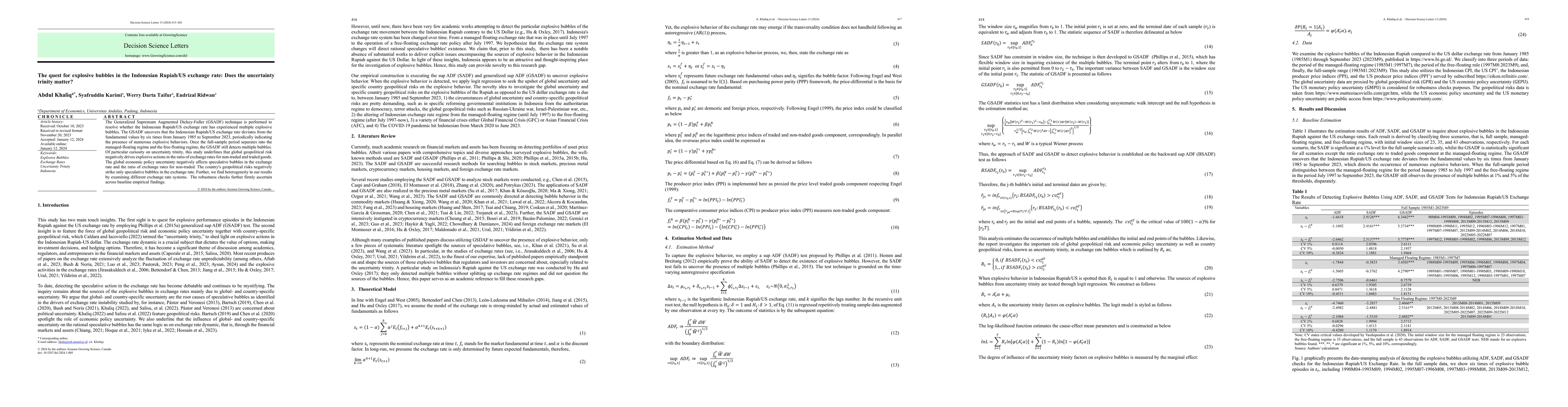

The Generalized Supremum Augmented Dickey-Fuller (GSADF) technique is

performed to resolve whether the Indonesian Rupiah/US exchange rate has

experienced multiple explosive bubbles. The GSADF uncovers that the Indonesian

Rupiah/US exchange rate deviates from the fundamental values by six times from

January 1985 to September 2023, periodically indicating the presence of

numerous explosive behaviors. Once the full-sample period separates into the

managed-floating regime and the free-floating regime, the GSADF still detects

multiple bubbles. Of particular curiosity on uncertainty trinity, this study

underlines that global geopolitical risk negatively drives explosive actions in

the ratio of exchange rates for non-traded and traded goods. The global

economic policy uncertainty negatively affects speculative bubbles in the

exchange rate and the ratio of exchange rates for non-traded. The country's

geopolitical risks negatively strike only speculative bubbles in the exchange

rate. Further, we find heterogeneity in our results by examining different

exchange rate systems. The robustness checks further firmly ascertain across

baseline empirical findings.

Discussion 0