Large Language Models (LLMs) have recently gained popularity in stock trading

for their ability to process multimodal financial data. However, most existing

methods focus on single-stock trading and lack the capacity to reason over

multiple candidates for portfolio construction. Moreover, they typically lack

the flexibility to revise their strategies in response to market shifts,

limiting their adaptability in real-world trading. To address these challenges,

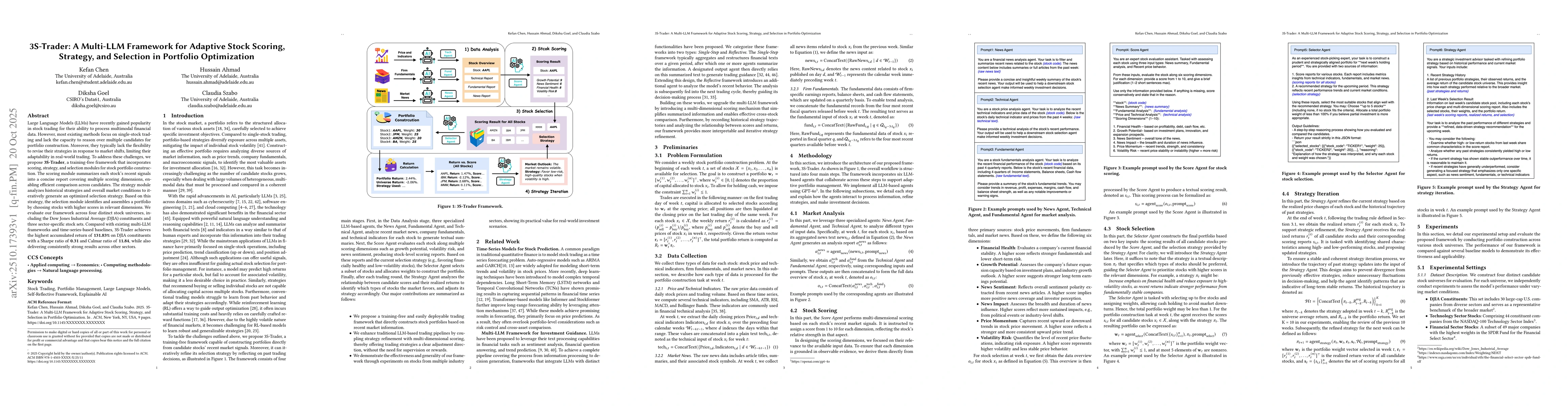

we propose 3S-Trader, a training-free framework that incorporates scoring,

strategy, and selection modules for stock portfolio construction. The scoring

module summarizes each stock's recent signals into a concise report covering

multiple scoring dimensions, enabling efficient comparison across candidates.

The strategy module analyzes historical strategies and overall market

conditions to iteratively generate an optimized selection strategy. Based on

this strategy, the selection module identifies and assembles a portfolio by

choosing stocks with higher scores in relevant dimensions. We evaluate our

framework across four distinct stock universes, including the Dow Jones

Industrial Average (DJIA) constituents and three sector-specific stock sets.

Compared with existing multi-LLM frameworks and time-series-based baselines,

3S-Trader achieves the highest accumulated return of 131.83% on DJIA

constituents with a Sharpe ratio of 0.31 and Calmar ratio of 11.84, while also

delivering consistently strong results across other sectors.

Discussion 0