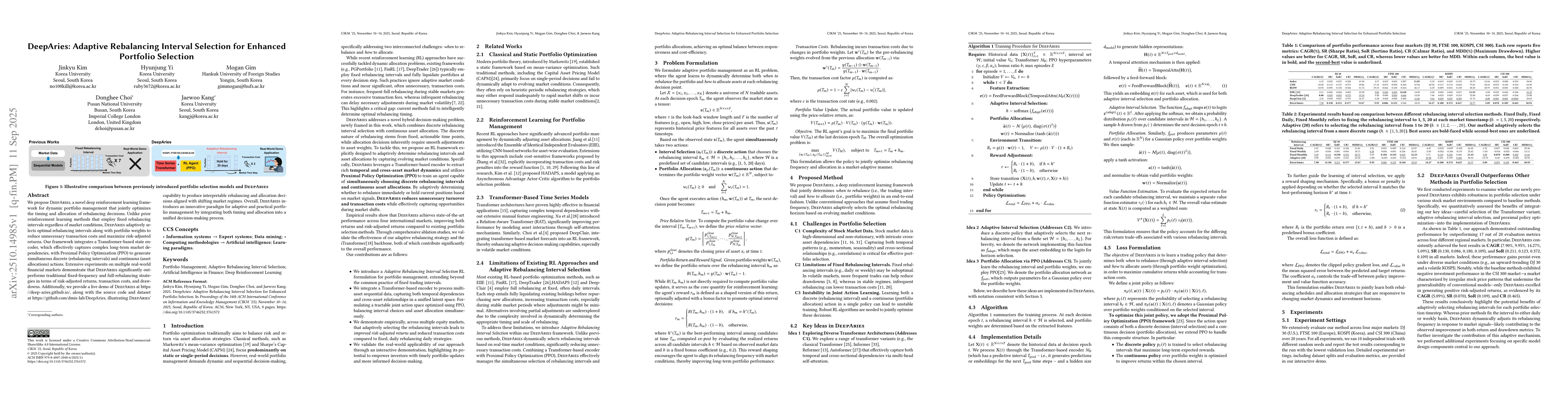

We propose DeepAries , a novel deep reinforcement learning framework for

dynamic portfolio management that jointly optimizes the timing and allocation

of rebalancing decisions. Unlike prior reinforcement learning methods that

employ fixed rebalancing intervals regardless of market conditions, DeepAries

adaptively selects optimal rebalancing intervals along with portfolio weights

to reduce unnecessary transaction costs and maximize risk-adjusted returns. Our

framework integrates a Transformer-based state encoder, which effectively

captures complex long-term market dependencies, with Proximal Policy

Optimization (PPO) to generate simultaneous discrete (rebalancing intervals)

and continuous (asset allocations) actions. Extensive experiments on multiple

real-world financial markets demonstrate that DeepAries significantly

outperforms traditional fixed-frequency and full-rebalancing strategies in

terms of risk-adjusted returns, transaction costs, and drawdowns. Additionally,

we provide a live demo of DeepAries at https://deep-aries.github.io/, along

with the source code and dataset at https://github.com/dmis-lab/DeepAries,

illustrating DeepAries' capability to produce interpretable rebalancing and

allocation decisions aligned with shifting market regimes. Overall, DeepAries

introduces an innovative paradigm for adaptive and practical portfolio

management by integrating both timing and allocation into a unified

decision-making process.

Discussion 0