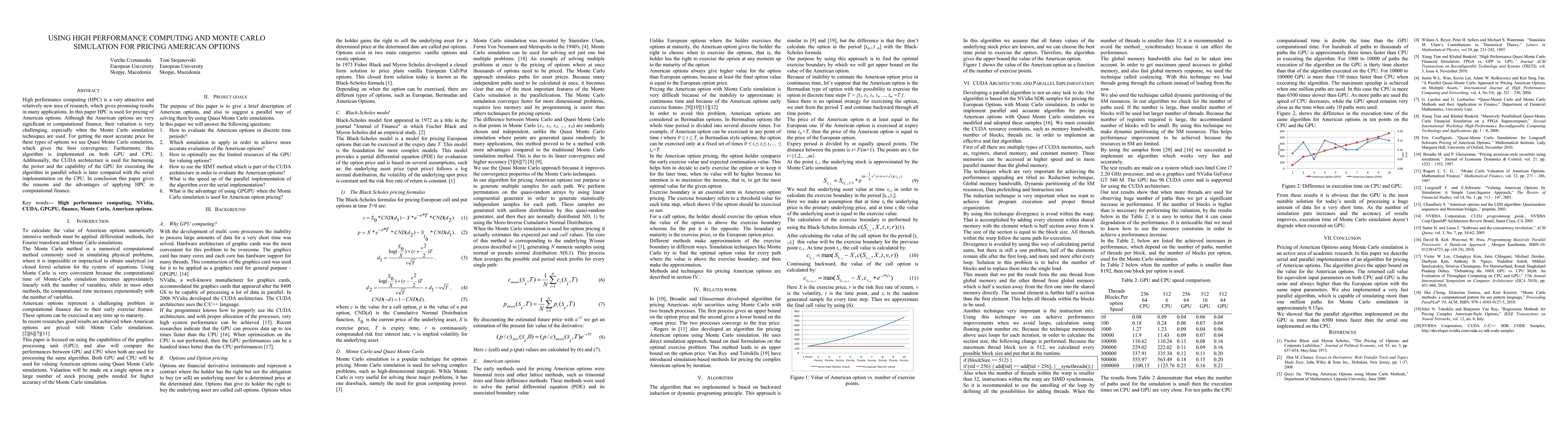

High performance computing (HPC) is a very attractive and relatively new area

of research, which gives promising results in many applications. In this paper

HPC is used for pricing of American options. Although the American options are

very significant in computational finance; their valuation is very challenging,

especially when the Monte Carlo simulation techniques are used. For getting the

most accurate price for these types of options we use Quasi Monte Carlo

simulation, which gives the best convergence. Furthermore, this algorithm is

implemented on both GPU and CPU. Additionally, the CUDA architecture is used

for harnessing the power and the capability of the GPU for executing the

algorithm in parallel which is later compared with the serial implementation on

the CPU. In conclusion this paper gives the reasons and the advantages of

applying HPC in computational finance.

Discussion 0