In classical canonical correlation analysis (CCA), the goal is to determine

the linear transformations of two random vectors into two new random variables

that are most strongly correlated. Canonical variables are pairs of these new

random variables, while canonical correlations are correlations between these

pairs. In this paper, we propose and study two generalizations of this

classical method:

(1) Instead of two random vectors we study more complex data structures that

appear in important applications. In these structures, there are $L$ features,

each described by $p_l$ scalars, $1 \le l \le L$. We observe $n$ such objects

over $T$ time points. We derive a suitable analog of the CCA for such data. Our

approach relies on embeddings into Reproducing Kernel Hilbert Spaces, and

covers several related data structures as well.

(2) We develop an analogous approach for multidimensional random processes.

In this case, the experimental units are multivariate continuous,

square-integrable functions over a given interval. These functions are modeled

as elements of a Hilbert space, so in this case, we define the multiple

functional canonical correlation analysis, MFCCA.

We justify our approaches by their application to two data sets and suitable

large sample theory. We derive consistency rates for the related transformation

and correlation estimators, and show that it is possible to relax two common

assumptions on the compactness of the underlying cross-covariance operators and

the independence of the data.

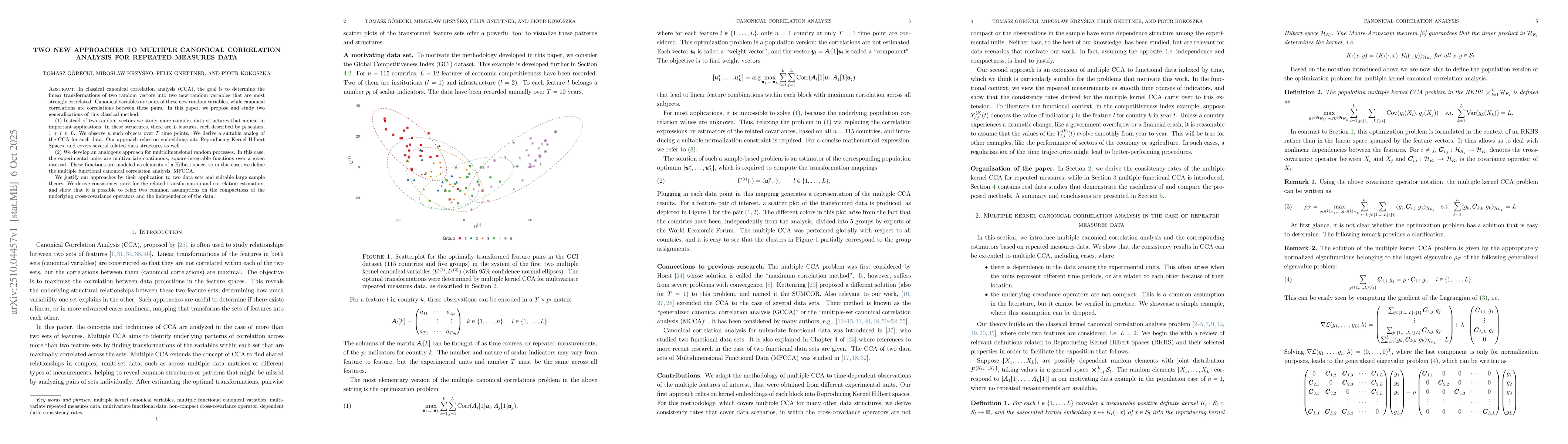

Discussion 0