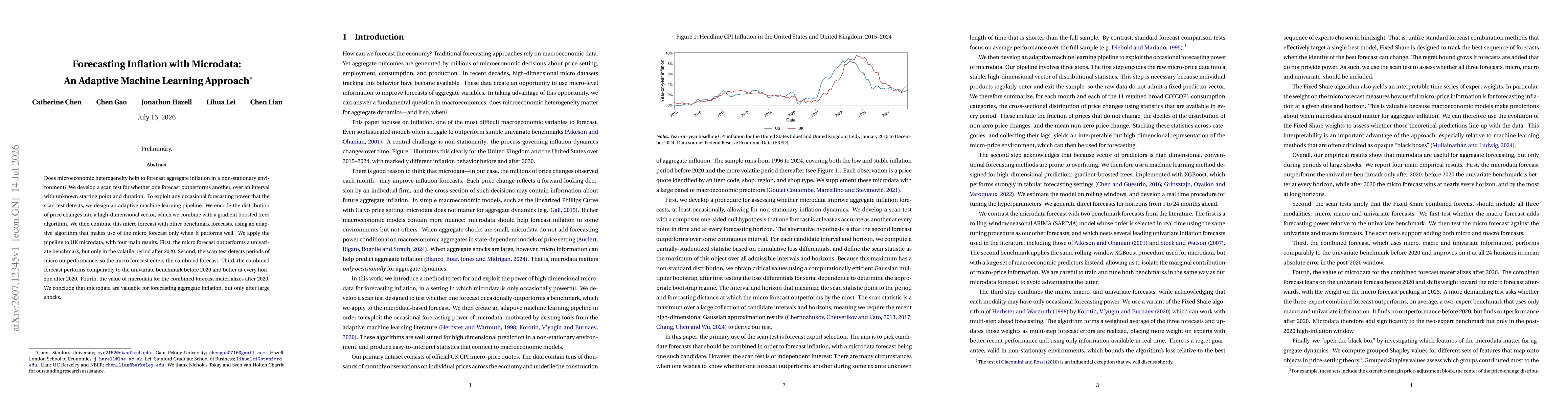

Does microeconomic heterogeneity help to forecast aggregate inflation in a non-stationary environment? We develop a scan test for whether one forecast outperforms another, over an interval with unknown starting point and duration. To exploit any occasional forecasting power that the scan test detects, we design an adaptive machine learning pipeline. We encode the distribution of price changes into a high-dimensional vector, which we combine with a gradient boosted trees algorithm. We then combine this micro forecast with other benchmark forecasts, using an adaptive algorithm that makes use of the micro forecast only when it performs well. We apply the pipeline to UK microdata, with four main results. First, the micro forecast outperforms a univariate benchmark, but only in the volatile period after 2020. Second, the scan test detects periods of micro outperformance, so the micro forecast enters the combined forecast. Third, the combined forecast performs comparably to the univariate benchmark before 2020 and better at every horizon after 2020. Fourth, the value of microdata for the combined forecast materializes after 2020. We conclude that microdata are valuable for forecasting aggregate inflation, but only after large shocks.

Discussion 0