Large language models show promise for financial decision-making, yet

deploying them as autonomous trading agents raises fundamental challenges: how

to adapt instructions when rewards arrive late and obscured by market noise,

how to synthesize heterogeneous information streams into coherent decisions,

and how to bridge the gap between model outputs and executable market actions.

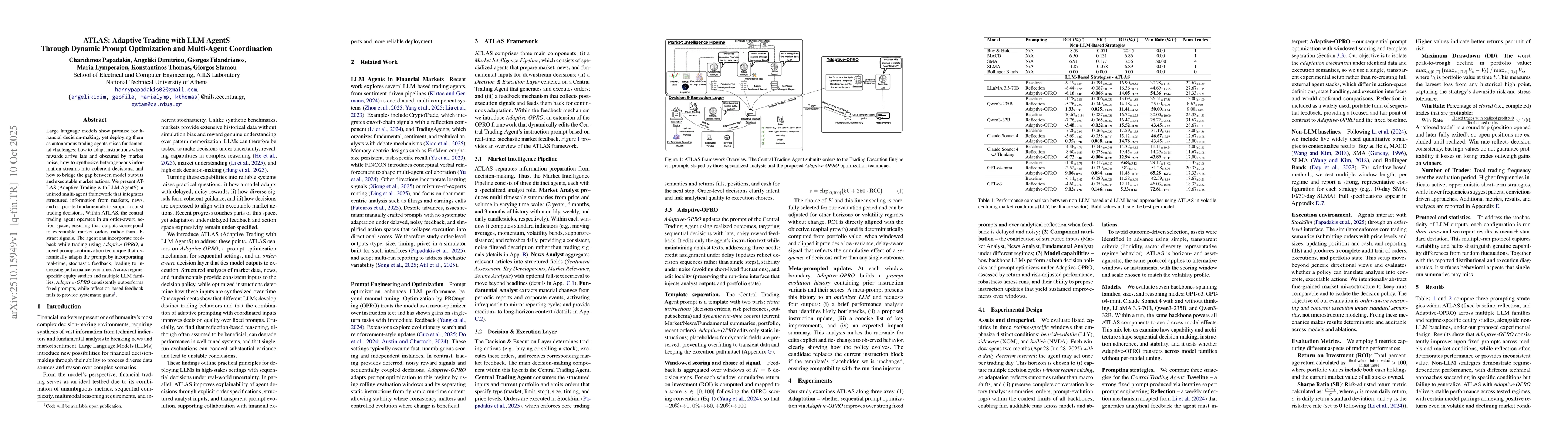

We present ATLAS (Adaptive Trading with LLM AgentS), a unified multi-agent

framework that integrates structured information from markets, news, and

corporate fundamentals to support robust trading decisions. Within ATLAS, the

central trading agent operates in an order-aware action space, ensuring that

outputs correspond to executable market orders rather than abstract signals.

The agent can incorporate feedback while trading using Adaptive-OPRO, a novel

prompt-optimization technique that dynamically adapts the prompt by

incorporating real-time, stochastic feedback, leading to increasing performance

over time. Across regime-specific equity studies and multiple LLM families,

Adaptive-OPRO consistently outperforms fixed prompts, while reflection-based

feedback fails to provide systematic gains.

Discussion 0