Double-Path Adaptive-correlation Spatial-Temporal Inverted Transformer for Stock Time Series Forecasting

Publication

Metrics

AI Quick Summary

The paper proposes a Double-Path Adaptive-correlation Spatial-Temporal Inverted Transformer (DPA-STIFormer) for stock time series forecasting, leveraging feature changes as tokens to model dynamic spatial information. The model employs a Double Direction Self-adaptation Fusion mechanism to extract and fuse temporal and feature correlations, achieving state-of-the-art performance on stock market datasets.

Paper Preview

Abstract

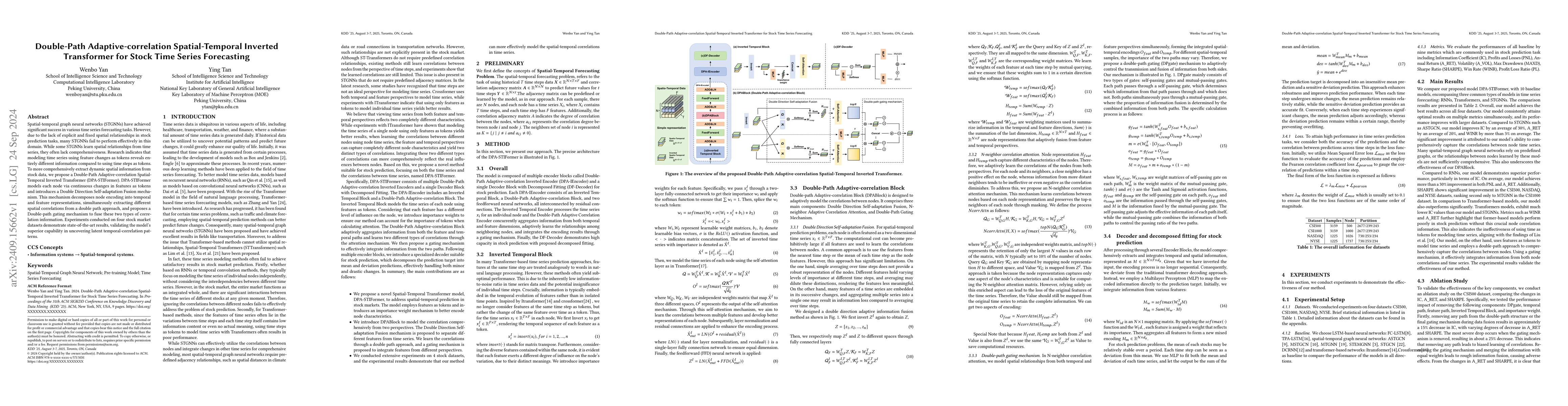

Spatial-temporal graph neural networks (STGNNs) have achieved significant success in various time series forecasting tasks. However, due to the lack of explicit and fixed spatial relationships in stock prediction tasks, many STGNNs fail to perform effectively in this domain. While some STGNNs learn spatial relationships from time series, they often lack comprehensiveness. Research indicates that modeling time series using feature changes as tokens reveals entirely different information compared to using time steps as tokens. To more comprehensively extract dynamic spatial information from stock data, we propose a Double-Path Adaptive-correlation Spatial-Temporal Inverted Transformer (DPA-STIFormer). DPA-STIFormer models each node via continuous changes in features as tokens and introduces a Double Direction Self-adaptation Fusion mechanism. This mechanism decomposes node encoding into temporal and feature representations, simultaneously extracting different spatial correlations from a double path approach, and proposes a Double-path gating mechanism to fuse these two types of correlation information. Experiments conducted on four stock market datasets demonstrate state-of-the-art results, validating the model's superior capability in uncovering latent temporal-correlation patterns.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0