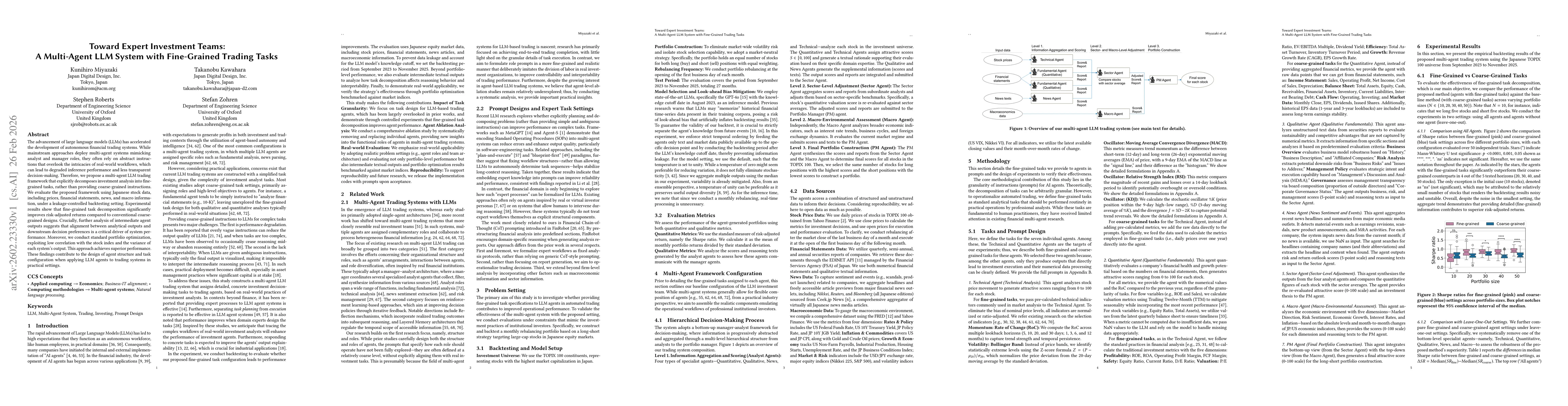

The advancement of large language models (LLMs) has accelerated the development of autonomous financial trading systems. While mainstream approaches deploy multi-agent systems mimicking analyst and manager roles, they often rely on abstract instructions that overlook the intricacies of real-world workflows, which can lead to degraded inference performance and less transparent decision-making. Therefore, we propose a multi-agent LLM trading framework that explicitly decomposes investment analysis into fine-grained tasks, rather than providing coarse-grained instructions. We evaluate the proposed framework using Japanese stock data, including prices, financial statements, news, and macro information, under a leakage-controlled backtesting setting. Experimental results show that fine-grained task decomposition significantly improves risk-adjusted returns compared to conventional coarse-grained designs. Crucially, further analysis of intermediate agent outputs suggests that alignment between analytical outputs and downstream decision preferences is a critical driver of system performance. Moreover, we conduct standard portfolio optimization, exploiting low correlation with the stock index and the variance of each system's output. This approach achieves superior performance. These findings contribute to the design of agent structure and task configuration when applying LLM agents to trading systems in practical settings.

Discussion 0