TimeRAG: BOOSTING LLM Time Series Forecasting via Retrieval-Augmented Generation

Publication

Metrics

AI Quick Summary

TimeRAG enhances LLM-based time series forecasting by using Retrieval-Augmented Generation (RAG) to create a knowledge base of historical sequences, retrieve similar patterns via Dynamic Time Warping, and improve forecast accuracy by 2.97% on average.

Paper Preview

Abstract

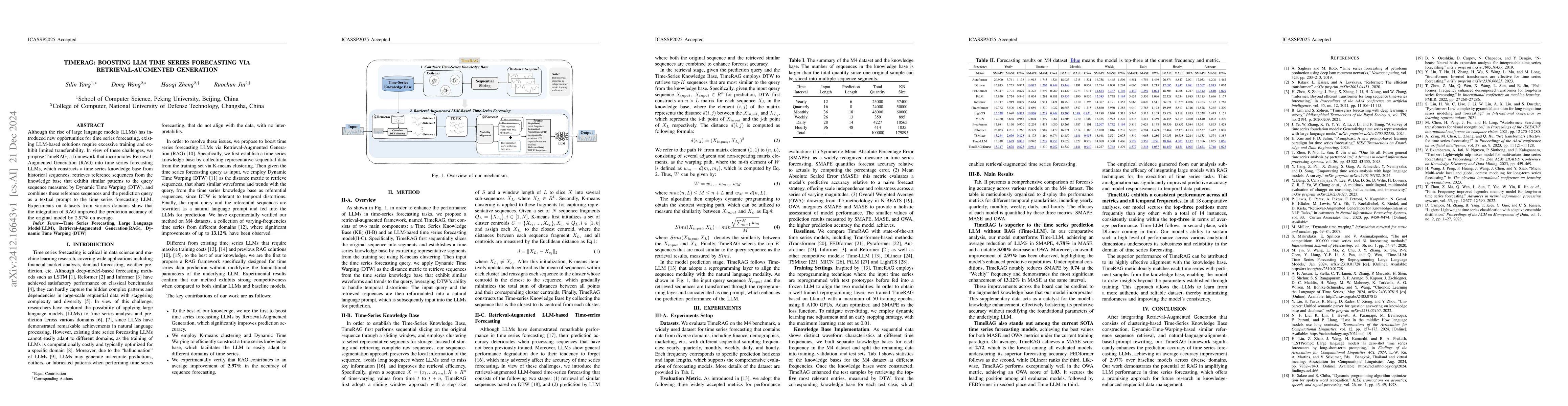

Although the rise of large language models (LLMs) has introduced new opportunities for time series forecasting, existing LLM-based solutions require excessive training and exhibit limited transferability. In view of these challenges, we propose TimeRAG, a framework that incorporates Retrieval-Augmented Generation (RAG) into time series forecasting LLMs, which constructs a time series knowledge base from historical sequences, retrieves reference sequences from the knowledge base that exhibit similar patterns to the query sequence measured by Dynamic Time Warping (DTW), and combines these reference sequences and the prediction query as a textual prompt to the time series forecasting LLM. Experiments on datasets from various domains show that the integration of RAG improved the prediction accuracy of the original model by 2.97% on average.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0