Authors

Publication

Metrics

Quick Actions

AI Quick Summary

This paper examines overlooked data-generating processes for factors in return differences in time-series asset pricing, finding that traditional methods significantly underestimate market returns. It argues that Fama-French three-factor models may be misspecified and proposes using non-difference compound returns for a more accurate analysis.

Paper Preview

Abstract

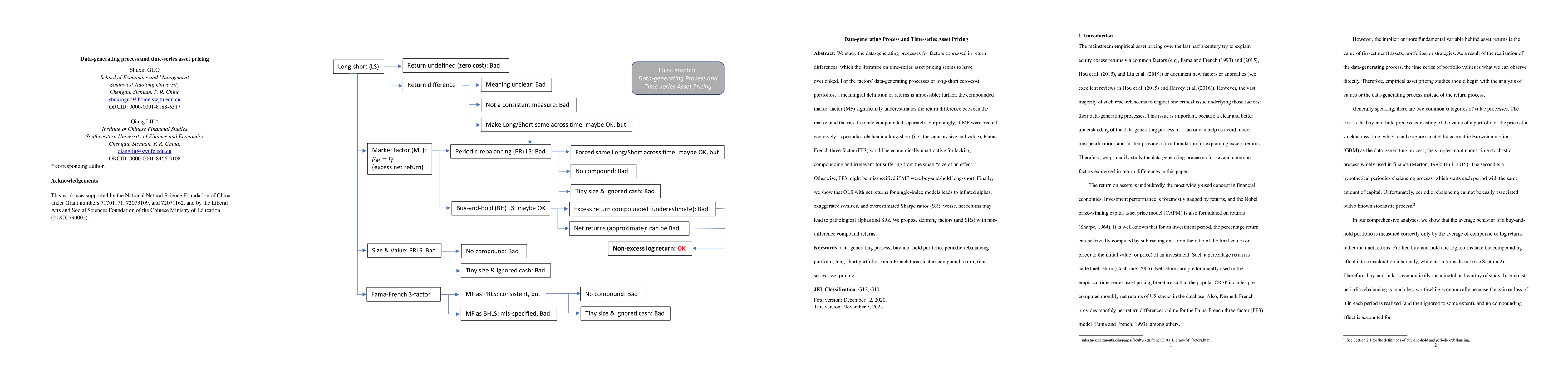

We study the data-generating processes for factors expressed in return differences, which the literature on time-series asset pricing seems to have overlooked. For the factors' data-generating processes or long-short zero-cost portfolios, a meaningful definition of returns is impossible; further, the compounded market factor (MF) significantly underestimates the return difference between the market and the risk-free rate compounded separately. Surprisingly, if MF were treated coercively as periodic-rebalancing long-short (i.e., the same as size and value), Fama-French three-factor (FF3) would be economically unattractive for lacking compounding and irrelevant for suffering from the small "size of an effect." Otherwise, FF3 might be misspecified if MF were buy-and-hold long-short. Finally, we show that OLS with net returns for single-index models leads to inflated alphas, exaggerated t-values, and overestimated Sharpe ratios (SR); worse, net returns may lead to pathological alphas and SRs. We propose defining factors (and SRs) with non-difference compound returns.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

How to Cite This Paper

@article{liu2024data,

title = {Data-generating process and time-series asset pricing},

author = {Liu, Qiang and Guo, Shuxin},

year = {2024},

eprint = {2405.10920},

archivePrefix = {arXiv},

primaryClass = {q-fin.GN},

}Liu, Q., & Guo, S. (2024). Data-generating process and time-series asset pricing. arXiv. https://arxiv.org/abs/2405.10920Liu, Qiang, and Shuxin Guo. "Data-generating process and time-series asset pricing." arXiv, 2024, arxiv.org/abs/2405.10920.PDF Preview

Key Terms

Similar Papers

Found 4 papersData Generating Process to Evaluate Causal Discovery Techniques for Time Series Data

Andrew R. Lawrence, Rui Sampaio, Marcus Kaiser et al.

Empirical Asset Pricing via Ensemble Gaussian Process Regression

Damir Filipović, Puneet Pasricha

No citations found for this paper.

Comments (0)