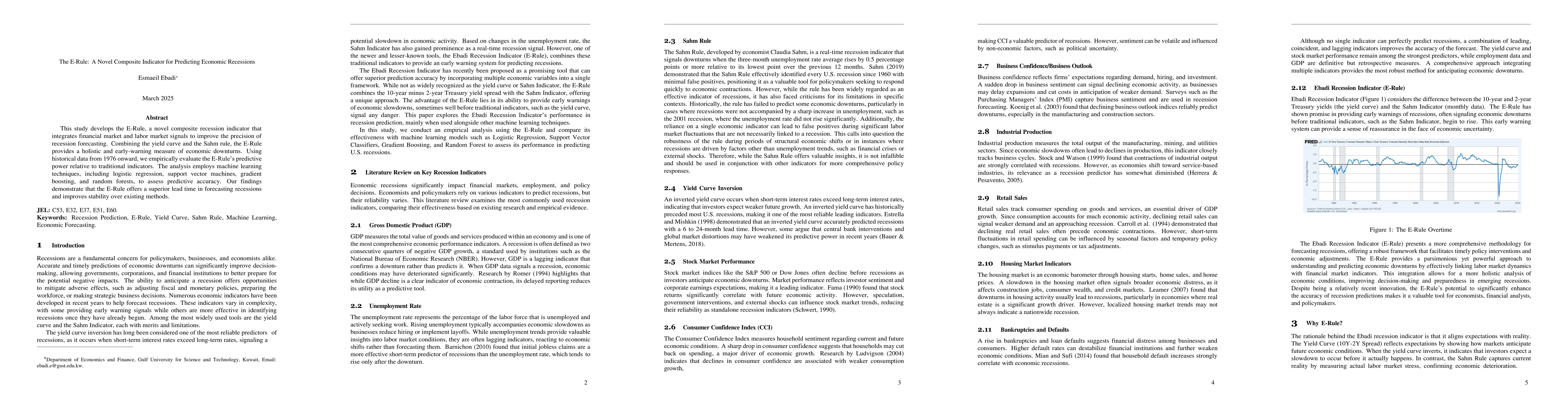

This study develops the E-Rule, a composite recession indicator integrating financial market signals (yield curve) and labor market stress measures (Sahm Rule), using historical data from 1976 and machine learning techniques like logistic regression, support vector machines, gradient boosting, and random forests.

Discussion 0