01

MethodologyHow they did it

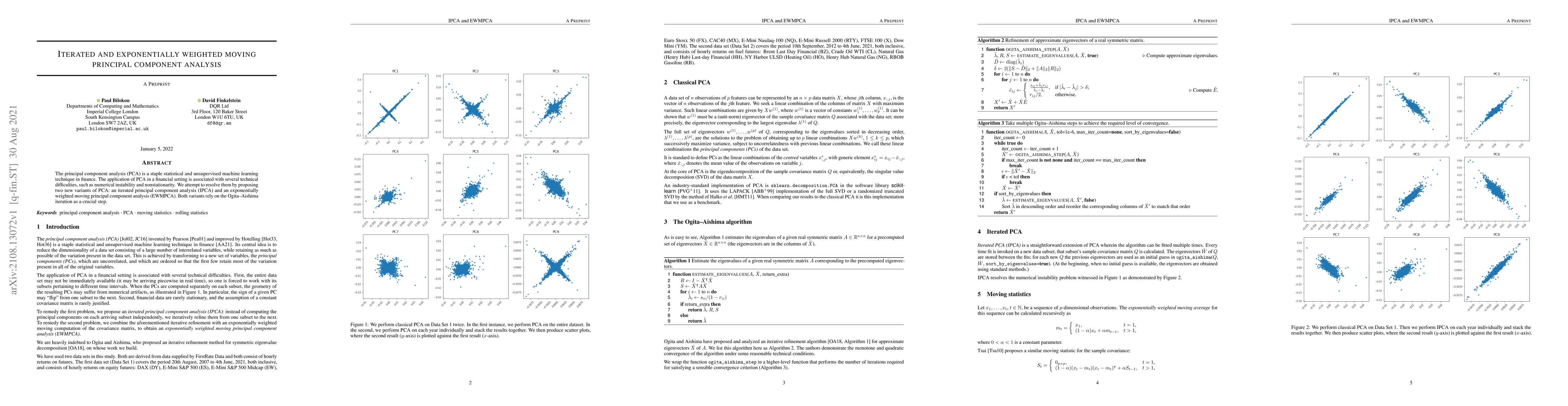

The paper proposes two new variants of PCA: Iterated Principal Component Analysis (IPCA) and Exponentially Weighted Moving Principal Component Analysis (EWMPCA), both utilizing the Ogita-Aishima iteration for numerical stability and addressing nonstationarity in financial data.

Discussion 0