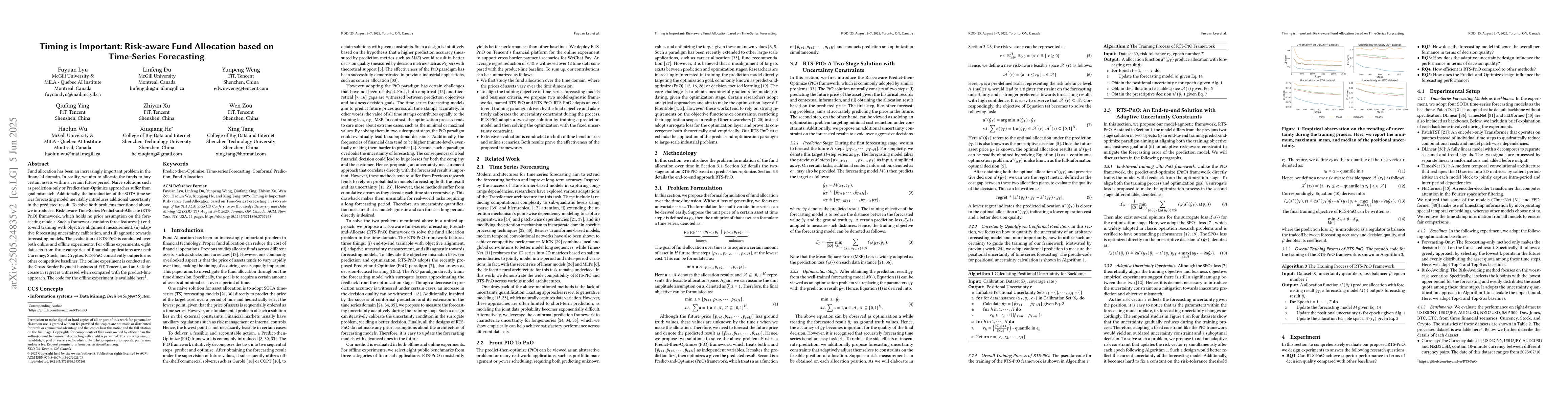

Fund allocation has been an increasingly important problem in the financial

domain. In reality, we aim to allocate the funds to buy certain assets within a

certain future period. Naive solutions such as prediction-only or

Predict-then-Optimize approaches suffer from goal mismatch. Additionally, the

introduction of the SOTA time series forecasting model inevitably introduces

additional uncertainty in the predicted result. To solve both problems

mentioned above, we introduce a Risk-aware Time-Series Predict-and-Allocate

(RTS-PnO) framework, which holds no prior assumption on the forecasting models.

Such a framework contains three features: (i) end-to-end training with

objective alignment measurement, (ii) adaptive forecasting uncertainty

calibration, and (iii) agnostic towards forecasting models. The evaluation of

RTS-PnO is conducted over both online and offline experiments. For offline

experiments, eight datasets from three categories of financial applications are

used: Currency, Stock, and Cryptos. RTS-PnO consistently outperforms other

competitive baselines. The online experiment is conducted on the Cross-Border

Payment business at FiT, Tencent, and an 8.4\% decrease in regret is witnessed

when compared with the product-line approach. The code for the offline

experiment is available at https://github.com/fuyuanlyu/RTS-PnO.

Discussion 0