Academic Profile

Statistics

Similar Authors

Papers on arXiv

Enabling robots to autonomously perform hybrid motions in diverse environments can be beneficial for long-horizon tasks such as material handling, household chores, and work assistance. This requires ...

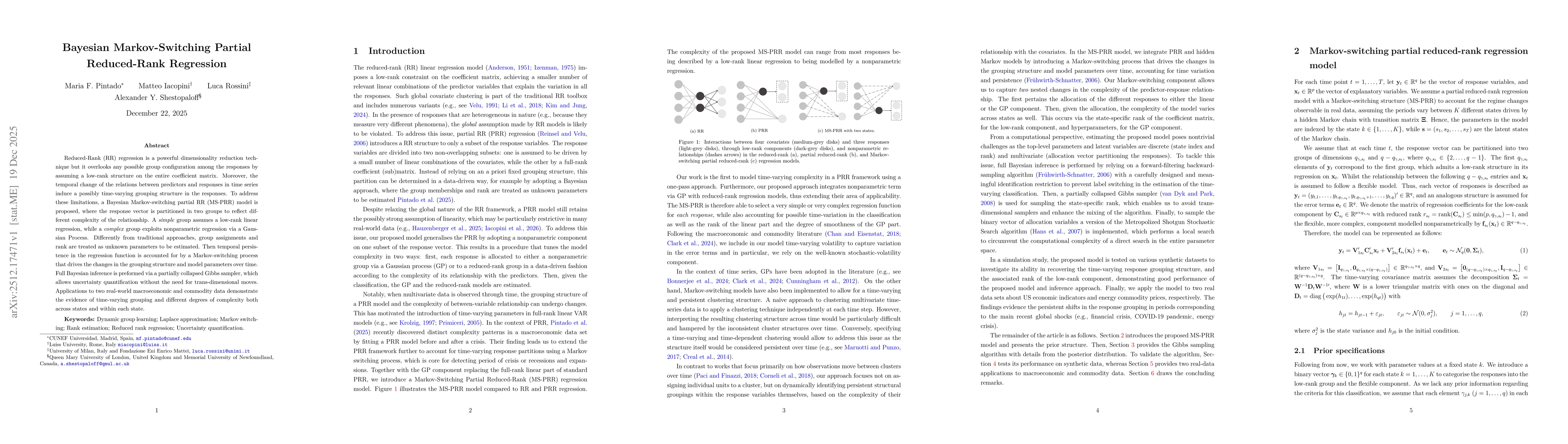

Reduced-rank (RR) regression may be interpreted as a dimensionality reduction technique able to reveal complex relationships among the data parsimoniously. However, RR regression models typically ov...

We consider forecast comparison in the presence of instability when this affects only a short period of time. We demonstrate that global tests do not perform well in this case, as they were not desi...

Putting a price on carbon -- with taxes or developing carbon markets -- is a widely used policy measure to achieve the target of net-zero emissions by 2050. This paper tackles the issue of producing...

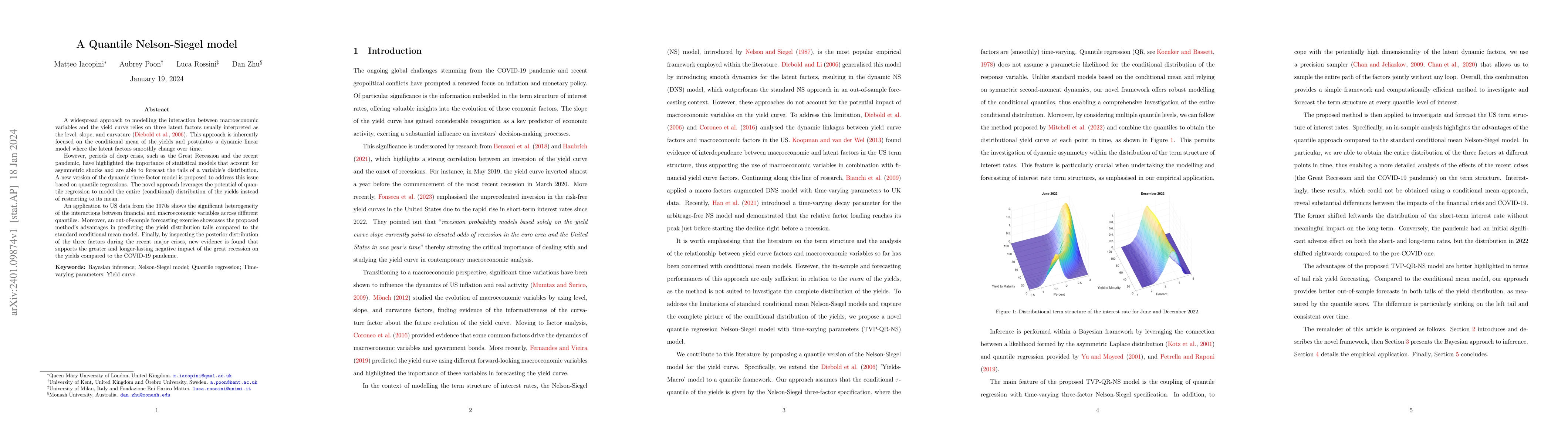

A widespread approach to modelling the interaction between macroeconomic variables and the yield curve relies on three latent factors usually interpreted as the level, slope, and curvature (Diebold ...

Ranking lists are often provided at regular time intervals by one or multiple rankers in a range of applications, including sports, marketing, and politics. Most popular methods for rank-order data ...

An innovative method is proposed to construct a quantile dependence system for inflation and money growth. By considering all quantiles and leveraging a novel notion of quantile sensitivity, the met...

Reduced-rank regression recognises the possibility of a rank-deficient matrix of coefficients. We propose a novel Bayesian model for estimating the rank of the coefficient matrix, which obviates the...

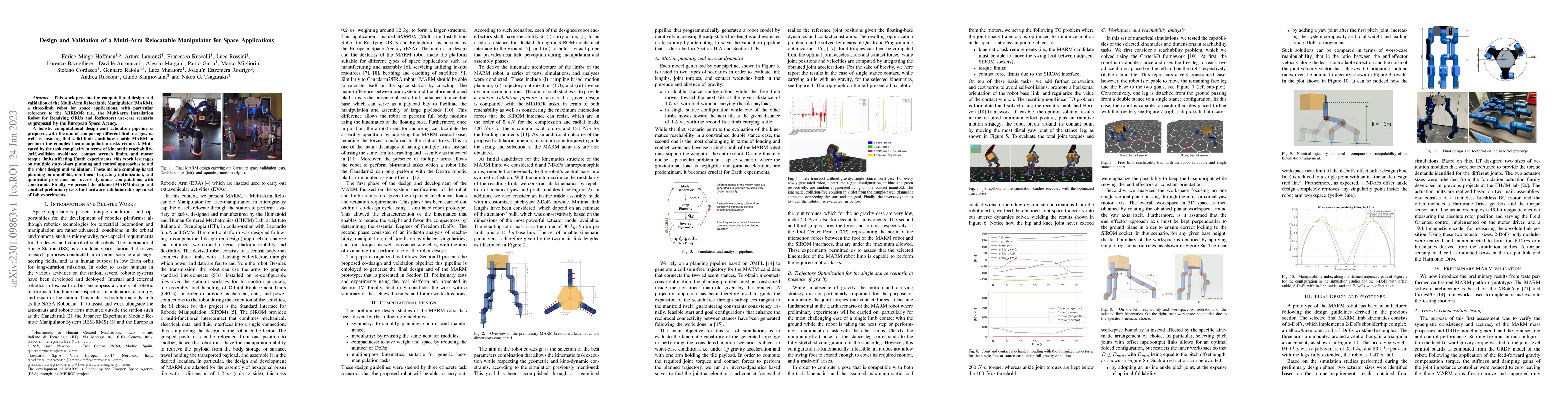

This work presents the computational design and validation of the Multi-Arm Relocatable Manipulator (MARM), a three-limb robot for space applications, with particular reference to the MIRROR (i.e., ...

This article proposes a novel Bayesian multivariate quantile regression to forecast the tail behavior of US macro and financial indicators, where the homoskedasticity assumption is relaxed to allow ...

Timely characterizations of risks in economic and financial systems play an essential role in both economic policy and private sector decisions. However, the informational content of low-frequency v...

The deployment of robots within realistic environments requires the capability to plan and refine the loco-manipulation trajectories on the fly to avoid unexpected interactions with a dynamic enviro...

This paper examines the dependence between electricity prices, demand, and renewable energy sources by means of a multivariate copula model {while studying Germany, the widest studied market in Euro...

Motivated by the proliferation of extensive macroeconomic and health datasets necessitating accurate forecasts, a novel approach is introduced to address Vector Autoregressive (VAR) models. This app...

In this paper we propose a time-varying parameter (TVP) vector error correction model (VECM) with heteroskedastic disturbances. We propose tools to carry out dynamic model specification in an automa...

Recent research finds that forecasting electricity prices is very relevant. In many applications, it might be interesting to predict daily electricity prices by using their own lags or renewable ene...

Vector autoregressive (VAR) models assume linearity between the endogenous variables and their lags. This assumption might be overly restrictive and could have a deleterious impact on forecasting ac...

This paper proposes a novel asymmetric continuous probabilistic score (ACPS) for evaluating and comparing density forecasts. It extends the proposed score and defines a weighted version, which empha...

This paper studies the forecasting ability of cryptocurrency time series. This study is about the four most capitalized cryptocurrencies: Bitcoin, Ethereum, Litecoin and Ripple. Different Bayesian m...

Over the last decade, big data have poured into econometrics, demanding new statistical methods for analysing high-dimensional data and complex non-linear relationships. A common approach for addres...

In recent years, artificial feet based on soft robotics and under-actuation principles emerged to improve mobility on challenging terrains. This paper presents the application of the MuJoCo physics en...

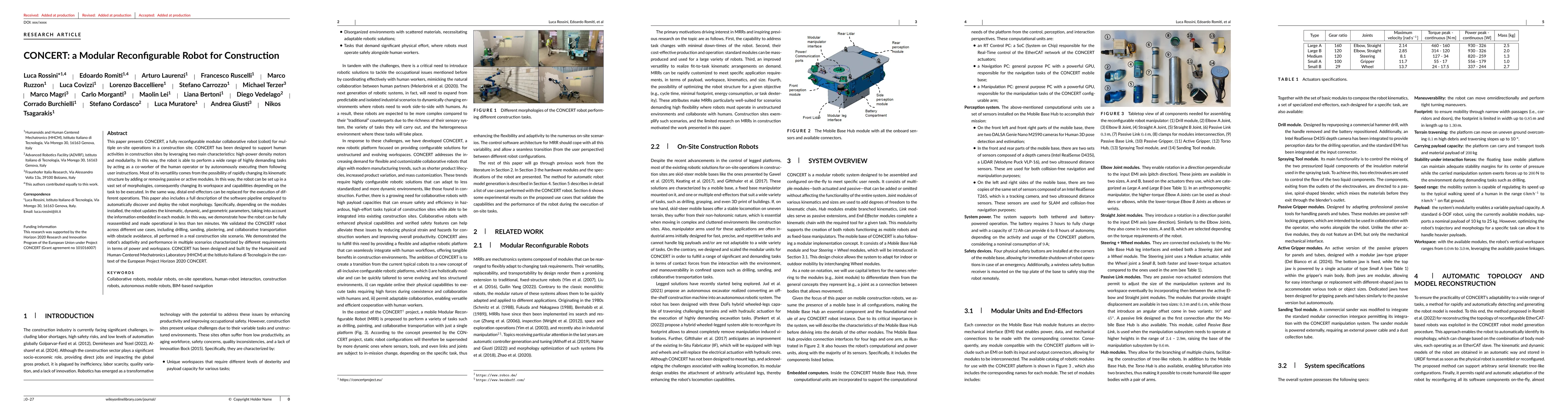

This paper presents CONCERT, a fully reconfigurable modular collaborative robot (cobot) for multiple on-site operations in a construction site. CONCERT has been designed to support human activities in...

Adaptive recovery from fall incidents are essential skills for the practical deployment of wheeled-legged robots, which uniquely combine the agility of legs with the speed of wheels for rapid recovery...

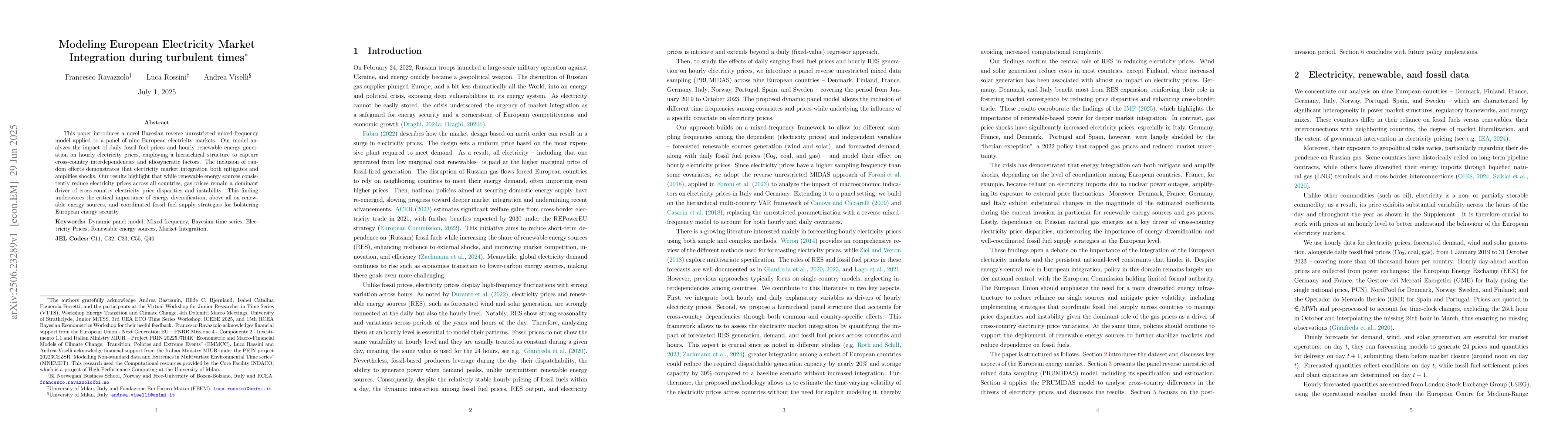

This paper introduces a novel Bayesian reverse unrestricted mixed-frequency model applied to a panel of nine European electricity markets. Our model analyzes the impact of daily fossil fuel prices and...

Infinite hidden Markov models provide a flexible framework for modelling time series with structural changes and complex dynamics, without requiring the number of latent states to be specified in adva...

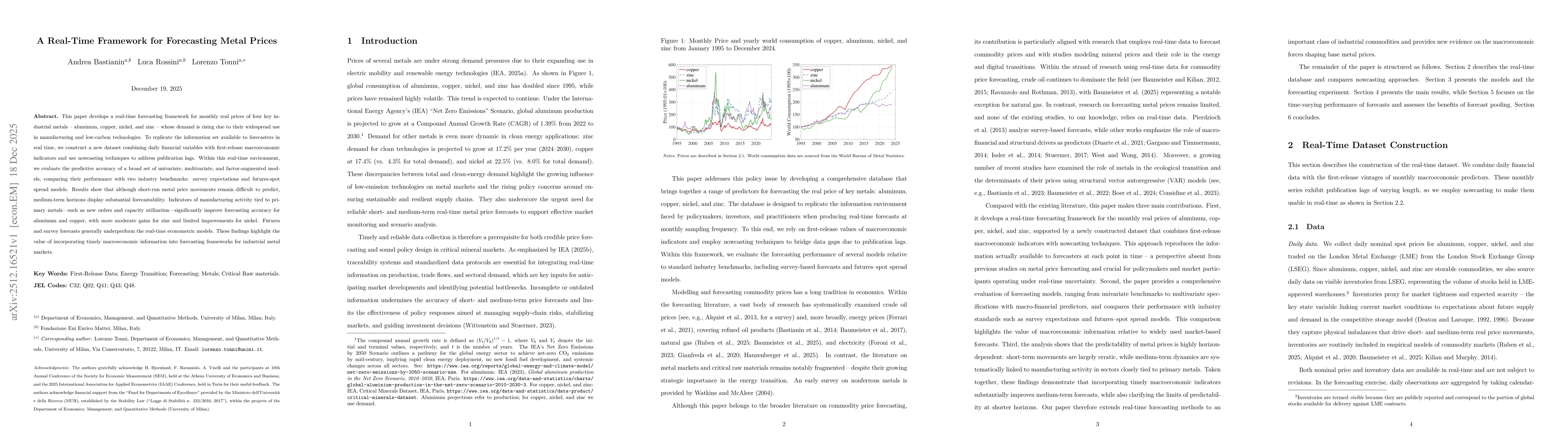

This paper develops a real-time forecasting framework for the monthly real prices of four key industrial metals -- aluminum, copper, nickel, and zinc -- whose demand is rising due to their widespread ...

Reduced-Rank (RR) regression is a powerful dimensionality reduction technique but it overlooks any possible group configuration among the responses by assuming a low-rank structure on the entire coeff...

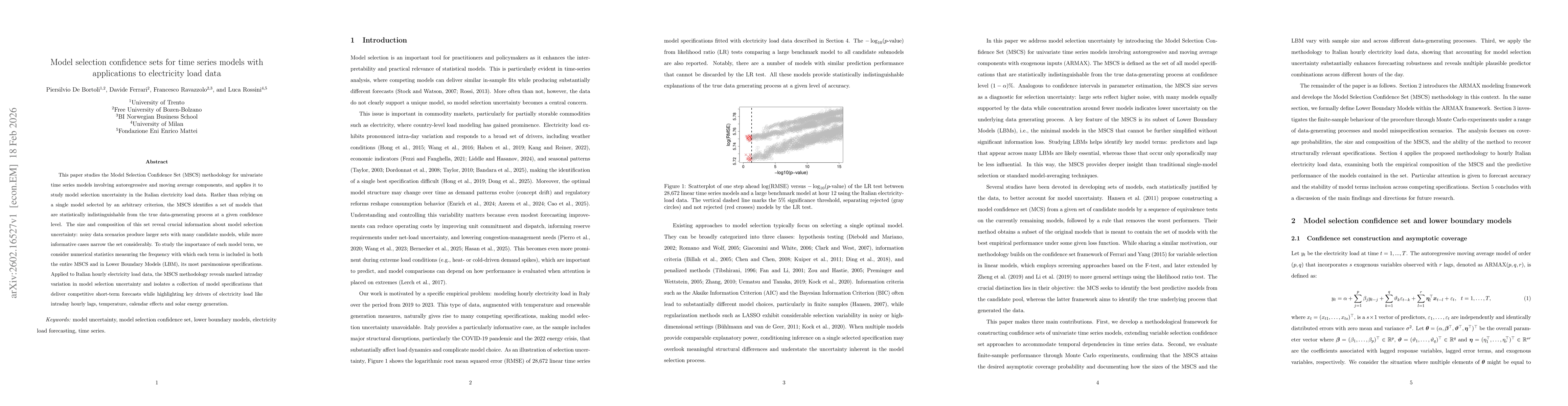

This paper studies the Model Selection Confidence Set (MSCS) methodology for univariate time series models involving autoregressive and moving average components, and applies it to study model selecti...

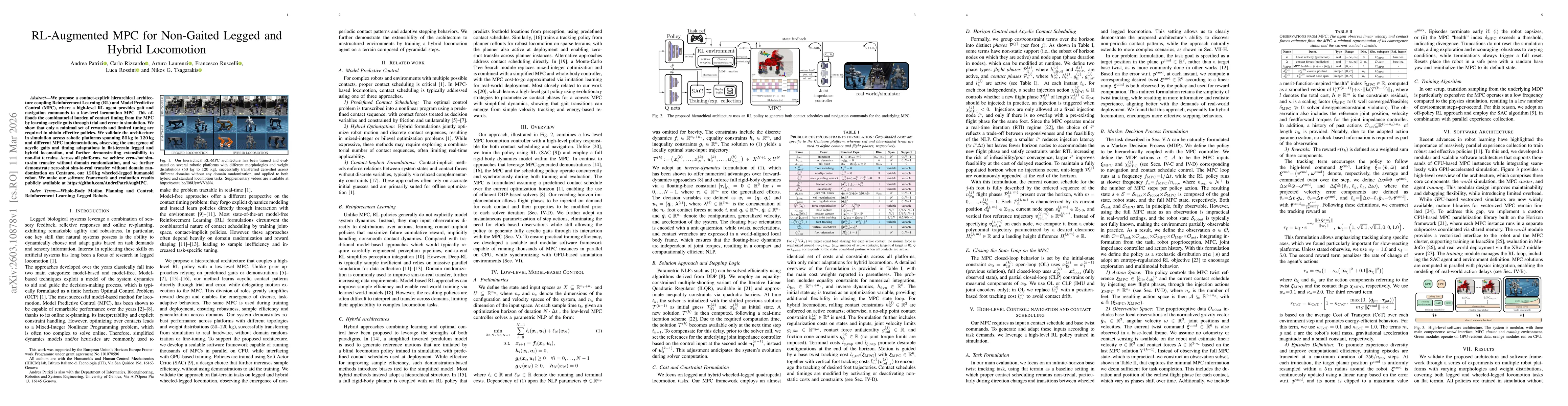

We propose a contact-explicit hierarchical architecture coupling Reinforcement Learning (RL) and Model Predictive Control (MPC), where a high-level RL agent provides gait and navigation commands to a ...

We use web search data to construct monthly indexes of derived demand for cobalt, copper, and nickel, which are key inputs in technologies driving the energy and digital transitions. We incorporate th...

This paper presents KYON, a hybrid wheel-legged quadruped robot equipped with a bimanual upper body for loco-manipulation tasks. The platform features a semi-modular design with a reconfigurable lower...

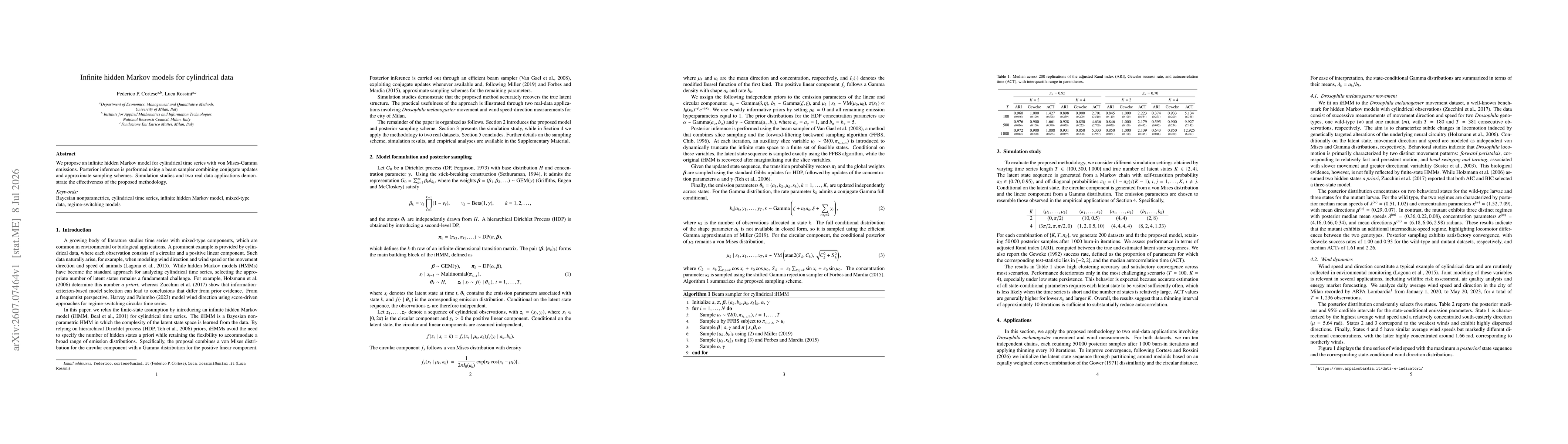

We propose an infinite hidden Markov model for cylindrical time series with von Mises-Gamma emissions. Posterior inference is performed using a beam sampler combining conjugate updates and approximate...