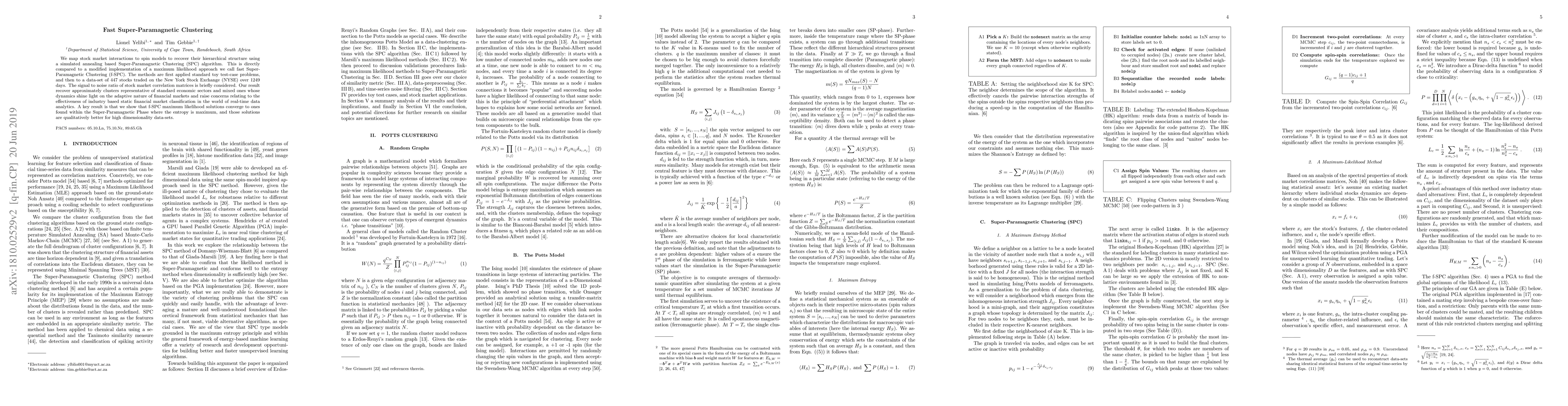

Fast Super-Paramagnetic Clustering

Publication

Metrics

AI Quick Summary

A new algorithm called Fast Super-Paramagnetic Clustering (f-SPC) is proposed to analyze stock market interactions and identify clusters representative of economic sectors, with results showing improved performance for high-dimensional data sets.

Paper Preview

Abstract

We map stock market interactions to spin models to recover their hierarchical structure using a simulated annealing based Super-Paramagnetic Clustering (SPC) algorithm. This is directly compared to a modified implementation of a maximum likelihood approach we call Fast Super-Paramagnetic Clustering (f-SPC). The methods are first applied standard toy test-case problems, and then to a data-set of 447 stocks traded on the New York Stock Exchange (NYSE) over 1249 days. The signal to noise ratio of stock market correlation matrices is briefly considered. Our result recover approximately clusters representative of standard economic sectors and mixed ones whose dynamics shine light on the adaptive nature of financial markets and raise concerns relating to the effectiveness of industry based static financial market classification in the world of real-time data analytics. A key result is that we show that f-SPC maximum likelihood solutions converge to ones found within the Super-Paramagnetic Phase where the entropy is maximum, and those solutions are qualitatively better for high dimensionality data-sets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0