Time series forecasting enables early warning and has driven asset performance management from traditional planned maintenance to predictive maintenance. However, the lack of interpretability in forecasting methods undermines users' trust and complicates debugging for developers. Consequently, interpretable time-series forecasting has attracted increasing research attention. Nevertheless, existing methods suffer from several limitations, including insufficient modeling of temporal dependencies, lack of feature-level interpretability to support early warning, and difficulty in simultaneously achieving the accuracy and interpretability. This paper proposes the interpretable polynomial learning (IPL) method, which integrates interpretability into the model structure by explicitly modeling original features and their interactions of arbitrary order through polynomial representations. This design preserves temporal dependencies, provides feature-level interpretability, and offers a flexible trade-off between prediction accuracy and interpretability by adjusting the polynomial degree. We evaluate IPL on simulated and Bitcoin price data, showing that it achieves high prediction accuracy with superior interpretability compared with widely used explainability methods. Experiments on field-collected antenna data further demonstrate that IPL yields simpler and more efficient early warning mechanisms.

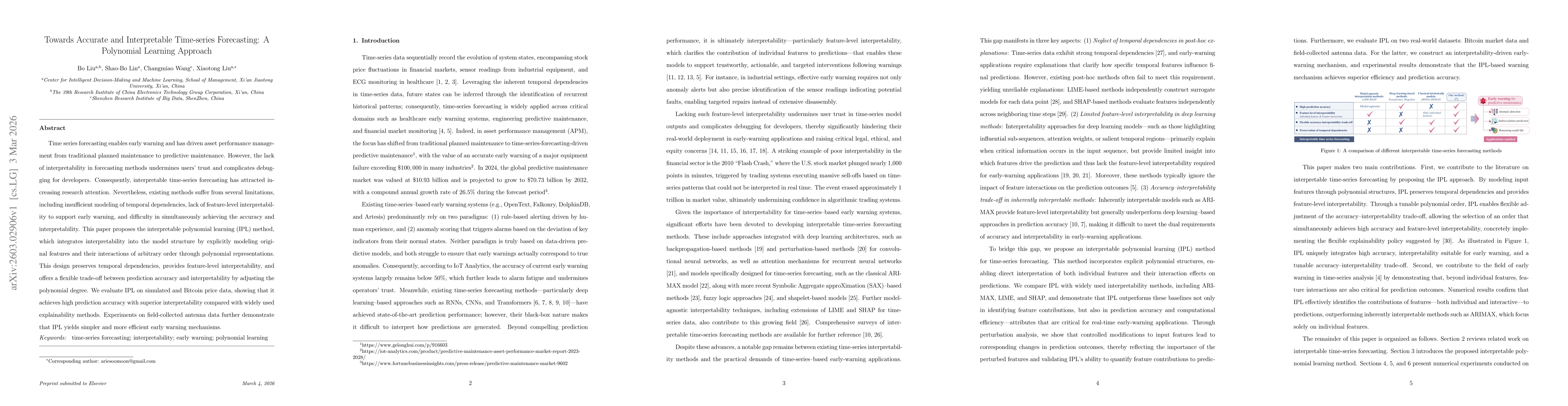

Discussion 0