Publication

Metrics

Paper Preview

Abstract

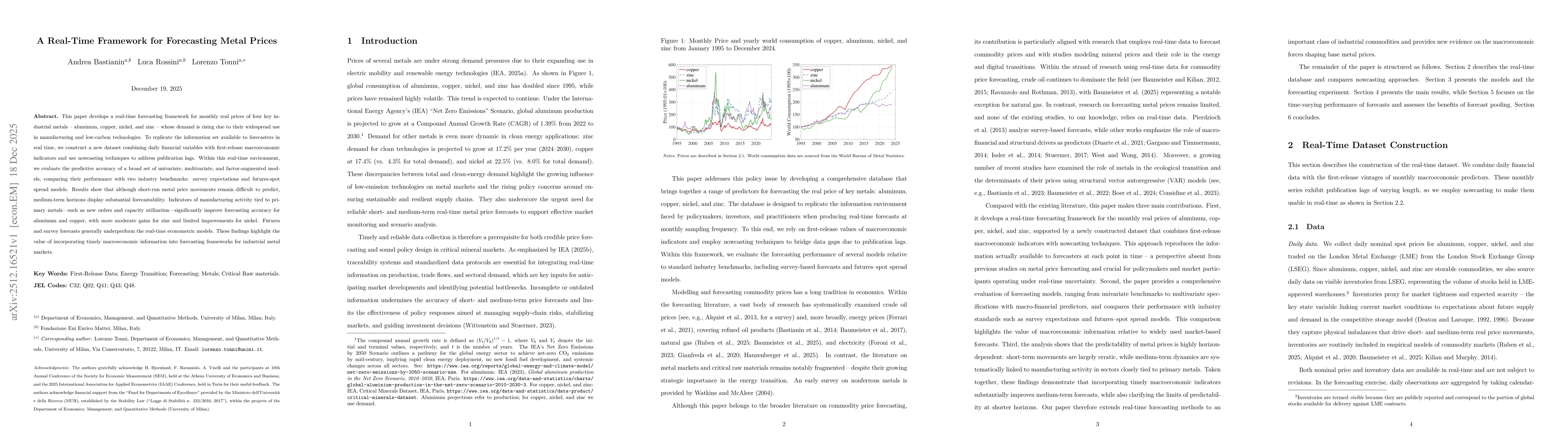

This paper develops a real-time forecasting framework for the monthly real prices of four key industrial metals -- aluminum, copper, nickel, and zinc -- whose demand is rising due to their widespread use in manufacturing and low-carbon technologies. To replicate the information set available to forecasters in real time, we construct a new dataset combining daily financial variables with first-release macroeconomic indicators and use nowcasting techniques to address publication lags. Within this real-time environment, we evaluate the predictive accuracy of a broad set of univariate, multivariate, and factor-augmented models, comparing their performance with two industry benchmarks: survey expectations and futures-spot spread models. Results show that although short-run metal price movements remain difficult to predict, medium-term horizons display substantial forecastability. Indicators of manufacturing activity tied to primary metals -- such as new orders and capacity utilization -- significantly improve forecasting accuracy for aluminum and copper, with more moderate gains for zinc and limited improvements for nickel. Futures and survey forecasts generally underperform the real-time econometric models. These findings highlight the value of incorporating timely macroeconomic information into forecasting frameworks for industrial metal markets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0