01

MethodologyHow they did it

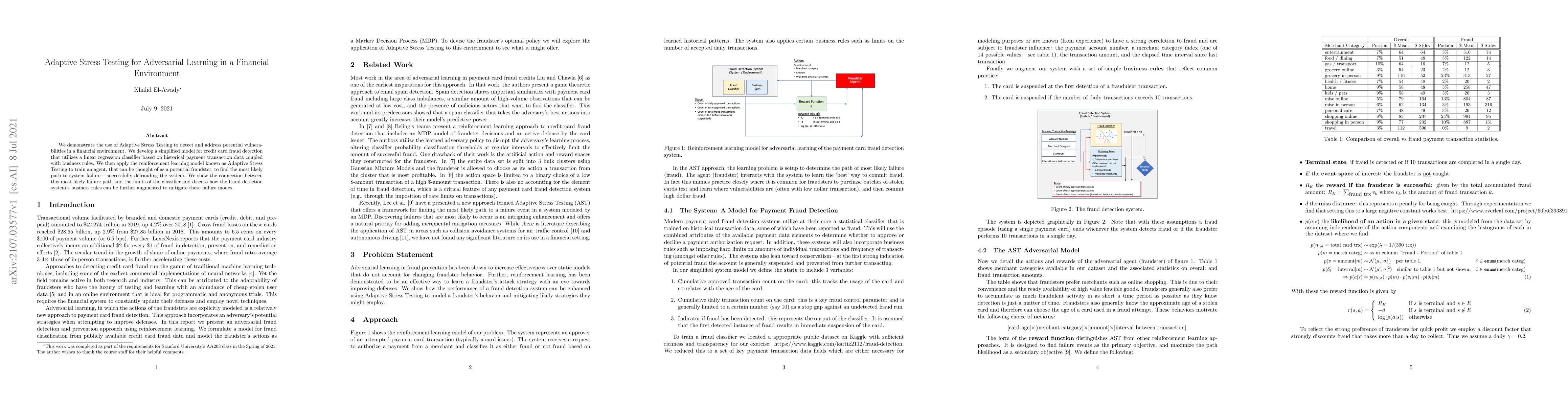

The paper demonstrates Adaptive Stress Testing (AST) for adversarial learning in a financial environment using a simplified credit card fraud detection model based on historical transaction data and business rules. A reinforcement learning model is applied to train an agent simulating a potential fraudster to find the most likely path to system failure.

Discussion 0