Vector Autoregression in Cryptocurrency Markets: Unraveling Complex Causal Networks

Publication

Metrics

AI Quick Summary

This paper demonstrates that multivariate linear models can effectively capture the complex interdependencies within cryptocurrency markets, revealing significant influence nodes. The study finds that node degree correlates with market capitalization, but some nodes have disproportionate influence, highlighting the importance of a few key coins in driving market dynamics.

Paper Preview

Abstract

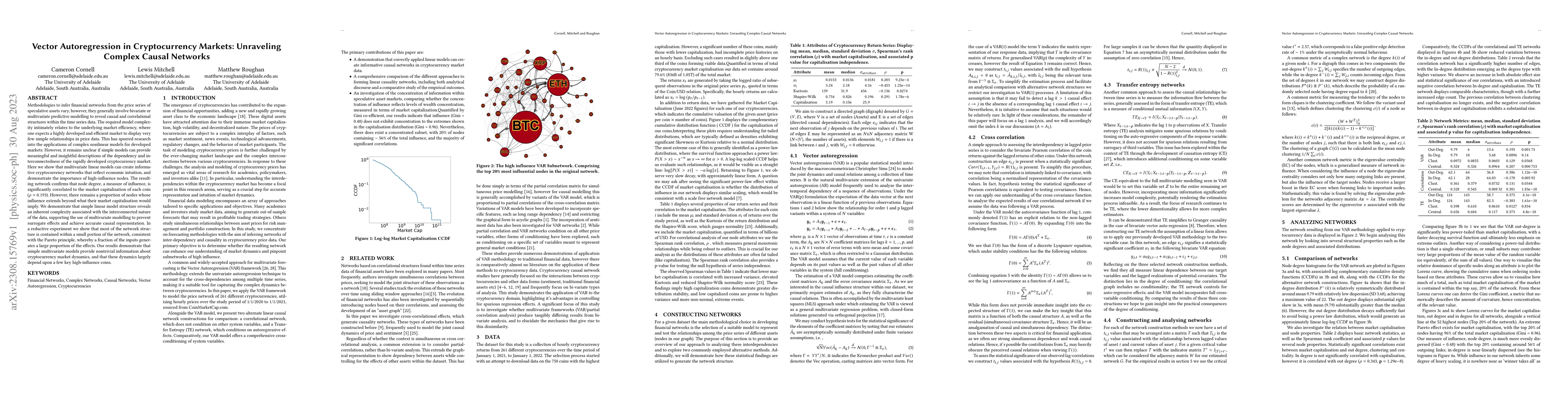

Methodologies to infer financial networks from the price series of speculative assets vary, however, they generally involve bivariate or multivariate predictive modelling to reveal causal and correlational structures within the time series data. The required model complexity intimately relates to the underlying market efficiency, where one expects a highly developed and efficient market to display very few simple relationships in price data. This has spurred research into the applications of complex nonlinear models for developed markets. However, it remains unclear if simple models can provide meaningful and insightful descriptions of the dependency and interconnectedness of the rapidly developed cryptocurrency market. Here we show that multivariate linear models can create informative cryptocurrency networks that reflect economic intuition, and demonstrate the importance of high-influence nodes. The resulting network confirms that node degree, a measure of influence, is significantly correlated to the market capitalisation of each coin ($\rho=0.193$). However, there remains a proportion of nodes whose influence extends beyond what their market capitalisation would imply. We demonstrate that simple linear model structure reveals an inherent complexity associated with the interconnected nature of the data, supporting the use of multivariate modelling to prevent surrogate effects and achieve accurate causal representation. In a reductive experiment we show that most of the network structure is contained within a small portion of the network, consistent with the Pareto principle, whereby a fraction of the inputs generates a large proportion of the effects. Our results demonstrate that simple multivariate models provide nontrivial information about cryptocurrency market dynamics, and that these dynamics largely depend upon a few key high-influence coins.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0