AI Quick Summary

DeRegiME introduces a probabilistic multi-horizon forecaster that separates latent uncertainty regimes from the signal using a sparse variational Gaussian process with a nonstationary regime-mixing kernel and a shared gate, producing a single posterior rather than a mixture of experts. It yields an interpretable mean–residual–noise decomposition, identifies regime clusters and implicit changepoints, and achieves consistent, state-of-the-art improvements in predictive density, CRPS, and MSE across diverse distribution-shift scenarios.

Quick Answers

What is "DeRegiME: Deep Regime Mixtures for Probabilistic Forecasting under Distribution Shift" about?

DeRegiME introduces a probabilistic multi-horizon forecaster that separates latent uncertainty regimes from the signal using a sparse variational Gaussian process with a nonstationary regime-mixing kernel and a shared gate, producing a single posterior rather than a mixture of experts. It yields an interpretable mean–residual–noise decomposition, identifies regime clusters and implicit changepoints, and achieves consistent, state-of-the-art improvements in predictive density, CRPS, and MSE across diverse distribution-shift scenarios.

What methodology did the authors use?

DeRegiME introduces a direct multi-horizon probabilistic forecaster that separates latent uncertainty regimes from the signal using a sparse variational Gaussian process with a nonstationary regime-mixing kernel and per-regime sub-kernels; a shared gate assigns forecast locations to horizon-indexed regimes, enabling a mean-residual-noise decomposition and horizon-dependent regime allocations, with predictive density computed by marginalising over regime labels and residuals via a Student-t... More in Methodology →

What are the key results?

Across ten benchmarks and three encoder grids, DeRegiME achieves a 20.3% improvement in NLPD over the strongest encoder-matched baseline (DeepAR/GluonTS-style dynamic Student-t head). — Parallel improvements are observed in CRPS (3.0%) and MSE (4.7%), with consistency across datasets exhibiting abrupt, gradual, and seasonal distribution shifts. More in Key Results →

Why is this work significant?

The approach provides an interpretable, probabilistic forecasting framework that preserves residual structure and regime dynamics under distribution shift, offering state-of-the-art predictive density while exposing regime transitions and uncertainty regimes across multiple horizons. More in Significance →

What are the main limitations?

The method relies on sparse-GP approximations; scalability to extremely large datasets or very high-resolution grids may be constrained by kernel evaluations. — Performance depends on the quality of regime-feature extraction z_r(ξ) and the learned gate; mis-specification could dampen regime clarity in some domains. More in Limitations →

Paper Preview

Abstract

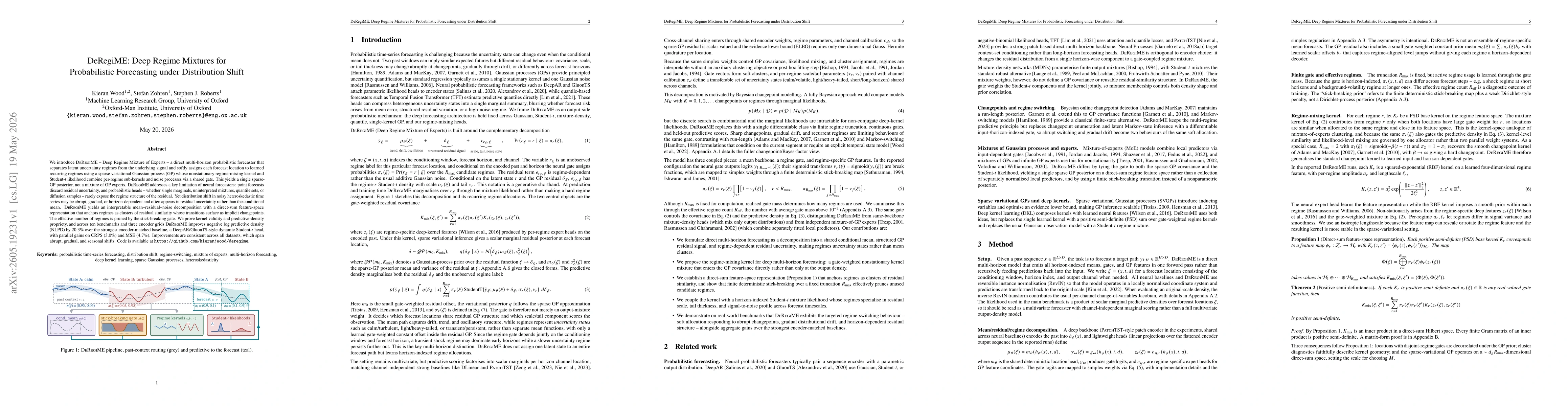

We introduce DeRegiME -- Deep Regime Mixture of Experts -- a direct multi-horizon probabilistic forecaster that separates latent uncertainty regimes from the underlying signal and softly assigns each forecast location to learned recurring regimes using a sparse variational Gaussian process (GP) whose nonstationary regime-mixing kernel and Student-t likelihood combine per-regime sub-kernels and noise processes via a shared gate. This yields a single sparse-GP posterior, not a mixture of GP experts. DeRegiME addresses a key limitation of neural forecasters: point forecasts discard residual uncertainty, and probabilistic heads -- whether single marginals, uninterpreted mixtures, quantile sets, or diffusion samples -- rarely expose the regime structure of the residual. Yet distribution shift in noisy heteroskedastic time series may be abrupt, gradual, or horizon-dependent and often appears in residual uncertainty rather than the conditional mean. DeRegiME yields an interpretable mean-residual-noise decomposition with a direct-sum feature-space representation that anchors regimes as clusters of residual similarity whose transitions surface as implicit changepoints. The effective number of regimes is pruned by the stick-breaking gate. We prove kernel validity and predictive-density propriety, and across ten benchmarks and three encoder grids DeRegiME improves negative log predictive density (NLPD) by 20.3% over the strongest encoder-matched baseline, a DeepAR/GluonTS-style dynamic Student-t head, with parallel gains on CRPS (3.0%) and MSE (4.7%). Improvements are consistent across all datasets, which span abrupt, gradual, and seasonal shifts.

AI Key Findings

Generated May 31, 2026

Methodology — What approach did the authors take?

DeRegiME introduces a direct multi-horizon probabilistic forecaster that separates latent uncertainty regimes from the signal using a sparse variational Gaussian process with a nonstationary regime-mixing kernel and per-regime sub-kernels; a shared gate assigns forecast locations to horizon-indexed regimes, enabling a mean-residual-noise decomposition and horizon-dependent regime allocations, with predictive density computed by marginalising over regime labels and residuals via a Student-t likelihood.

Key Results — What are the main findings?

- Across ten benchmarks and three encoder grids, DeRegiME achieves a 20.3% improvement in NLPD over the strongest encoder-matched baseline (DeepAR/GluonTS-style dynamic Student-t head).

- Parallel improvements are observed in CRPS (3.0%) and MSE (4.7%), with consistency across datasets exhibiting abrupt, gradual, and seasonal distribution shifts.

- The method yields an interpretable mean–residual–noise decomposition and horizon-indexed regime allocations that surface as implicit changepoints.

Significance — Why does this research matter?

The approach provides an interpretable, probabilistic forecasting framework that preserves residual structure and regime dynamics under distribution shift, offering state-of-the-art predictive density while exposing regime transitions and uncertainty regimes across multiple horizons.

Technical Contribution — What is the technical contribution?

Propose DeRegiME, a deep regime mixture of experts framework that uses a sparse variational GP with a nonstationary regime-mixing kernel and a shared gate to yield a single posterior over residuals, enabling horizon-indexed regime allocations and a predictive density that marginalises over latent regimes and residuals.

Novelty — What is new about this work?

Introduces horizon-dependent regime allocations within a deep GP-based probabilistic forecaster, achieving an interpretable mean–residual–noise decomposition and avoiding a pure mixture-of-experts; provides kernel validity and predictive-density propriety proofs across multi-horizon distribution-shift scenarios.

Limitations — What are the limitations of this study?

- The method relies on sparse-GP approximations; scalability to extremely large datasets or very high-resolution grids may be constrained by kernel evaluations.

- Performance depends on the quality of regime-feature extraction z_r(ξ) and the learned gate; mis-specification could dampen regime clarity in some domains.

Future Work — What did the authors propose for future work?

- Extend to even larger-scale time series and alternative kernel families to capture more complex regime dynamics.

- Investigate automatic regime number pruning dynamics under nonstationary regimes and potential online adaptation.

- Explore integration with alternative likelihoods and training objectives to further enhance calibration under extreme distribution shifts.

How to Cite This Paper

@article{wood2026deregime,

title = {DeRegiME: Deep Regime Mixtures for Probabilistic Forecasting under Distribution Shift},

author = {Wood, Kieran and Zohren, Stefan and Roberts, Stephen J.},

year = {2026},

eprint = {2605.19231},

archivePrefix = {arXiv},

primaryClass = {cs.LG},

}Wood, K., Zohren, S., & Roberts, S. (2026). DeRegiME: Deep Regime Mixtures for Probabilistic Forecasting under Distribution Shift. arXiv. https://arxiv.org/abs/2605.19231Wood, Kieran, et al. "DeRegiME: Deep Regime Mixtures for Probabilistic Forecasting under Distribution Shift." arXiv, 2026, arxiv.org/abs/2605.19231.PDF Preview

Similar Papers

Found 4 papersAdaptive Sampling for Probabilistic Forecasting under Distribution Shift

Syama Sundar Rangapuram, Rajbir Singh Nirwan, Michael Bohlke-Schneider et al.

Probabilistic Hierarchical Forecasting with Deep Poisson Mixtures

Kin G. Olivares, O. Nganba Meetei, Ruijun Ma et al.

Forecasting labels under distribution-shift for machine-guided sequence design

Lauren Berk Wheelock, Sam Sinai, Stephen Malina et al.

Regime-Arrival Uncertainty in Generalization Bounds under Distribution Shift

Prince Poudel

Comments (0)