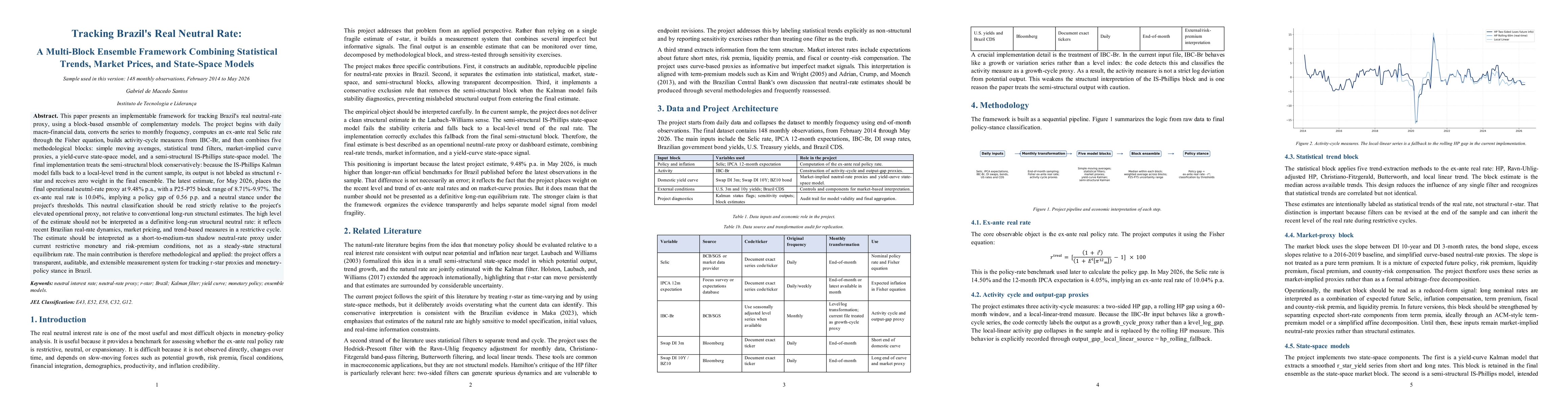

This paper presents an implementable framework for tracking Brazil's real neutral-rate proxy, using a block-based ensemble of complementary models. The project begins with daily macro-financial data, converts the series to monthly frequency, computes an ex-ante real Selic rate through the Fisher equation, builds activity-cycle measures from IBC-Br, and then combines five methodological blocks: simple moving averages, statistical trend filters, market-implied curve proxies, a yield-curve state-space model, and a semi-structural IS-Phillips state-space model. The final implementation treats the semi-structural block conservatively: because the IS-Phillips Kalman model falls back to a local-level trend in the current sample, its output is not labeled as structural r-star and receives zero weight in the final ensemble. The latest estimate, for May 2026, places the final operational neutral-rate proxy at 9.48% p.a., with a P25-P75 block range of 8.71%-9.97%. The ex-ante real rate is 10.04%, implying a policy gap of 0.56 p.p. and a neutral stance under the project's thresholds. This neutral classification should be read strictly relative to the project's elevated operational proxy, not relative to conventional long-run structural estimates. The high level of the estimate should not be interpreted as a definitive long-run structural neutral rate: it reflects recent Brazilian real-rate dynamics, market pricing, and trend-based measures in a restrictive cycle. The estimate should be interpreted as a short-to-medium-run shadow neutral-rate proxy under current restrictive monetary and risk-premium conditions, not as a steady-state structural equilibrium rate. The main contribution is therefore methodological and applied: the project offers a transparent, auditable, and extensible measurement system for tracking r-star proxies and monetary-policy stance in Brazil.

Discussion 0