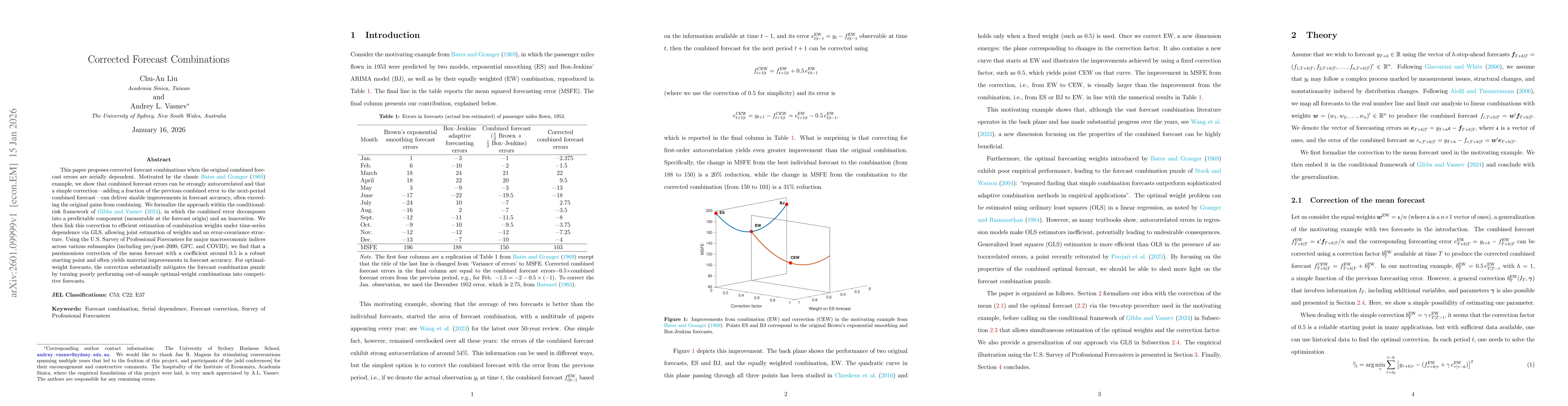

This paper proposes corrected forecast combinations when the original combined forecast errors are serially dependent. Motivated by the classic Bates and Granger (1969) example, we show that combined forecast errors can be strongly autocorrelated and that a simple correction--adding a fraction of the previous combined error to the next-period combined forecast--can deliver sizable improvements in forecast accuracy, often exceeding the original gains from combining. We formalize the approach within the conditional risk framework of Gibbs and Vasnev (2024), in which the combined error decomposes into a predictable component (measurable at the forecast origin) and an innovation. We then link this correction to efficient estimation of combination weights under time-series dependence via GLS, allowing joint estimation of weights and an error-covariance structure. Using the U.S. Survey of Professional Forecasters for major macroeconomic indices across various subsamples (including pre and post-2000, GFC, and COVID), we find that a parsimonious correction of the mean forecast with a coefficient around 0.5 is a robust starting point and often yields material improvements in forecast accuracy. For optimal-weight forecasts, the correction substantially mitigates the forecast combination puzzle by turning poorly performing out-of-sample optimal-weight combinations into competitive forecasts.

Discussion 0