Academic Profile

Statistics

Similar Authors

Papers on arXiv

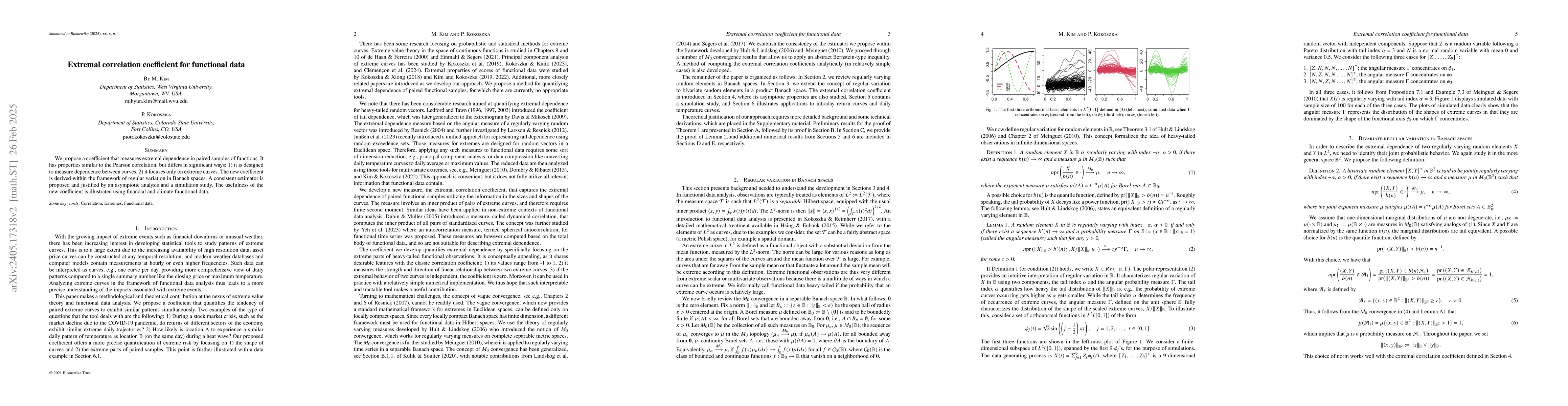

We propose a coefficient that measures dependence in paired samples of functions. It has properties similar to the Pearson correlation, but differs in significant ways: 1) it is designed to measure ...

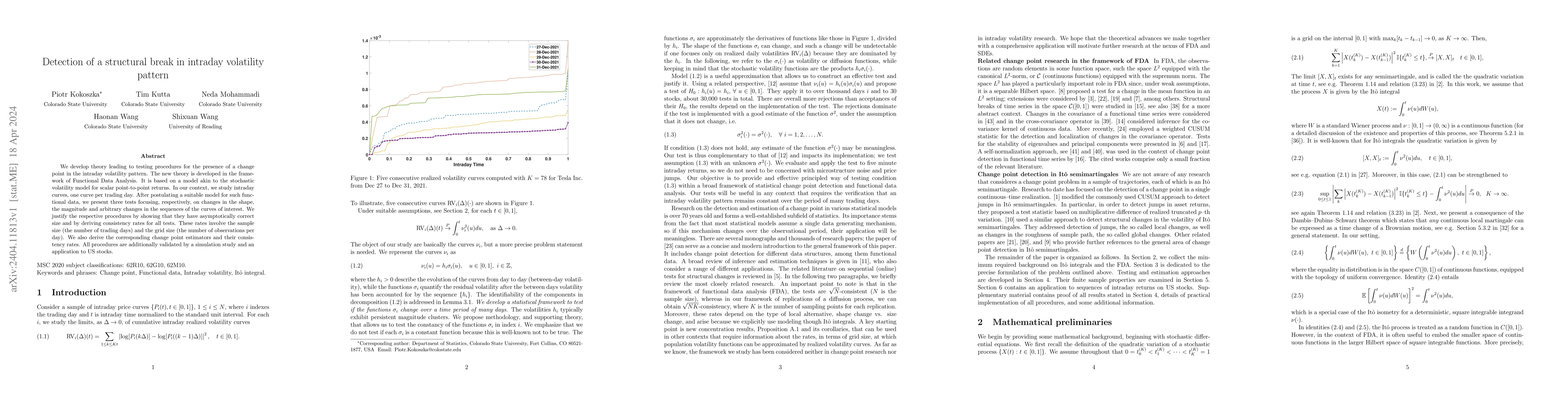

We develop theory leading to testing procedures for the presence of a change point in the intraday volatility pattern. The new theory is developed in the framework of Functional Data Analysis. It is...

For a broad class of nonlinear time series known as Bernoulli shifts, we establish the asymptotic normality of the smoothed periodogram estimator of the long-run variance. This estimator uses only a...

We propose a stochastic volatility model for time series of curves. It is motivated by dynamics of intraday price curves that exhibit both between days dependence and intraday price evolution. The c...

We develop a test of normality for spatially indexed functions. The assumption of normality is common in spatial statistics, yet no significance tests, or other means of assessment, have been availa...

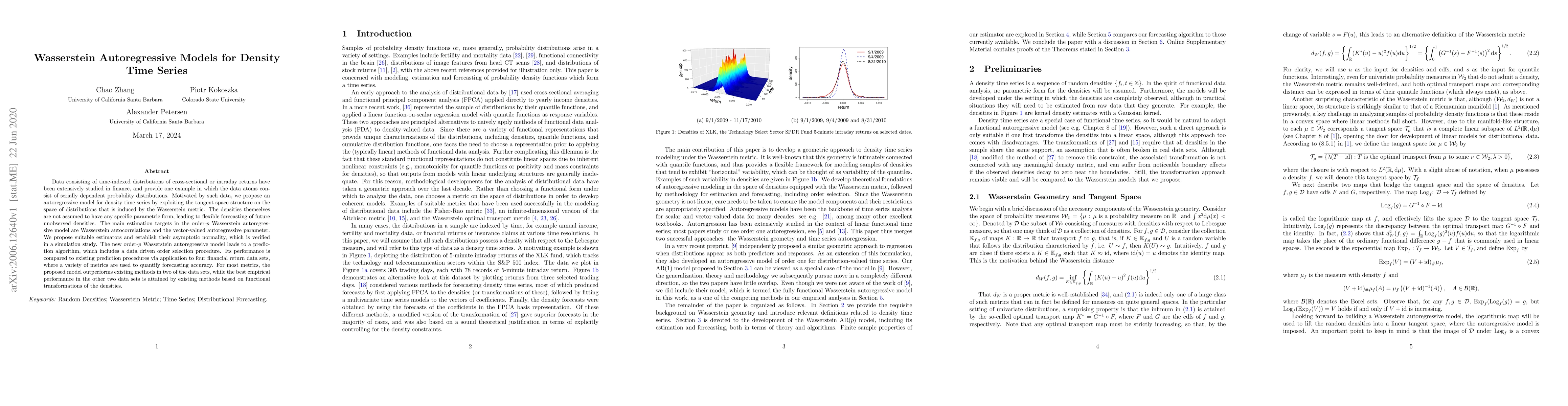

Data consisting of time-indexed distributions of cross-sectional or intraday returns have been extensively studied in finance, and provide one example in which the data atoms consist of serially dep...

Motivated by applications in functional data analysis, we study the partial sum process of sparsely observed, random functions. A key novelty of our analysis are bounds for the distributional distance...

We develop methodology and theory for the detection of a phase transition in a time-series of high-dimensional random matrices. In the model we study, at each time point \( t = 1,2,\ldots \), we obser...

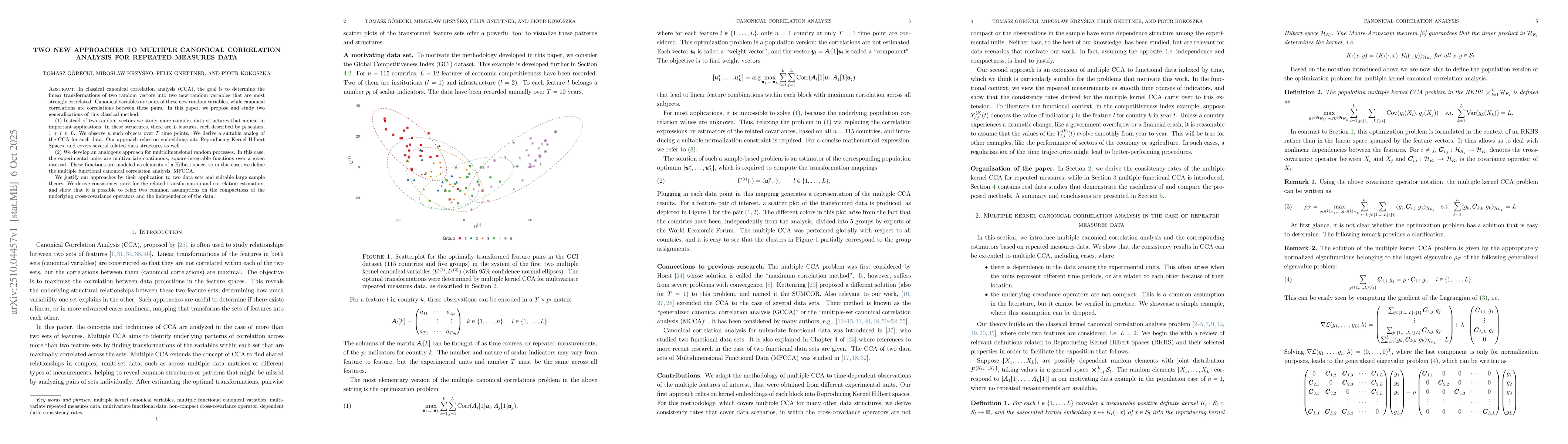

In classical canonical correlation analysis (CCA), the goal is to determine the linear transformations of two random vectors into two new random variables that are most strongly correlated. Canonical ...

We derive an estimator of the spectral density of a functional time series that is the output of a multilayer perceptron neural network. The estimator is motivated by difficulties with the computation...

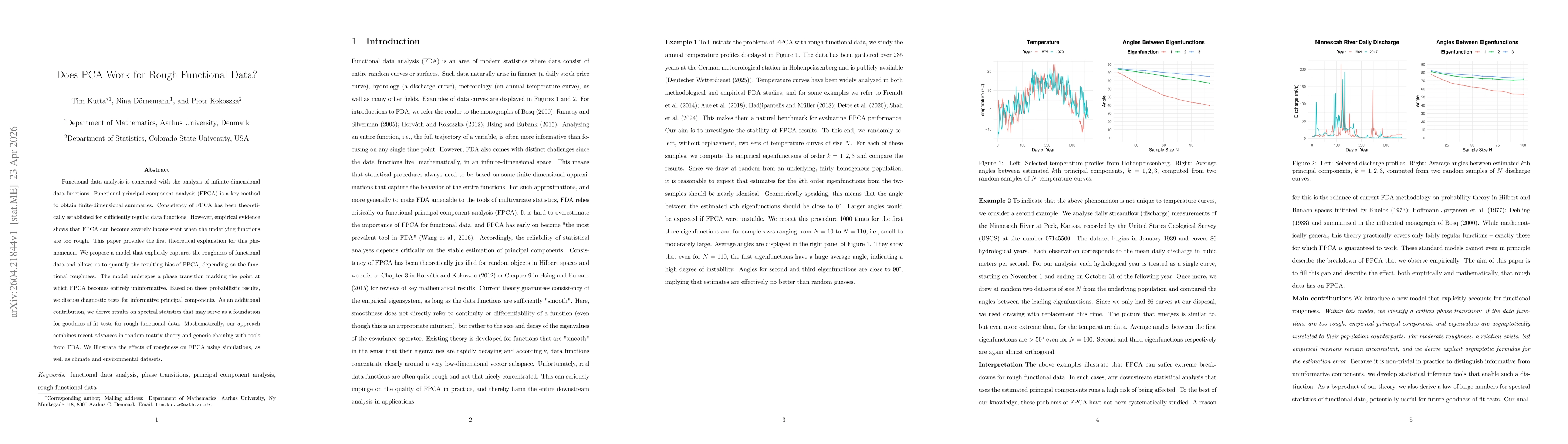

Functional data analysis is concerned with the analysis of infinite-dimensional data functions. Functional principal component analysis (FPCA) is a key method to obtain finite-dimensional summaries. C...