Publication

Metrics

AI Quick Summary

This paper compares the performance of three multivariate forecasting techniques—Vector Auto Regression, Support Vector Machine, and Recurrent Neural Networks with Long Short-Term Memory—to predict the USD/INR foreign exchange rate. The results show that contemporary machine learning and deep learning techniques outperform traditional econometric methods, with RNN-LSTM achieving the highest accuracy at 97.83%.

Paper Preview

Abstract

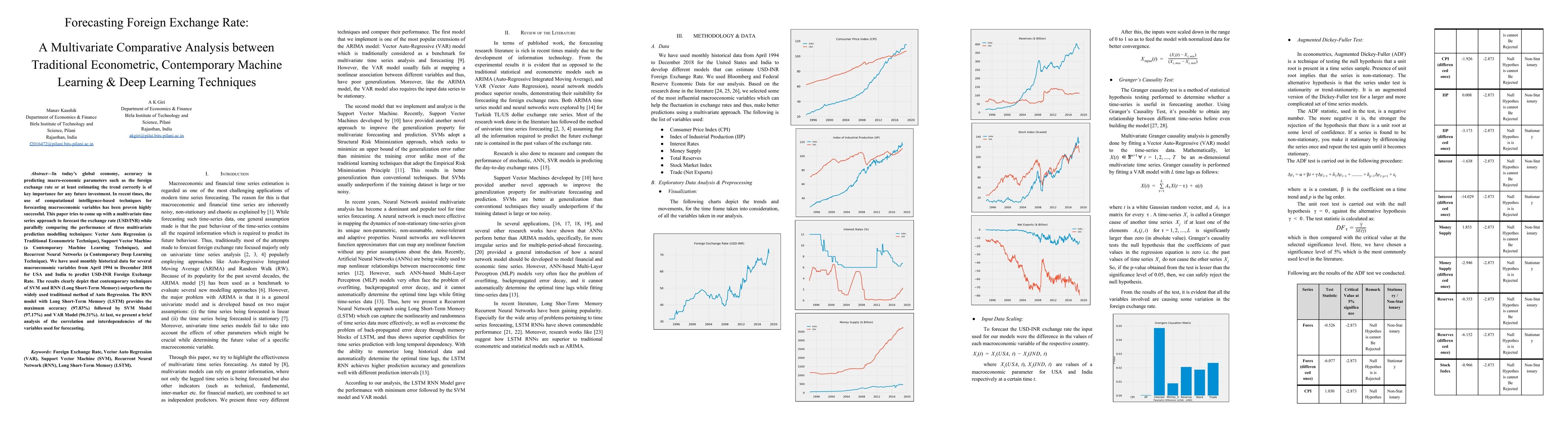

In todays global economy, accuracy in predicting macro-economic parameters such as the foreign the exchange rate or at least estimating the trend correctly is of key importance for any future investment. In recent times, the use of computational intelligence-based techniques for forecasting macroeconomic variables has been proven highly successful. This paper tries to come up with a multivariate time series approach to forecast the exchange rate (USD/INR) while parallelly comparing the performance of three multivariate prediction modelling techniques: Vector Auto Regression (a Traditional Econometric Technique), Support Vector Machine (a Contemporary Machine Learning Technique), and Recurrent Neural Networks (a Contemporary Deep Learning Technique). We have used monthly historical data for several macroeconomic variables from April 1994 to December 2018 for USA and India to predict USD-INR Foreign Exchange Rate. The results clearly depict that contemporary techniques of SVM and RNN (Long Short-Term Memory) outperform the widely used traditional method of Auto Regression. The RNN model with Long Short-Term Memory (LSTM) provides the maximum accuracy (97.83%) followed by SVM Model (97.17%) and VAR Model (96.31%). At last, we present a brief analysis of the correlation and interdependencies of the variables used for forecasting.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0